Premium Bonds vs Cash ISA: Which One Actually Pays More in 2026?

The Premium Bonds prize fund rate is 3.30%. Top Cash ISAs pay 4.62%. Yet half of all bondholders win less than the headline rate suggests. The maths is brutal and almost nobody explains it honestly.

Cite this article

Freedom Isn't Free (2026) Premium Bonds vs Cash ISA: Which One Actually Pays More in 2026?. Available at: https://freedomisntfree.co.uk/articles/premium-bonds-vs-cash-isa (Accessed: 15 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Premium Bonds pay a 3.30% prize fund rate (rising to 3.80% from the July 2026 draw). Top easy-access Cash ISAs pay around 4.6% AER. Both are tax-free.

- The prize fund rate is the average return across all bondholders. The median bondholder wins significantly less, because a handful of large prizes drag the mean upwards.

- Premium Bonds are uniquely backed by HM Treasury through NS&I, so there is no £85,000 FSCS cap. They are useful sovereign-backed exposure above £85k.

- A Cash ISA almost always beats Premium Bonds on expected return for balances under £20,000. Premium Bonds make sense for high earners who have already used their ISA allowance.

- The way these products are marketed pushes the lowest-income savers towards the option that pays them less. That is a design problem, not a maths problem.

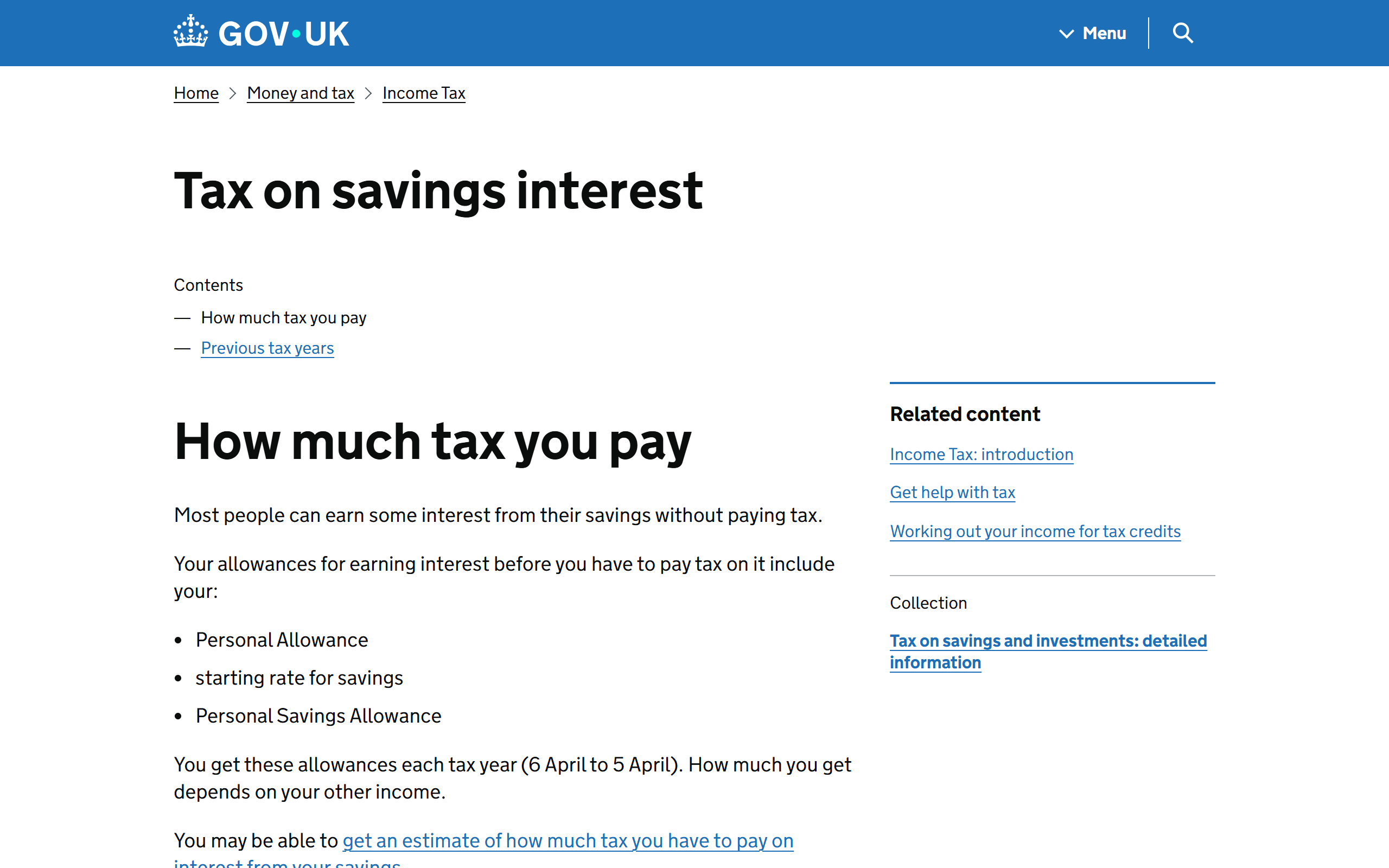

Expected annual return on £10,000

Median bondholder typically wins less than the mean. The prize fund rate is misleading at low balances.

Which product wins for you

| Your situation | Better choice |

|---|---|

| Under £20k savings, basic-rate | Cash ISA |

| Under £20k savings, higher-rate | Cash ISA |

| ISA used, £20k to £50k, higher or additional rate | Premium Bonds |

| Cash over £85k, want sovereign-backed | Premium Bonds |

| Saving for emergency fund or known goal | Cash ISA |

| Would otherwise gamble the money | Premium Bonds |

Rates as of May 2026. Top Cash ISAs around 4.6% AER, Premium Bonds prize fund 3.30% (3.80% from July 2026).

Premium Bonds vs Cash ISA: Which One Actually Pays More in 2026?

The core trade-off is simple. Premium Bonds give you a tax-free monthly prize lottery with a 3.30% average annual return. A Cash ISA gives you tax-free guaranteed interest at up to 4.62% AER on top easy-access accounts. Both are UK-only. Both are sensible options for someone. Both are routinely misunderstood, and one of them is sold harder to the people it pays least.

