FCA Targeted Support: What It Means for UK Savers

Your pension provider can now legally suggest a contribution rate, a specific fund, a drawdown level. The FCA calls it 'targeted support'. It is not advice and it is not free of conflict. Here is what you get.

Cite this article

Freedom Isn't Free (2026) FCA Targeted Support: What It Means for UK Savers. Available at: https://freedomisntfree.co.uk/articles/fca-targeted-support-uk (Accessed: 15 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- FCA targeted support went live on 6 April 2026. Authorised firms can now make ready-made suggestions to groups of consumers who share similar circumstances, sitting between generic guidance and full regulated advice.

- The FCA estimates 23 million UK adults are underserved by the current advice market. Fewer than 1 in 10 adults received regulated financial advice last year, mainly because it is priced out of reach.

- Targeted support is not advice. The firm making the suggestion is usually the firm selling the product. There is no personalised assessment of your full circumstances, and the conflict of interest is baked in.

- Used well, it can nudge under-savers and over-cautious investors in the right direction. Used badly, it is regulated marketing. The Consumer Duty, FOS and FSCS still apply, but the responsibility to think it through is yours.

Guidance vs targeted support vs regulated advice

| Feature | Generic guidance | Targeted support | Regulated advice |

|---|---|---|---|

| Personalised to you | No | Group-level only | Yes, full fact-find |

| Typical cost to you | £0 | £0 (firm absorbs) | £13k to £16k over 5 years |

| Firm liability | Low | Consumer Duty + FOS + FSCS | Full suitability liability |

| Live since | Always | 6 April 2026 | Pre-2012 (post-RDR rules apply) |

FCA estimates 23 million UK adults are underserved by the current advice market.

FCA Targeted Support: What It Means for UK Savers

The FCA targeted support regime went live on 6 April 2026 and is the biggest change to how UK consumers get help with their money in a generation. For the first time, authorised firms can make specific suggestions about your pension or your investments without crossing the line into regulated financial advice. No fact-find, no full assessment of your circumstances, no four-figure invoice.

The regulator's intent is to close the so-called advice gap, which is the chasm between the 9% of adults who pay for regulated advice and the 91% who do not. Whether that goal is met depends almost entirely on how firms choose to use the new permission. This article is a plain explainer of what the regime is, what it changes, and where it falls short.

