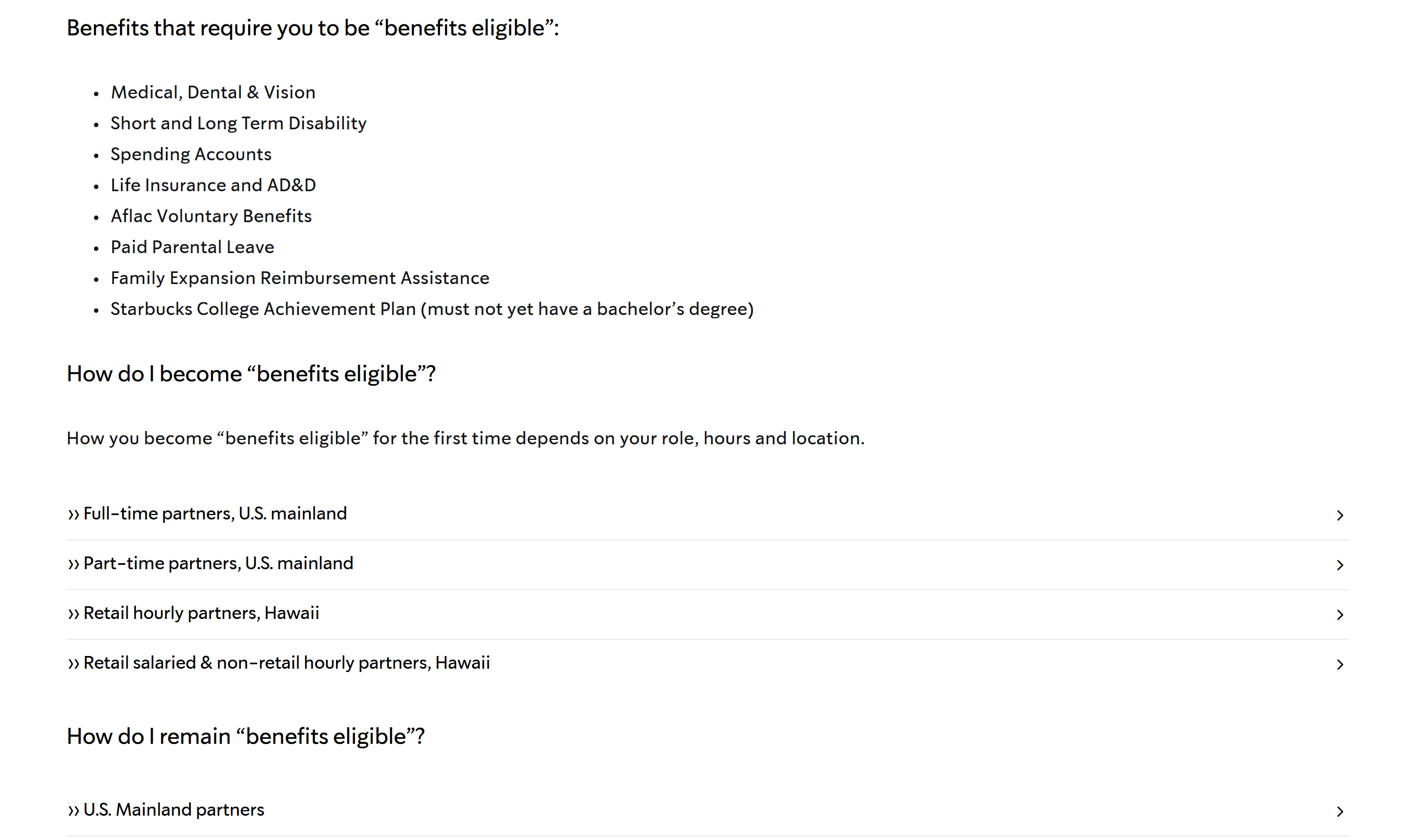

What Is Barista FIRE? America's Health Insurance Hack

A 20-hour Starbucks shift can knock $500,000 off the portfolio you need to quit your career. The catch: the strategy only exists because US health insurance is chained to your job.