This guide compares the two using current 2026 figures, explains why the headline prize fund rate flatters Premium Bonds for most holders, and shows who each product actually suits.

Contents

- How Premium Bonds work

- How Cash ISAs work

- The prize fund rate is misleading

- When Premium Bonds win

- When a Cash ISA wins

- Worked examples at £10,000

- The decision matrix

- Frequently asked questions

How Premium Bonds Work

Premium Bonds are issued by National Savings and Investments (NS&I), a Treasury-owned bank. You buy bonds at £1 each, with a minimum purchase of £25 and a maximum holding of £50,000 per person.

Instead of paying interest, each £1 bond is entered into a monthly prize draw run by ERNIE (Electronic Random Number Indicator Equipment). Prizes range from £25 to £1,000,000 and are completely tax-free.

The current odds, as published on nsandi.com, are 23,000 to 1 for every £1 bond in each monthly draw (improving to 22,000 to 1 from the July 2026 draw). The annual prize fund rate sits at 3.30% until the June 2026 draw, then rises to 3.80% from July 2026.

That prize fund rate is the total prize pool divided by all eligible bonds in issue. It is the average return across every bondholder, not what any individual will win. We will come back to why that distinction matters.

Two structural points worth understanding:

- Capital is 100% secure. NS&I is backed directly by HM Treasury, so deposits sit outside the standard FSCS scheme. You do not need to worry about the £85,000 FSCS limit here, which makes Premium Bonds genuinely useful for savers with large cash piles.

- All prizes are tax-free. They do not count towards your Personal Savings Allowance or your ISA allowance, and they never appear on a tax return.

How Cash ISAs Work

A Cash ISA is a tax-free savings account. Interest is paid into the account untaxed and never enters your tax calculation, regardless of how high your income is or how much interest you earn.

The rules:

- £20,000 annual ISA allowance across all ISA types combined (Cash ISA, Stocks and Shares ISA, Lifetime ISA, Innovative Finance ISA).