Contents

- What FCA targeted support actually is

- How it differs from advice and guidance

- What firms can now suggest

- The advice gap targeted support is trying to close

- Where the conflict of interest sits

- Consumer protections that still apply

- How to use targeted support without getting played

- Frequently Asked Questions

What FCA targeted support actually is

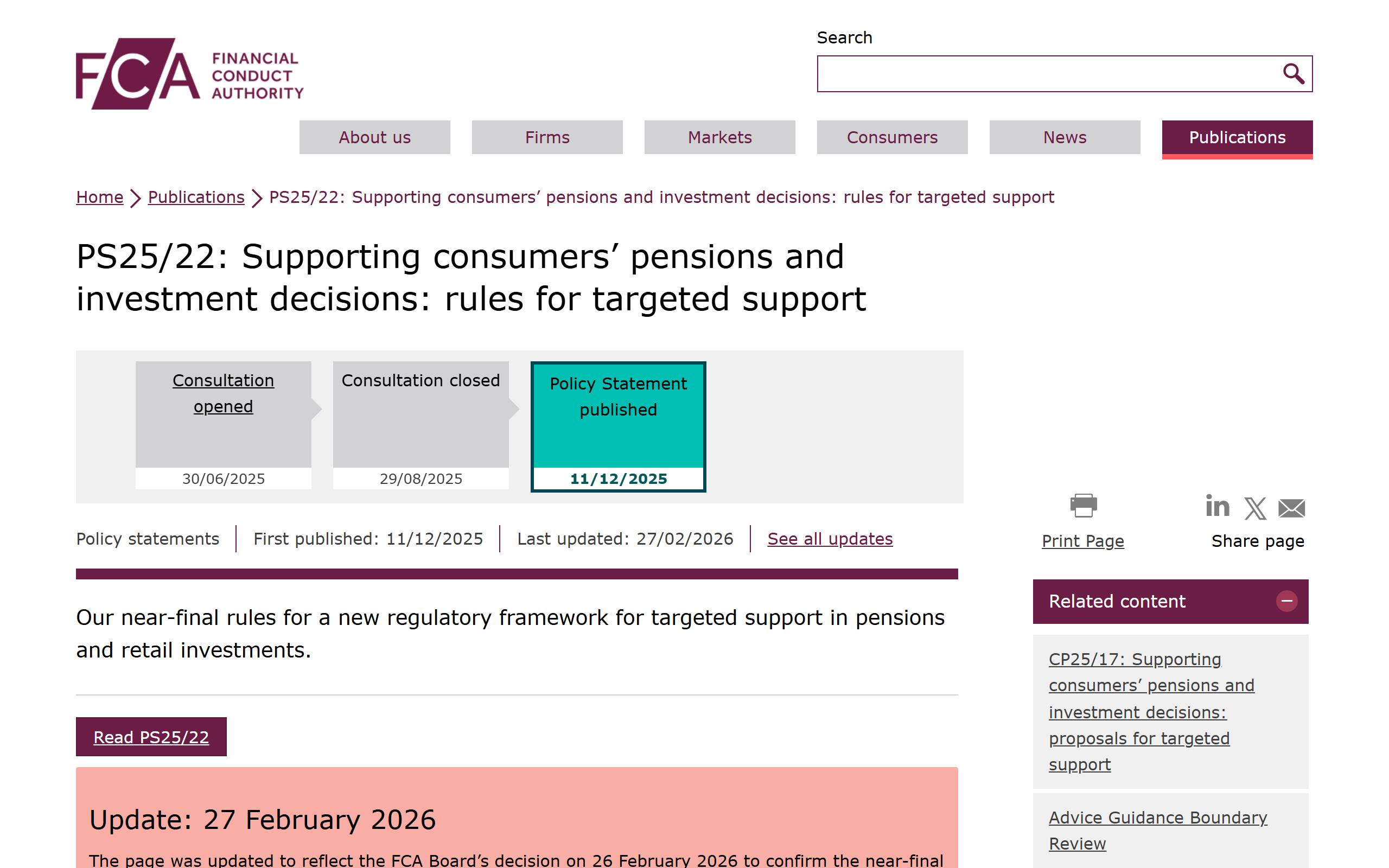

Targeted support is a new regulated activity introduced under the FCA's Advice Guidance Boundary Review. The policy statement, PS25/22, was published in December 2025, the rules were finalised by the FCA Board on 26 February 2026, and the regime went live on 6 April 2026. Firms could begin applying for permission from 2 March 2026, and the FCA opened a pre-application support service to keep the queue moving.

The core idea is simple. An authorised firm identifies a group of customers with shared characteristics, designs a "ready-made suggestion" that fits that group, and delivers it. The customer does not need to disclose their full financial picture, the firm does not need to conduct a full suitability assessment, and the cost to the customer is typically zero because the firm absorbs it as part of its service model.

It applies to pensions and retail investments only. Mortgages, insurance, debt, and tax sit outside the scope.

How it differs from advice and guidance

UK financial help has historically sat in two boxes. Guidance is generic information, such as factsheets from MoneyHelper or a workplace pension provider's general literature, that does not recommend a specific course of action. Regulated financial advice is a personalised recommendation, made after a fact-find, by a firm that takes responsibility for whether the recommendation suits you. Advice is expensive. Recent FCA research put the cost of advice for a £250,000 portfolio at between £13,375 and £16,250 over five years, which is a non-starter for most people.

Targeted support sits in between. The firm identifies a group ("customers aged 50 to 55 with a defined contribution pot below £100,000 who are paying in less than 8%", for example) and offers that group a suggestion ("consider increasing your contribution rate to 10%"). The suggestion is not personal to you, but it is more specific than generic guidance, and the firm has to be able to justify why the group definition and the suggestion make sense.

The legal nuance is that targeted support is not a "personal recommendation" in the regulated-advice sense. That is what allows it to skip the full suitability assessment. The customer is told, in plain language, that the suggestion is based on group characteristics rather than their own complete circumstances.