Cite this article

Freedom Isn't Free (2026) What Is Barista FIRE? America's Health Insurance Hack. Available at: https://freedomisntfree.co.uk/articles/what-is-barista-fire (Accessed: 15 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Barista FIRE means quitting your career, letting your portfolio compound, and covering part of your expenses with a part-time job

- Every $1,000 of durable annual part-time income cuts roughly $25,000 off the portfolio you need

- The real prize is employer health insurance: Starbucks covers part-timers averaging 20 hours a week, which bridges the gap to Medicare at 65

- The whole strategy is a workaround for employer-tethered US healthcare, and it inherits the insecurity of the system it routes around

Barista FIRE numbers at a 4% withdrawal rate

| Annual spending | Part-time income | Portfolio must fund | Portfolio needed |

|---|---|---|---|

| $60,000 | $0 (full FIRE) | $60,000 | $1,500,000 |

| $60,000 | $12,000 | $48,000 | $1,200,000 |

| $60,000 | $20,000 | $40,000 | $1,000,000 |

| $50,000 | $20,000 | $30,000 | $750,000 |

Every $1,000 of durable annual part-time income cuts about $25,000 off the portfolio you need before you can quit.

What Is Barista FIRE? America's Health Insurance Hack

Barista FIRE gets described the same way across most American personal finance sites: quit your career years before traditional retirement, let your investments keep compounding, and plug the income gap with a relaxed part-time job. That description is accurate, and it misses the entire point. The strategy is not named after Starbucks because steaming milk is soothing. It is named after Starbucks because Starbucks offers health insurance to employees averaging just 20 hours a week, and in America, health insurance is the wall standing between you and early retirement.

We write about money from the UK, where the NHS means nobody has to delay quitting a job they hate over an insulin prescription. That outside view is useful here, because it makes the structure of barista FIRE easier to see: this is a healthcare strategy wearing a coffee apron. The part-time paycheque is the supporting act.

Contents

- What Barista FIRE Actually Means

- Barista FIRE vs Coast FIRE, Lean FIRE and Full FIRE

- The Health Insurance Bridge: Why the Job Beats the Paycheque

- The Barista FIRE Maths: A Worked Example in Dollars

- Who Barista FIRE Suits

- The Risks Nobody Prices In

- The Irony at the Heart of Barista FIRE

- Frequently Asked Questions

What Barista FIRE Actually Means

Barista FIRE is a variant of the broader FIRE movement (Financial Independence, Retire Early) in which you stop full-time work before you have saved a full retirement portfolio. Your investments cover most of your living costs through withdrawals, and a part-time job covers the rest.

The standard FIRE benchmark says you need roughly 25 times your annual spending invested before you can retire outright, the inverse of the 4% withdrawal rule. Barista FIRE says: you do not need the whole 25x if you are willing to keep earning something. You are not retired, but you are not employed in the way that was grinding you down either. You have swapped a career for a shift pattern, and swapped "I need this job" for "I could walk out on Friday."

Two things make the strategy work. The first is the maths of partial income, which we will get to. The second is specific to the United States: certain employers, most famously Starbucks, extend medical benefits to part-time staff. For an American in their 40s or 50s, that benefit can be worth more than the wages.

Barista FIRE vs Coast FIRE, Lean FIRE and Full FIRE

The FIRE flavours all answer the same question, "when can I stop?", with different definitions of stopping.

| Flavour | Do you still work? | What funds your life now? | Portfolio needed |

|---|---|---|---|

| Full FIRE | No | Portfolio withdrawals only | 25x annual spending |

| Lean FIRE | No | Portfolio withdrawals, small budget | 25x a deliberately lean spend |

| Coast FIRE | Yes, full-time | Your salary; you just stop saving | Enough that compounding alone hits your number by 65 |

| Barista FIRE | Yes, part-time | Portfolio withdrawals plus part-time pay | 25x the gap between spending and part-time income |

The one most often confused with barista FIRE is coast FIRE. The difference is what you are living on today. A coast FIRE household still works full-time and pays its bills from salary; the milestone just means they can stop contributing to retirement accounts. A barista FIRE household has actually quit and is drawing on the portfolio now, decades before a traditional retirement date.

Put differently: coast FIRE changes how you save, barista FIRE changes how you live. Coast is a milestone. Barista is an exit.

The coast FIRE calculator will show you the coast milestone for your own numbers (it displays dollars for US visitors), and it doubles as a sanity check for barista plans: if you have not even reached coast FIRE, quitting to work part-time means your eventual retirement is also underfunded, not just your present.

The Health Insurance Bridge: Why the Job Beats the Paycheque

The defining problem for any American who retires at 45 or 50 is the healthcare gap. Medicare eligibility begins at 65, with a sign-up window opening three months before your 65th birthday. Retire at 50 and you have a 15-year stretch in which a single serious diagnosis, uninsured, can vaporise the portfolio you spent two decades building. No other rich country makes its early retirees solve this puzzle.