- Easy-access or fixed structure available. Easy-access pays a variable rate and lets you withdraw on demand. Fixed-rate Cash ISAs lock the money up for 1-5 years in exchange for a slightly higher rate.

- Flexible ISA feature (offered by some providers, not all): money withdrawn and replaced within the same tax year does not count against your annual allowance. This is a quiet but powerful feature.

- FSCS protection up to £85,000 per banking authorisation. Several "different" brands share a single licence, so the practical cap is per licence, not per brand. See our FSCS guide for the providers that share.

Top easy-access Cash ISA rates in May 2026 sit around 4.6% AER. Trading 212 leads at 4.62% (3.60% variable plus a 12-month 1.02% bonus). Plum sits just behind at 4.60%. Moneybox pays 4.33% but limits you to three withdrawals before the rate collapses. Mainstream providers like Bank of Ireland UK pay around 4.21%. Rates change frequently; our Cash ISA comparison page tracks the current top picks.

Fixed-rate Cash ISAs typically pay 0.2-0.5% more than easy-access for a one-year lock. For most savers, easy-access is the right starting point.

The Prize Fund Rate Is Misleading

This is the bit that is rarely explained properly.

The 3.30% prize fund rate is an average. It is calculated as total annual prizes divided by total bonds in issue. It tells you what the system pays out collectively, not what you personally will earn.

The median bondholder return is materially lower than the mean, because a handful of huge prizes (two £1 million prizes per month, plus a long tail of £100,000 and £50,000 prizes) pull the mean upwards while doing nothing for typical holders. Independent simulations by MoneySavingExpert and others have repeatedly shown that someone holding £1,000 has roughly a 50% chance of winning nothing at all over a 12-month period. The same holder has a tiny chance of winning thousands.

In statistical terms, the distribution is highly right-skewed. A small number of lucky winners drag the average up. Most people, by definition, sit below the average.

The skew is worst at low holdings. Someone with £100 in Premium Bonds has roughly a 1 in 25 chance per month of winning anything at all, and the expected annual return for a £100 holding is well below 3.30% in practice. At the £50,000 maximum holding, the law of large numbers starts to help. You hold so many bonds that your monthly outcomes converge towards the prize fund rate. Even then, the median holder at £50k typically wins slightly less than the mean.

To put numbers on it:

- £1,000 holding: median return roughly 0% in any given year, with a long tail of small wins

- £10,000 holding: median return roughly 2-3%, mean closer to the prize fund rate

- £50,000 holding: median return roughly 2.5-3.2%, mean close to the prize fund rate

These are indicative figures from independent simulations of the published odds, not guaranteed outcomes. Past prize-draw results are not a reliable guide to future returns, and the prize fund rate itself can be cut by NS&I at any time.

This is the single biggest thing the NS&I marketing does not spell out, and it is the reason a Cash ISA usually pays a typical holder more than Premium Bonds at the same rate.

When Premium Bonds Win

Premium Bonds are the right answer for specific people, not the general public:

- Additional-rate taxpayers (income over £125,140) who get no Personal Savings Allowance at all. Every pound of bank interest above zero is taxed at 45%. Tax-free prizes from Premium Bonds are genuinely competitive once you factor that in.

- Higher-rate taxpayers above the £500 PSA who have already used their £20,000 ISA allowance for the year. Premium Bonds are the next tax-efficient cash home, with no annual cap up to £50k.

- Cash holders above £85,000 who want some exposure outside the FSCS limit. NS&I sits behind the Treasury balance sheet, not the FSCS, so the full £50,000 maximum holding is sovereign-backed regardless of the FSCS rule. For someone holding £200k in cash, splitting £50k into Premium Bonds removes one chunk from the bank-licence diversification problem entirely.

- People who would otherwise spend the money gambling. This is a behavioural argument rather than a maths argument, and it is real. Someone who buys £10 of National Lottery tickets a week is spending £520 a year on a product with an expected return of around minus 50%. Putting that money in Premium Bonds instead keeps the lottery dopamine and the capital. It is a harm-reduction case, not a return-maximising one.

