Should You Ever Lend Money to Family?

Lend £5,000 to a relative and you become their creditor at every family dinner until it is repaid. Gift what you can afford or say no. The loan is the option that costs you both.

Cite this article

Freedom Isn't Free (2026) Should You Ever Lend Money to Family?. Available at: https://freedomisntfree.co.uk/articles/should-you-lend-money-to-family-uk (Accessed: 4 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- A family loan changes your role, not just your bank balance: you become your relative's creditor at every gathering until it is repaid, and most families never price that in.

- The clean rule: gift what you can afford to lose, or say no. A smaller gift beats a bigger loan almost every time.

- The loan itself is not taxed in the UK, but any interest you charge is taxable savings income, and an unpaid loan still counts as part of your estate for inheritance tax.

- If you insist on lending, write it down: amount, repayment schedule, what happens if things go wrong. Paperwork protects the relationship as much as the money.

| Annual exemption | £3,000 per tax year, one unused year carries forward |

| Small gifts | £250 per person, any number of people |

| Wedding gift to your child | £5,000 |

| Wedding gift to a grandchild | £2,500 |

| Regular gifts from spare income | Unlimited, if they do not cut your standard of living |

| Anything bigger | IHT-free if you live 7 more years |

Giving money to family: UK tax-free gift allowances (2026/27)

Should You Ever Lend Money to Family?

Lending money to family is one of those questions where the standard advice - "only lend what you can afford to lose" - quietly concedes the whole argument. If you can afford to lose it, you can afford to gift it. If you cannot afford to lose it, you cannot afford to lend it to someone you will be sharing Christmas with for the next forty years. The loan is the one option on the table that is worse than both alternatives, and it is somehow the default.

So here is the fork this article exists to settle. When your sister, your son or your uncle asks for money, you have three doors: lend it, gift it, or decline. I am going to argue, with the numbers and the UK tax rules on the table, that door one is almost always the wrong one. Then, as ever, the floor is yours.

Contents

- What a family loan really is

- The rule: gift it, or say no

- The tax rules on lending and gifting money to family

- If you do lend: write it down

- How to say no without breaking anything

- Where I land on lending money to family

What a family loan really is

A family loan looks like a financial transaction. It is really a role change. The moment the transfer lands, you stop being just a brother, a mum or a mate, and you become a creditor - and you stay one at every birthday, every Sunday lunch and every group chat until the money comes back. Nobody prices that in, because the price does not appear on any statement.

Look at what you have actually written, in commercial terms. You have issued an unsecured loan, usually at 0% interest, to a borrower a bank may already have turned down, with no credit check, no repayment schedule, no default terms, and a collections process that consists of ruining Boxing Day. A commercial lender would not touch that deal at any interest rate you would be comfortable charging a relative. What your relative is really asking you to do is absorb a risk the market has already refused, for free, out of love.

And the repayment dynamics are shaped against you. A bank chases arrears mechanically; you have to choose, every month, between raising the subject and keeping the peace. Most people keep the peace. The debt goes quiet, then stale, then unmentionable. Watch what "lent" money does over time: it slowly becomes a gift anyway, just one that arrives with a residue of resentment on both sides instead of goodwill. That is the trade you are really weighing: a gift with thanks now, or the same gift with a grudge later.

The rule: gift it, or say no

The affordability test cuts cleanly both ways, and it is the whole framework.

If losing the money would genuinely hurt you - it is your emergency fund, your ISA contributions, your own mortgage overpayment - then you cannot afford this, and the answer is no. That no is a verdict on your own position, not on their character: your own house has to be fireproof before you hand out buckets of water. A loan that sinks your own finances helps nobody; it just moves the crisis one household sideways.

If losing the money would not hurt you, gift it. Openly, cleanly, with no invoice attached. A gift settles everything on day one: no ledger, no creditor role, no awkwardness compounding at family occasions. If the full amount asked is too big to gift, gift the amount that is not. "I can't do £5,000, but here is £1,500 and it is yours" is a better outcome for both of you than £5,000 of slow-burning IOU. A smaller gift beats a bigger loan almost every time.

The honest case for lending anyway deserves its hearing. Family lending is how plenty of people escape genuinely predatory alternatives - the poverty premium is real, and a 0% family loan beats doorstep credit charging 50%-plus APR by a distance that can change a life. Deposit help is the other big one: family gifts and loans put £9.6 billion into first-time buyer deposits in 2024 (Savills), because that is what the housing market now costs - the full argument about the Bank of Mum and Dad is its own article. If a structured family loan is the difference between your kid renting forever and owning, the calculation genuinely changes. I am not pretending those cases away. I am saying they are the exceptions, they deserve paperwork, and the everyday "can you sort me out until things pick up" case is not one of them.

