FSCS Protection UK: What's Actually Covered Up to £120k?

Two of your accounts. Two different brand names. One banking licence. FSCS pays out once per licence, not once per brand. The trap that catches savers the morning a bank actually fails.

Cite this article

Freedom Isn't Free (2026) FSCS Protection UK: What's Actually Covered Up to £120k?. Available at: https://freedomisntfree.co.uk/articles/fscs-protection-uk-guide (Accessed: 29 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- FSCS protects up to £120,000 of cash deposits per person, per banking licence (raised from £85,000 on 1 December 2025) - not per account, brand, or product

- Several "different" UK banks share licences (HSBC + First Direct, Lloyds + Halifax + Bank of Scotland) - check the FSCS register

- Investment platforms have separate £85,000 protection (unchanged) covering custody/admin failures, but underlying assets are usually held in your name and outside the platform anyway

- Pensions and life policies have their own FSCS rules with no cap on insurance contracts and 100% protection for pension annuities

FSCS protection limits by product type

| Product | Limit | Per | Notes |

|---|---|---|---|

| Cash deposits | £120,000 | Person per banking licence | Raised from £85k on 1 Dec 2025. Joint accounts: £240,000 |

| Temporary high balance | £1,000,000 | 6 months | House sale, inheritance, divorce |

| Investment platform | £85,000 | Person per firm | Unchanged. Underlying assets usually safe regardless |

| Pension annuity | 100% (no cap) | Person per provider | Strongest FSCS rule |

| Long-term insurance | 100% (no cap) | Person per policy | Life, income protection |