When a Cash ISA Wins

For everyone else, the maths points to a Cash ISA:

- Basic-rate taxpayers below the £1,000 PSA. The PSA already shelters £25,000 at 4% from tax. A Cash ISA only adds value once you exceed it.

- Anyone with under £20,000 in cash savings. The full balance fits inside one year's ISA allowance. The expected return is higher than Premium Bonds, the income is guaranteed, and compounding works in your favour.

- Anyone using cash for an emergency fund or a known short-term goal. You need a predictable balance, not a lottery. A 4.5% guaranteed return on £15,000 is £675. A Premium Bonds equivalent gives you a median of roughly £300-400 with no guarantee.

- Higher-rate taxpayers who have not yet used their £20k ISA allowance. The ISA gives you both the tax shelter and the higher expected return. Premium Bonds only become interesting once the ISA is full.

Worked Examples at £10,000

Same balance, two products, current 2026 rates.

£10,000 in Premium Bonds

- Headline prize fund rate: 3.30%

- Expected (mean) annual return: £330

- Median realistic return: roughly £200-300 in a typical year

- Range: anywhere from £0 to (in theory) £1,000,000

- Tax: zero

£10,000 in a Cash ISA at 4.50% AER

- Guaranteed annual interest: £450

- Range: £450 (the rate may move during the year if variable)

- Tax: zero

£10,000 in a non-ISA easy-access account at 4.50%

- Gross interest: £450

- Basic-rate taxpayer below PSA: £450 net

- Higher-rate taxpayer above £500 PSA: £450 minus 40% on the excess, depending on other interest

- Additional-rate taxpayer (no PSA): £270 net after 45% tax

The Cash ISA's £450 guaranteed beats the Premium Bonds expected £330 in every reasonable scenario at £10,000. The gap widens once you factor in the median-vs-mean issue.

The case flips at higher balances and higher tax bands. A £50,000 Premium Bonds holding for an additional-rate taxpayer who has already used their ISA allowance generates a tax-free expected £1,650, against around £1,650 minus 45% (£907) on a comparable taxable savings account paying the same gross rate.

The Worker-Protective Angle

NS&I and Premium Bonds occupy a genuinely useful niche in the UK savings landscape. They are sovereign-backed, tax-free, and have no annual contribution cap up to £50,000. That combination is uniquely valuable for high earners who have already exhausted their ISA allowance and would otherwise pay 40% or 45% on additional savings interest.

For everyone else, the maths is brutal. A Cash ISA pays more in expected return, more in median return, and more in certainty. The Cash ISA wins.

The problem is how these products are sold. NS&I runs glossy television campaigns featuring jackpot winners. Cash ISAs have no equivalent marketing. The lottery framing is psychologically powerful, particularly for lower-income households who are most exposed to the "what if I won?" hook. Behavioural finance research consistently finds that people overweight small probabilities of large payoffs - the same cognitive bias that makes the National Lottery work.

The result is that the savers who would benefit most from a Cash ISA's predictable compounding are the most likely to be pulled towards Premium Bonds by the marketing. That is a feature of how the products are sold, not how the maths works. If you are choosing between the two, ignore the adverts and look at your tax band, your ISA allowance, and your balance. The right answer falls out of those three numbers.

Premium Bonds vs Cash ISA: The Decision Matrix

| Your situation | Better choice |

|---|---|

| Under £20k in savings, basic-rate taxpayer | Cash ISA |

| Under £20k in savings, higher-rate taxpayer | Cash ISA |

| ISA allowance used, balance £20k-£50k, higher or additional rate | Premium Bonds |

| ISA allowance used, balance £20k-£50k, basic rate | Premium Bonds if tax matters, taxable savings if rate matters |

| Over £85k in cash, want sovereign-backed exposure | Premium Bonds (up to £50k) |

| Saving for emergency fund or known goal | Cash ISA |

| Would otherwise gamble the money | Premium Bonds |

| Additional-rate taxpayer, any balance | Premium Bonds likely beats taxable savings |

You can hold both. Many people sensibly do: ISA allowance used in full, then Premium Bonds for the next £50k of cash, with the rest split across top easy-access savings accounts or short-dated gilts depending on tax band.