The tax rules on lending and gifting money to family

The good news first: the UK does not tax family generosity anywhere near as hard as people fear, and there is no gift tax.

Lending itself is tax-free. There is no tax on making a loan, no cap on how much you can lend a family member, and repayments of the amount you lent are not income. HMRC only takes an interest when you do: any interest you charge is taxable savings income. It counts against your Personal Savings Allowance - £1,000 a year for basic-rate taxpayers, £500 at higher rate - and above that it goes on a Self Assessment return. In practice most family loans are interest-free and generate no tax at all.

Gifts are simpler than the folklore says. You can give away £3,000 a year free of inheritance tax (the annual exemption, and one unused year carries forward, so a couple who skipped last year can hand over £12,000 between them). On top of that: unlimited £250 small gifts to different people, £5,000 for your child's wedding, £2,500 for a grandchild's, and unlimited regular gifts out of spare income if they do not dent your standard of living.

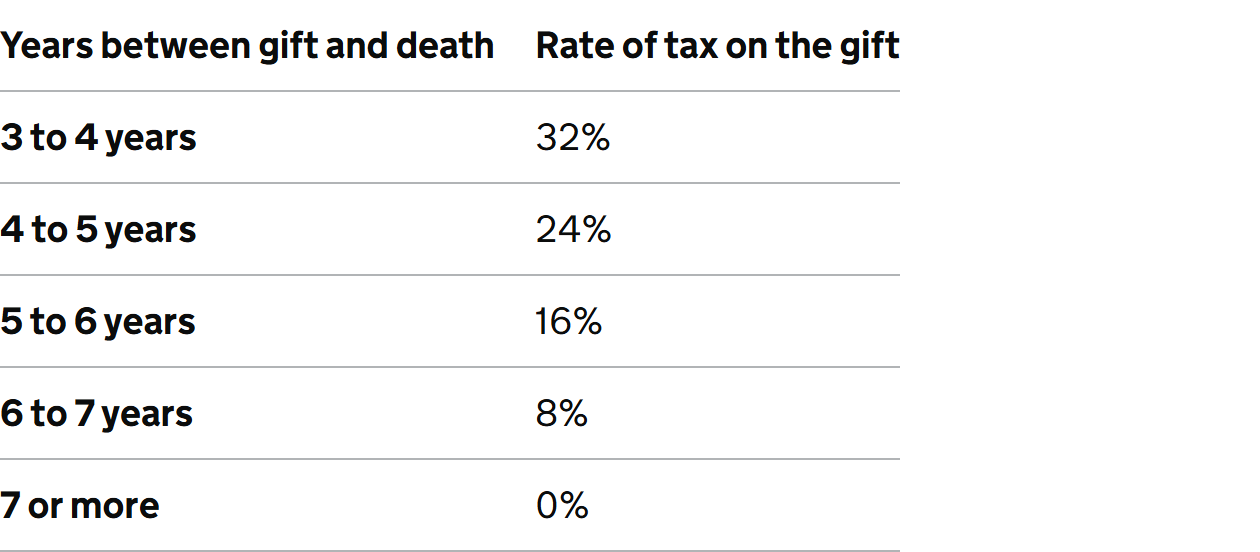

Bigger gifts run on the 7-year rule. Give £20,000 to your daughter and it is a "potentially exempt transfer": survive seven years and it never troubles inheritance tax at all. Die sooner and it counts back into your estate, but tax and taper relief only bite on gifts above the £325,000 nil-rate band. For an ordinary family, a five-figure gift almost never produces an actual IHT bill.

The 7-year rule is a large-estate problem wearing an everyman costume.

The 7-year rule is a large-estate problem wearing an everyman costume.

The loan trap inside your estate. Here is the wrinkle the lend-don't-gift crowd misses: an outstanding loan is an asset you still own. If you die with £15,000 still owed by your nephew, that £15,000 sits inside your estate for IHT, and your executors are supposed to collect it - from your nephew, while grieving. Waive the loan in your lifetime and the waiver is itself a gift, with the same 7-year clock. Lending does not avoid the estate questions a gift raises. It defers them to the worst possible moment and hands them to someone else.

If you do lend: write it down

If the case really is one of the exceptions - the deposit, the escape from a predatory lender, the bridge with a defined end - then do it like an adult transaction, precisely because the relationship matters.

Put it in writing. A one-page agreement: the amount, the repayment schedule, what happens if a payment is missed, whether interest applies. Paperwork looks like faff and works like kindness - it removes the ambiguity that curdles relationships, and both sides get to point at the document instead of at each other. Under the Limitation Act 1980 you generally have six years to enforce a simple contract debt in court, but treat that as trivia: the real function of the document is that you never get anywhere near a courtroom.