What firms can now suggest

The FCA's published examples give a flavour of what the regime is intended to cover. The three big use cases are:

- Under-saving for retirement. A workplace pension provider can identify members who are below an age-appropriate contribution rate and suggest a higher one. Today, the same provider can only point you at a contribution calculator and hope you find your way. The default contribution rates under workplace pension auto-enrolment sit well below what most workers need to retire comfortably, and targeted support is the first regulated tool that lets providers say so directly.

- Cash sitting idle when it could be invested. The FCA notes that around 7 million UK adults hold £10,000 or more in cash savings but are not engaged with investments. A bank or investment platform can now suggest, to a group with that profile, that some of the cash be moved into a stocks and shares ISA or general investment account.

- Unsustainable pension drawdown. A retiree drawing 8% a year from a moderate-risk drawdown pot is on track to run out of money. A pension provider can now identify that group and suggest a lower drawdown rate or a different fund mix. The maths behind a sustainable rate is set out in our pension drawdown guide.

What firms cannot do under targeted support is replicate the breadth of regulated advice. They cannot tell you whether the suggestion is suitable for your full situation. They cannot weigh your debts, your dependants, your tax position, your other pensions, or your wider goals. The Consumer Duty requires them to make the limitations clear, but the limitations are real.

The advice gap targeted support is trying to close

The FCA's own Financial Lives survey is the clearest description of the problem. Roughly 23 million UK adults are underserved by the current advice market, in the sense that they have decisions to make about money but get neither professional advice nor enough engagement with their providers to act on those decisions. The cost of regulated advice has risen, the post-Retail Distribution Review world abolished commission-funded advice for most customers, and firms have retreated to higher-net-worth segments where the economics work.

The FCA estimates that over the next decade, at least 18 million people could be offered help under the new regime. That is a meaningful number if it lands. The risk is that the actual lift is much smaller because the firms with the easiest path to scale, the largest workplace pension providers and platforms, also have the strongest incentive to keep their suggestions narrowly aligned with what they sell.

Where the conflict of interest sits

This is the part that does not get enough airtime. The firms delivering targeted support are the firms selling you products. Your workplace pension provider has a list of funds it manages. Your platform has a default portfolio it earns a margin on. The bank running the cash-to-investments suggestion has its own stocks and shares ISA to sell you.

The FCA is not naive about this. The rules require firms to demonstrate that targeted support delivers good outcomes under the Consumer Duty, which means firms cannot simply push customers toward their highest-margin product and call it a suggestion. But the practical reality is that targeted support will, by design, route you toward the suggesting firm's own product line, because that is the only product line that firm can offer.

If your workplace pension provider tells you "people like you should be paying in 10%", that is good guidance, broadly. If it then tells you "and you should be in our medium-risk lifestyle default", you are now being marketed to inside a regulated wrapper. The suggestion may still be reasonable, but it is not independent advice. It is informed sales.

For most people, most of the time, that is fine. The default funds offered by major UK workplace pension providers are mostly competent, low-cost, age-appropriate strategies. The problem comes at the edges, where someone with a more complex situation, such as multiple pensions, a partner with very different earnings, a mortgage strategy, or a planned career break, gets a one-size-fits-the-group suggestion and treats it as a plan. It is not.

Consumer protections that still apply

Targeted support is a regulated activity, and the standard consumer protections apply:

- The Consumer Duty. Firms must monitor outcomes and compensate where targeted support causes harm. This is the meaningful backstop.

- The Financial Ombudsman Service (FOS). Complaints about targeted support can be taken to the FOS in the same way as complaints about regulated advice.

- The Financial Services Compensation Scheme (FSCS). If a firm fails owing customers money relating to targeted support, FSCS protection applies under the existing investment business limits (currently up to £85,000 per person per firm). The FSCS protection rules work the same way as they do for any other regulated investment activity.

What customers do not get is the higher bar of regulated-advice liability. If you act on a targeted-support suggestion and it turns out to be poorly suited to your situation, the firm's defence will usually be that you were told the suggestion was based on group characteristics, not your individual circumstances, and you chose to act on it anyway. That defence is harder to mount for full regulated advice, which is one of the reasons regulated advice is expensive.