Barista FIRE is the puzzle's most popular answer. Starbucks extends medical, dental and vision cover to part-time staff: under its published eligibility rules, US mainland partners qualify after 240 paid hours over three consecutive months, then keep the plan with 520 paid hours per six-month period, an average of 20 hours a week. Federal law only obliges large employers to cover staff working 30 or more hours a week, and most retailers set their benefits bar exactly there, which is why Starbucks, not Walmart, ended up naming the strategy. Twenty hours a week of espresso duty buys you employer-sponsored group health insurance without going anywhere near the individual market. A handful of other large employers run similar part-time benefits schemes, but Starbucks remains the reference case.

The alternative is the ACA marketplace at HealthCare.gov, where premium tax credits reduce your monthly cost based on household income; households between 100% and 400% of the federal poverty level qualify for credits in every state. Early retirees with low taxable income can do well here, and some barista FIRE households deliberately manage their withdrawals to stay in credit territory. But the generosity of those credits moves with the politics in Washington, and pricing a 15-year plan on a subsidy Congress re-litigates is not everyone's idea of security. An employer plan at 20 hours a week is the more predictable bridge, which is exactly why people take the job.

So the real barista FIRE trade: you sell roughly 1,000 hours a year, and the wages are the smaller half of what you get back. The bigger half is the healthcare bridge from your quit date to Medicare at 65.

The Barista FIRE Maths: A Worked Example in Dollars

Start with the full FIRE benchmark. If your household spends $60,000 a year, the rule of 25 says you need $60,000 x 25 = $1,500,000 invested to retire outright.

Now add a part-time job paying $20,000 a year after tax. Your portfolio no longer has to fund $60,000 of spending, only the $40,000 gap:

- Full FIRE number: $60,000 x 25 = $1,500,000

- Barista FIRE number: ($60,000 - $20,000) x 25 = $1,000,000

That modest part-time income just removed $500,000 from the portfolio you need before you can quit. The general rule: every $1,000 of durable annual part-time earnings cuts about $25,000 off the requirement, because the portfolio is spared from generating that income at a 4% withdrawal rate. Even $500 a month, $6,000 a year, is worth $150,000 of portfolio you do not have to build. For someone saving $30,000 a year, that is five years of grinding handed back.

One caveat the rule of 25 hides: the full 25x discount assumes the side income runs forever. It will not; you will stop working at some point, usually by Medicare age. If you barista from 50 to 65 and then retire completely, your true requirement sits somewhere between the $1,000,000 and the $1,500,000, because the portfolio must eventually carry the whole load. This is what a proper barista FIRE calculator models: income that switches off at a chosen age rather than running to infinity. You can approximate it in two passes with our FI number calculator (also dollar-denominated for US visitors), and the rest of our US calculator suite covers the surrounding maths. The lazy 25x-the-gap version is a floor, not the answer.

And the number that matters more than any of these is your spending. Cut the $60,000 to $50,000 and the barista FIRE number falls to $750,000. The expense line does more work than the income line ever will.

Who Barista FIRE Suits

The classic candidate is mid-40s to mid-50s, with a portfolio somewhere between half and three-quarters of their full FIRE number, in a career they no longer want. Barista FIRE at 40 is possible on the same maths, but it stretches the healthcare bridge to 25 years and gives sequence risk more room to bite, so the numbers need to be more conservative.

It also suits people for whom full retirement is the wrong goal anyway. Twenty hours a week provides structure, colleagues and a reason to leave the house, which a surprising number of early retirees discover they miss badly. There is a strong overlap with burnout-driven FIRE: often the honest problem is not work itself but the specific job, the specific pressure, the specific hours. Barista FIRE lets you keep the tolerable parts of working life and evict the rest.

Who it does not suit: anyone whose spending already strains the plan, anyone banking on part-time work that may not exist in a downturn, and anyone below their coast FIRE milestone, for whom quitting now underfunds both the present and the future.

The Risks Nobody Prices In

Part-time work is the most disposable labour in the economy. Retail and food service hours are the first thing cut in a downturn. And because benefits eligibility usually hangs on maintaining average hours, a quiet quarter at your store can cost you the health plan, not just the wages. The plan's foundation is a category of employment with the least security American labour law has to offer.

The benefit is policy, not statute. Starbucks' 20-hour threshold is a company decision, and company decisions get reversed. A future CEO trimming costs could lift the threshold or cut the subsidy with a memo. A national health service cannot be rewritten by one employer's benefits team; this can. If your 15-year plan rests on a perk, you need a plan B, which in practice means the ACA marketplace and its own political weather.