| General insurance | 90% (no cap) | Per claim | Motor, home, travel |

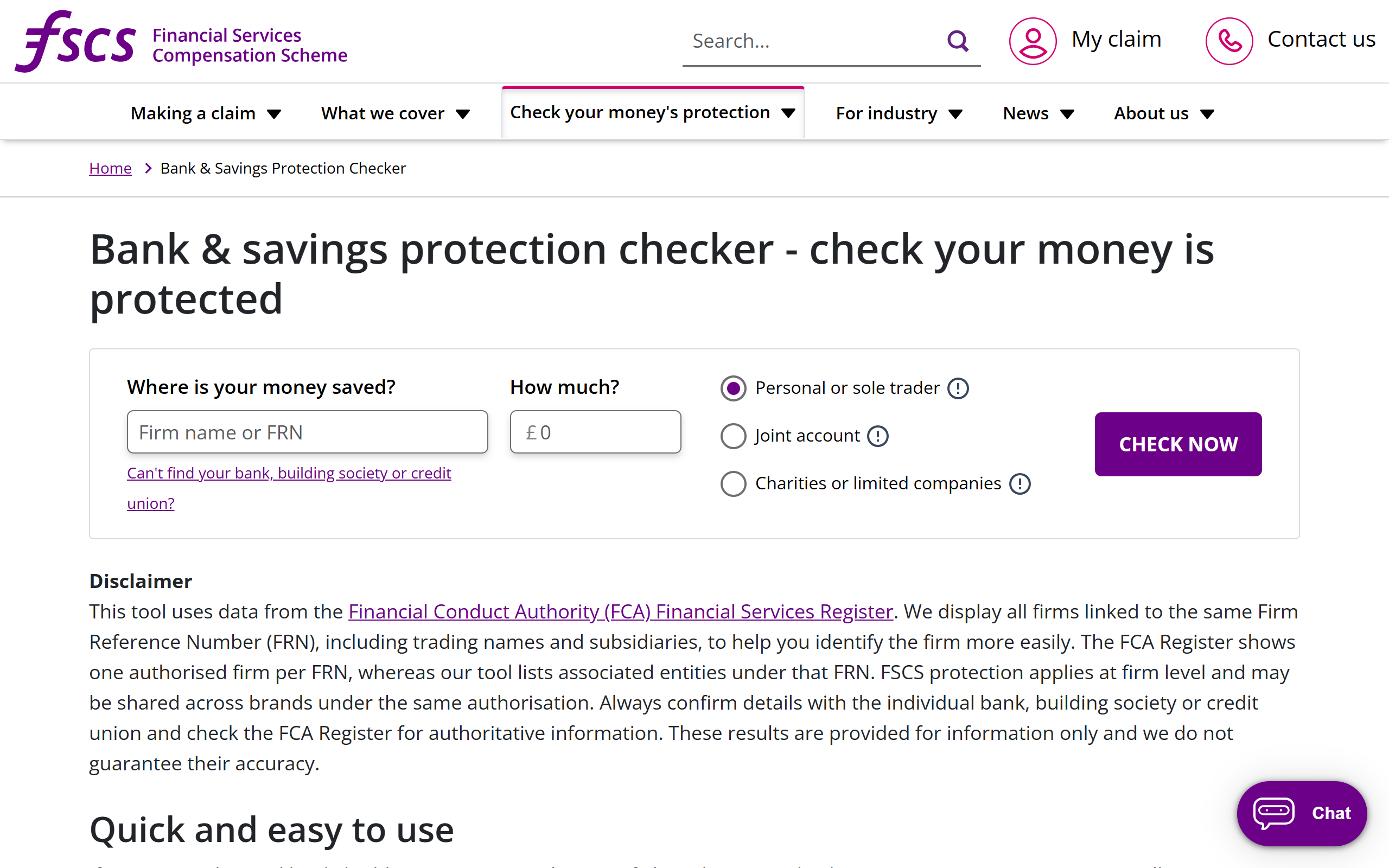

Source: FSCS.org.uk. Always check the FSCS register for licence sharing between brands.

FSCS Protection UK: What's Actually Covered Up to £120k?

The Financial Services Compensation Scheme is the UK's safety net for when banks, building societies, investment firms, insurers, or pension providers fail. The cash deposit limit rose from £85,000 to £120,000 on 1 December 2025, and most savers still quote the old number. It is also widely understood as "£120,000 per account", which is wrong in several ways and has historically cost depositors money in real failures.

This guide covers what FSCS actually protects after the December 2025 uplift, the per-banking-licence rule that catches savers out, how the rules differ between banking, investing, and insurance, and the practical steps for anyone holding more than £120,000 in cash.

Contents

- What FSCS does

- The £120,000 cash deposit rule

- Banks that share a single FSCS licence

- Investment platform protection (different rules)

- Pensions and insurance protection

- When FSCS does not help

- Frequently asked questions

What FSCS Does

FSCS is funded by levies on UK financial firms and pays out compensation when an authorised firm fails. It protects:

- Cash deposits at UK banks, building societies, and credit unions

- Investments held on UK-authorised investment platforms

- Pension contracts (annuities, drawdown contracts, occupational schemes)

- Insurance policies

- Mortgage advice and home finance

- General insurance claims

FSCS does not protect against investment losses, market falls, or your own bad decisions. If your global tracker drops 30%, FSCS does not compensate you. It pays out only when the firm itself fails - administrative collapse, fraud, or insolvency.

The £120,000 Cash Deposit Rule

For cash deposits, FSCS protects up to £120,000 per person, per banking licence, raised from £85,000 on 1 December 2025. The key qualifier is still "per banking licence" - not per account, not per brand.

A few important details:

- Joint accounts get £240,000 protection (£120k per joint holder)

- Temporary high balances (e.g. proceeds from selling a house) can be protected up to £1m for 6 months while you arrange more permanent storage

- Money held by minors counts towards the parent's limit only if the parent is the legal owner of the account

- The £120,000 limit applies even if you have multiple accounts at the same bank

What this means in practice: if you have £150,000 in an easy-access savings account at one bank, £30,000 of it is uninsured. If the bank fails, FSCS pays out £120,000 and you lose the rest.

Banks That Share a Single FSCS Licence

The trap that catches savers is that many "different" UK banks operate under the same banking licence, sharing one £120,000 limit between them. Examples in 2026:

- HSBC and First Direct: same licence

- Lloyds, Halifax, and Bank of Scotland: same licence

- Yorkshire Building Society, Norwich & Peterborough, and Egg: same licence

- Coventry Building Society and Stroud & Swindon: same licence

If you have £80,000 with HSBC and £60,000 with First Direct, you have £140,000 with one banking licence. Only £120,000 is FSCS-protected.

The FSCS register lets you check which banks share a licence. Always check before splitting savings between two "different" banks for safety. Genuinely separate banking groups (Barclays, Lloyds, NatWest, HSBC, Santander, and the various challenger banks) generally have their own licences.

Investment Platform Protection (Different Rules)

For investment platforms (Trading 212, Vanguard, Hargreaves Lansdown, AJ Bell, Interactive Investor, etc.), the FSCS rules are separate from banking deposit protection. The investment limit did not move on 1 December 2025 - it stayed at £85,000. Only the deposit limit at banks, building societies and credit unions rose.