Never leave a deposit loan undeclared. If the money is helping with a house purchase, the mortgage lender will ask directly whether it is a gift or a loan, because a loan affects affordability and gets factored into what they will lend. Calling a loan a gift on a mortgage application is fraud. If it is a loan, declare it and accept the smaller mortgage; if you want the full borrowing power for them, it needs to genuinely be a gift, with a signed letter saying so.

Agree the failure mode up front. The single most useful sentence in a family loan conversation: "if it all goes wrong and you can't repay, we write it off and never mention it again." Say it before the transfer. You have converted the worst-case scenario from a feud into a plan, and you have quietly run the affordability test out loud - because if you cannot say that sentence and mean it, you have just discovered you should not be lending.

How to say no without breaking anything

Declining is a skill, and it is worth doing well, because "no" said badly costs relationships almost as reliably as a soured loan.

Blame the plan, not the person. "All my money is locked away in my pension and ISA and I don't keep spare cash" is true for most people reading this site and closes the conversation without a verdict on anyone's character. Better still, pair the no with something concrete: pay a specific bill directly, gift a smaller amount outright, or sit down with them and the actual problem. If the ask is really about unmanageable debt, the kindest thing you can hand over is not £2,000 - it is an evening helping them contact StepChange or Citizens Advice, whose debt advice is free and who can do things you cannot, like negotiating with creditors. Our guide to the UK's debt help options walks through what each route actually does. Money you lend into an unsolved debt problem does not solve it; it usually just adds you to the list of creditors being juggled.

Where I land on lending money to family

Gift it or refuse it. I have not yet found the family situation where a loan beats one of those two doors once you price in the relationship - and the relationship is the only asset in this whole transaction that cannot be rebuilt with overtime.

The money transfer that taught me most backs this up. In 2020 my boyfriend handed me £1,000 and insisted I pick some stocks with it, knowing full well I would probably lose money and learn something. I bought BP and IAG and lost about 10% in a few months. It was a gift priced as tuition, not a loan - there was never a ledger, never a repayment conversation, and what it bought was a lesson about stock picking that has been paying dividends ever since. I have called it the cheapest education I have ever had. That is what money moving inside a family looks like when it works: given freely, sized to be survivable, and settled the moment it changes hands.

So: protect your own finances first, gift what you can genuinely spare, decline what you cannot, and save the structured loan for the rare, documented, deposit-shaped exception. Your relative gets help that comes with no strings, and you get to stay what you were before they asked - family, not a creditor.

The floor is yours.

Debt: The First 5,000 Years - David Graeber - Graeber's anthropology of debt opens with exactly this problem: what happens to human relationships when an obligation between people who care about each other gets converted into a precise, enforceable number. Five thousand years of evidence that families and ledgers mix badly. (Affiliate link - we may earn a small commission at no extra cost to you.)

Frequently Asked Questions

Can you lend money to family tax-free in the UK?

Yes. There is no tax on making a loan and no tax when the amount you lent is repaid. Tax only enters if you charge interest: that interest is taxable savings income, counted against your Personal Savings Allowance (£1,000 basic rate, £500 higher rate). Most interest-free family loans create no tax at all.

How much money can you lend a family member in the UK?

There is no legal limit on how much you can lend a family member. Remember that an outstanding loan remains an asset of your estate for inheritance tax if you die before it is repaid, and writing a loan off during your lifetime counts as a gift under the normal 7-year rule.

Can I give my daughter £20,000?

Yes, and no tax is due when she receives it, because the UK has no gift tax. A £20,000 gift above your annual exemptions is a potentially exempt transfer: survive seven years and it falls outside your estate entirely. Even if you die sooner, inheritance tax only applies to gifts above the £325,000 nil-rate band, so for most families no tax ever arises.

What is the best way to lend money to a family member?

Put it in writing: the amount, a repayment schedule, whether interest applies and what happens if payments stop. Agree up front what you will both do if it cannot be repaid. If the money is going toward a house deposit, declare it honestly to the mortgage lender as a loan, or make it a genuine documented gift instead.

Is it a good idea to lend money to family?

Usually not. An informal family loan combines an unsecured 0% loan a bank would refuse with a collections process that runs through your personal relationships. Gifting what you can afford to lose, or declining and offering practical help instead, almost always leaves both the finances and the relationship in better shape.

This article is general information, not financial or tax advice. Inheritance tax rules, allowances and thresholds can change, and how they apply depends on your circumstances. Check the current rules on GOV.UK, and consider regulated advice for a large or complex estate. If you are struggling with debt, free help is available from StepChange and Citizens Advice.

Sources

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all