The nastiest feature is correlation. The recession that cuts your barista hours is the same recession that drops your portfolio 30%. Your income insurance and your investments can fail in the same quarter, which is precisely when you need both.

Sequence of returns risk still applies. You are withdrawing from a portfolio decades before a conventional retirement. A bad crash in the first few years of withdrawals does damage that average returns never repair. Part-time income softens this compared with full FIRE, because your withdrawal rate is lower, but you also started with a smaller pot. The risk is reduced, not removed.

Careers do not keep, either. If barista FIRE fails five years in, the fallback is returning to your old profession, and five years out of a professional field is a long time. Price in the possibility that the door you close does not reopen at the same salary.

The Irony at the Heart of Barista FIRE

Step back and look at what this strategy actually is. Millions of Americans who have saved diligently for decades, who hold portfolios most households will never accumulate, still cannot leave jobs they hate without securing a replacement employer, because walking away means walking away from the insurance card.

Barista FIRE is a rational, even clever, individual response to that arrangement. But the arrangement itself deserves naming: the United States ties healthcare to employment, and the result is that labour stays put out of fear of medical bankruptcy rather than loyalty or pay. Economists call it job lock. Workers call it the reason they are still there. An entire FIRE strategy, calculators and subreddits and all, exists to arbitrage a 20-hour benefits threshold at a coffee chain, and everyone involved treats this as normal.

From the UK side of the Atlantic the strangeness is easier to see. British FIRE has plenty of its own headwinds - lower salaries, heavier tax on the way up - but "how do I stay insured until 65" appears in precisely zero UK FIRE spreadsheets. That line item is a policy choice, not a law of nature. Barista FIRE is what resourceful people build when the policy fails them. Fair play to the builders. The blueprint is still an indictment.

Further reading: Kristy Shen and Bryce Leung's Quit Like a Millionaire is the best account of what quitting years early actually takes, healthcare planning included, and Bill Perkins' Die With Zero is the argument for buying back your best years instead of grinding toward a bigger number. Disclosure: affiliate links - we may earn a small commission if you buy through them, at no cost to you.

Frequently Asked Questions

How much money do you need to barista FIRE?

Take your annual spending, subtract your expected after-tax part-time income, and multiply the gap by 25 - the inverse of the 4% withdrawal rule. A household spending $60,000 with $20,000 of part-time income needs about $1,000,000 invested, several times the median American couple's retirement savings. Treat that as a floor: the shortcut assumes the income continues indefinitely, so if you plan to stop working before the portfolio catches up, you need a buffer above it.

What is the difference between barista FIRE and coast FIRE?

Coast FIRE means you have invested enough that compounding alone will fund a normal-age retirement, but you keep working full-time to pay today's bills. Barista FIRE means you have actually quit full-time work and are living on portfolio withdrawals plus part-time income now. Coast changes how you save; barista changes how you live. Our coast FIRE guide covers the milestone version in detail.

Does Starbucks really give health insurance to part-time employees?

Yes. Under Starbucks' published benefits eligibility rules, part-time US mainland partners qualify for medical, dental and vision cover after 240 paid hours over three consecutive months, and keep it with 520 paid hours per six-month period - an average of 20 hours a week. That threshold, well below the 30-hour line at which federal law obliges large employers to offer coverage, is why the strategy carries the Starbucks job title rather than any other.

What jobs work for barista FIRE?

Any part-time work that reliably covers your income gap qualifies, from freelancing to seasonal work. But jobs carrying employer health benefits at part-time hours are the gold standard for Americans under 65, because they solve the healthcare bridge and the income gap in one move. If your part-time work has no benefits, price an ACA marketplace plan into your spending before you resign anything.

Can you barista FIRE at 40?

The maths works at any age, but at 40 you are underwriting a 25-year healthcare bridge to Medicare at 65 and giving market downturns far more time to interact with your withdrawals. Most people who barista FIRE that early either run a lower withdrawal rate, keep spending lean, or treat the part-time phase as semi-permanent rather than a short bridge.

What happens if you lose your part-time job?

Your income gap reopens and, if the job carried your health plan, so does the healthcare gap. The fallbacks are finding another benefits-eligible role, buying a marketplace plan at HealthCare.gov (premium tax credits based on your household income can cut the cost substantially), or drawing harder on the portfolio for a while. Barista FIRE plans should be stress-tested against exactly this scenario before you hand in your notice.

You can find more of our US-edition writing at /us/articles.

Sources

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all