Two layers of protection apply:

- Custody of your assets: FCA rules require investment platforms to hold your shares, funds, and ETFs in a separate "client money" structure, distinct from the platform's own assets. If the platform fails, the underlying investments are still legally yours and can be transferred to a new platform.

- FSCS top-up: covers up to £85,000 of any losses caused by the platform's failure - typically administrative shortfalls, fraud, or fees during the wind-down. Not market losses on your investments.

Practical implication: a £200,000 portfolio on a platform that fails should be returned to you in full because the underlying investments are not part of the platform's assets. The £85,000 cap only matters if there is a custody failure - rare but documented in cases like Beaufort Securities (2018).

For most retail investors, investment platform risk is far smaller than banking deposit risk. You can hold a £500,000 portfolio at one platform with relatively low concern, but you should not hold £300,000 of cash in one savings account.

Pensions and Insurance Protection

Pensions and insurance contracts get more generous FSCS treatment than cash:

- Pension annuities: 100% protection, no cap. If your annuity provider goes bust, your full income is protected.

- Personal pensions and SIPPs: 100% protection on the deposit/insurance portion, but underlying investments are subject to the same custody rules as investment platforms.

- Life insurance and long-term insurance contracts: 100% protection, no cap.

- General insurance (motor, home, travel): 90% protection, no cap, on claims arising before the insurer's failure.

The 100% no-cap protection on pension annuities is one of the strongest FSCS rules and is often a factor in deciding annuity vs drawdown for retirees worried about provider risk.

When FSCS Does Not Help

FSCS is not a guarantee against everything that can go wrong with UK finance:

- Market losses: not covered. A 30% market crash is not a "failure" event.

- Crypto and unauthorised products: outside the FCA regulatory perimeter, no FSCS protection. Crypto exchanges, peer-to-peer lending platforms, and offshore providers are typically outside FSCS regardless of how prominent their UK marketing is.

- Foreign banks operating in the UK: protection depends on whether they operate via a UK subsidiary (FSCS applies) or a UK branch (their home country's protection applies). Most large foreign banks in the UK are subsidiaries with full FSCS coverage.

- Money in wrong-named accounts: FSCS protects the named account holder. Money sitting in a friend's account, in business accounts where you are a beneficial but not legal owner, or in unauthorised intermediaries, may not be covered.

- Mortgage fraud or solicitor fraud: separate compensation schemes (CIPS, SRA) cover these, not FSCS.

For more on managing financial risk holistically, the emergency fund article covers cash positioning for resilience, and the best UK investment platform comparison discusses platform-specific protection.

Frequently Asked Questions

How much money does FSCS protect in the UK?

£120,000 per person per banking licence for cash deposits at banks, building societies and credit unions (raised from £85,000 on 1 December 2025). Joint accounts get £240,000. Investment platforms still cap at £85,000 (that limit did not move). Pensions and insurance policies have separate rules with different limits, generally with 100% protection on annuity income and long-term insurance contracts.

Are joint accounts protected up to £240,000?

Yes. Each joint account holder gets their own £120,000 protection on the joint account, totalling £240,000. This is in addition to any sole-account protection each holder has at the same banking licence.

Are investment ISAs protected by FSCS?

The cash portion of a Stocks and Shares ISA held at a banking licence is covered up to £120,000 (combined with other deposits at that bank). The investment portion is held in your name by the platform's custodian and is not part of the cash deposit limit. FSCS top-up to £85,000 covers any administrative loss if the investment platform itself fails - that £85k investment-business limit did not move on 1 December 2025.

What happens if my pension provider goes bust?

For annuities, 100% of your income is protected by FSCS with no cap. For SIPPs and personal pensions, the underlying investments are held separately from the provider's assets and should be transferred to a new provider. FSCS additionally covers up to £85,000 of any administrative shortfall (the investment-business limit, unchanged in December 2025).

Are challenger banks like Atom and Chip safe?

Yes, provided they have their own FCA authorisation and FSCS protection - which all the established UK challenger banks do. The £120,000 limit applies the same way as for high-street banks. Use the FSCS register to verify any unfamiliar provider's banking licence before depositing significant amounts.

Did FSCS protection rise in 2025?

Yes. On 1 December 2025 the deposit protection limit rose from £85,000 to £120,000 per eligible person, per bank, building society or credit union authorisation. The change applies to firms that failed after 30 November 2025. Joint accounts moved from £170,000 to £240,000. The investment-business limit stayed at £85,000.

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all