If you have not used your full ISA allowance yet, the Cash ISA comparison tool will show you the current top rates. Your marginal tax position changes the maths, and our take-home pay calculator can tell you which band you sit in.

For a broader view of NS&I products beyond Premium Bonds, see our overview of what NS&I is and how it fits the UK savings landscape.

Frequently Asked Questions

Are Premium Bonds better than a Cash ISA?

For most savers, no. A Cash ISA at 4.6% AER beats the 3.30% Premium Bonds prize fund rate on expected return, and the median bondholder typically wins less than the headline rate suggests. Premium Bonds become more attractive for higher-rate or additional-rate taxpayers who have already used their £20,000 ISA allowance, and for anyone holding more than £85,000 in cash who wants sovereign-backed exposure.

Can I have both Premium Bonds and a Cash ISA?

Yes. The two are completely separate. Premium Bonds do not count towards your £20,000 annual ISA allowance, and Cash ISAs do not affect your £50,000 Premium Bonds maximum. Many people sensibly hold both.

Are Premium Bonds protected by FSCS?

No, and they do not need to be. NS&I is owned directly by HM Treasury, so deposits and prizes are backed by the UK government rather than the FSCS scheme. This is why Premium Bonds are useful for savers who hold more than the £85,000 FSCS limit at any single bank. See our FSCS protection guide for how the standard rules work.

Do I need to declare Premium Bond winnings on a tax return?

No. All Premium Bond prizes are entirely free of income tax and capital gains tax. You do not declare them on a Self Assessment return, and they do not count towards your Personal Savings Allowance.

What is the average return on Premium Bonds?

The current prize fund rate is 3.30%, rising to 3.80% from the July 2026 draw. This is the mean return across all bondholders, not what any individual will earn. The median holder, particularly at lower balances, typically wins less than this. At the £50,000 maximum holding, your outcomes converge closer to the prize fund rate over time.

How quickly can I withdraw from Premium Bonds?

NS&I generally pays out cash withdrawals within 3 working days. This is slower than a typical easy-access Cash ISA, which usually pays out same-day or next-day, so Premium Bonds are not ideal for an emergency fund that you might need to access urgently.

Are Premium Bonds worth it in 2026?

For a basic-rate or higher-rate taxpayer with under £20,000 in savings, no - a top Cash ISA at around 4.6% AER pays more on expected return and gives you certainty. Premium Bonds are worth holding in 2026 mainly for additional-rate taxpayers, anyone who has already used their £20,000 ISA allowance, and savers with more than £85,000 in cash who want exposure outside the FSCS scheme.

What is the best Cash ISA in the UK right now?

In May 2026 the top easy-access Cash ISA rates sit around 4.6% AER, with Trading 212 at 4.62% (including a 12-month bonus) and Plum at 4.60%. "Best" depends on whether you value the highest headline rate, withdrawal flexibility, or brand familiarity. Rates change often, so always check our live Cash ISA comparison before opening one.

Can I lose money on Premium Bonds?

You cannot lose capital. NS&I guarantees to return your full investment on demand. You can lose purchasing power: if inflation runs above the prize fund rate, your money loses real value. With CPI around 2.5% and the prize fund rate at 3.30%, the real return is currently positive, but it is much thinner than the headline number suggests.

Read Next

- Best savings account UK 2026 - the full guide to easy-access, fixed bonds, and where the top rates actually sit

- UK Bonds Explained: Gilts, Premium Bonds and Tax - how Premium Bonds fit alongside gilts and the broader UK bond market

- FSCS Protection UK Guide - the £85,000 rule, the per-banking-licence catch, and why NS&I sits outside it

- What is NS&I? - the full picture of the Treasury-owned bank behind Premium Bonds, Income Bonds, and Direct Saver

Further Reading:

The Money Diet - Martin Lewis - The classic UK personal finance guide that lays out the case for tax-efficient saving in plain English. (Affiliate link - we may earn a small commission at no extra cost to you.)

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all