How to use targeted support without getting played

The honest framing of targeted support is that it is regulated, but lightly regulated, marketing. It is better than no help, worse than real advice, and most useful when used as a prompt rather than as a plan. A few rules of thumb:

- Treat suggestions as the start of a conversation, not the end of one. "Your provider thinks people like you should pay in 10% rather than 5%" is a good prompt to look at your own numbers and decide whether 10% is right for you. It is not a decision in itself.

- Cross-check the product suggestion. If the suggestion is to move into a specific fund, look at the ongoing charges figure, the asset allocation, and what comparable funds elsewhere look like. A 0.4% all-world tracker on one platform is broadly the same investment as a 0.4% all-world tracker on another.

- Check what is not being suggested. Your workplace pension provider will not suggest you move money to a different provider, because that is not in its commercial interest, but for some people it is the right answer.

- Use the free MoneyHelper service for a second opinion. MoneyHelper is funded by the FCA's levy on the industry, it does not sell anything, and it provides genuinely independent guidance. If a targeted-support suggestion lands in your inbox and you are not sure, that is the place to sanity-check it.

- Pay for advice if the decision is big enough. For decisions on the scale of a pension transfer, a defined benefit conversion, a tax-band planning question, or anything involving an inheritance, the cost of a single one-off advice session from an independent financial adviser is small compared to the cost of getting the decision wrong. Targeted support is not built for those decisions.

The right way to think about the regime is that it makes the bottom half of the advice problem slightly less bad without solving the top half. For most workers in defined contribution pensions, slightly less bad is still a real improvement on what they had on 5 April 2026. For everyone else, the calculus is unchanged.

Frequently Asked Questions

When did FCA targeted support start?

The rules went live on 6 April 2026, after the FCA Board confirmed the final policy statement on 26 February 2026. Firms have been able to apply for permission since 2 March 2026, and the regulator opened a pre-application support service to clear the initial queue.

Is targeted support free?

For consumers, in most cases, yes. The firms providing targeted support absorb the cost as part of their service model, on the basis that better-engaged customers are more profitable customers over time. There is no equivalent of the four-figure fee that regulated advice usually carries.

Does targeted support replace financial advice?

No. Targeted support is designed to fill the gap below the level where regulated advice makes sense. If you have a complex situation involving multiple pensions, tax planning, defined benefit transfers, inheritance, or significant assets, you still need regulated advice. The two regimes are intended to coexist.

What if a targeted support suggestion turns out to be wrong for me?

You can complain to the firm, and if you are not satisfied, escalate to the Financial Ombudsman Service. The Consumer Duty requires firms to monitor outcomes and provide redress where targeted support causes harm. FSCS protection also applies if the firm itself fails. The bar for redress is lower than it is for regulated advice, but the protections are real.

Why now? Why didn't the FCA do this years ago?

The advice gap has been understood for at least a decade, but the legal definition of a "personal recommendation" under MiFID II made it hard for firms to do anything between generic guidance and full advice without falling foul of suitability rules. The Advice Guidance Boundary Review, launched in 2023, was the work that produced targeted support as a new regulated category. The political appetite for reform sharpened after the 2024 pension freedoms reviews exposed how many drawdown customers were on track to run out of money.

Should I trust a suggestion from my pension provider?

You should treat it as informed input, not a final answer. The provider knows enough about your pension to make a sensible group-level suggestion, but it does not know your full financial picture, and it has a commercial interest in you staying with its products. Use the suggestion as a prompt to check your own numbers, not as a decision in itself.

Further Reading:

Smarter Investing - Tim Hale - The plain-English UK guide to building a low-cost portfolio yourself, which is the surest defence against being routed into the suggesting firm's house funds. (Affiliate link - we may earn a small commission at no extra cost to you.)

This article is educational commentary on the FCA's targeted support regime and is not regulated financial advice. Capital is at risk when investing, and tax and pension rules can change. For decisions specific to your circumstances, speak to an FCA-authorised independent financial adviser.

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all