Geopolitical Risk: The One Threat to Your Portfolio You Can't Hedge

In 1979 the Warsaw Pact planned to nuke West Germany, Belgium and Denmark, but not Britain or France. The lesson for your portfolio: the risk you can't hedge is the one that should never make you sell.

Cite this article

Freedom Isn't Free (2026) Geopolitical Risk: The One Threat to Your Portfolio You Can't Hedge. Available at: https://freedomisntfree.co.uk/articles/geopolitical-risk-investing (Accessed: 15 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Geopolitical risk is the one portfolio risk you cannot diversify away, because the worst case (nuclear war) makes every hedge worthless at once.

- Cold War nuclear plans on both sides deliberately targeted non-nuclear countries and spared the ones that could hit back. Deterrence decided who was on the list.

- Because the tail risk is unhedgeable, geopolitical fear should almost never move your portfolio. Every survivable crisis has been a hold-or-buy, not a sell.

- The defence and nuclear-energy spending boom is real, but a global index fund already owns it. You do not need to punt on war stocks.

Who the 1979 Warsaw Pact plan marked for nuclear strikes

| NATO member | Own nuclear weapons | On the nuclear target list |

|---|---|---|

| West Germany | No | Yes |

| Belgium | No | Yes |

| Netherlands | No | Yes |

| Denmark | No | Yes |

| United Kingdom | Yes | No |

| France | Yes | No |

Seven Days to the River Rhine, declassified in 2005. The deterrent decided who was on the list.

Geopolitical Risk: The One Threat to Your Portfolio You Can't Hedge

Geopolitical risk is the phrase every fund manager reaches for when they want to sound serious about the world and stay vague about your money. It lives in the risks section of every prospectus, earns a grave nod in every market outlook, and almost never arrives with anything useful attached.

So here is the useful part, and it is not the part you will expect. The one geopolitical event big enough to permanently destroy a globally diversified portfolio is also the event where your portfolio, your gold, your bunker and your tinned food are all worth exactly the same amount: nothing. Which makes geopolitical risk the one risk you genuinely cannot hedge. And that fact, once you sit with it, should make you calmer, not more anxious.

I studied International Relations at university, and a good chunk of the reading was about how the Cold War planned to end. It turns out to be oddly useful training for an investor, because it explains why the scariest risk on the board is the one you should waste the least energy trying to dodge.

Contents

- What geopolitical risk actually is

- The escalation ladder nobody wants to climb

- The detail that should change how you think

- De Gaulle and the bomb that kept France off the list

- Why this is the one risk you cannot hedge

- The risks that actually move markets

- The money that actually gets spent

- Frequently asked questions

What Geopolitical Risk Actually Is

Strip away the jargon and geopolitical risk is the chance that states, rather than markets, do something that costs you money. Wars, coups, sanctions, blockades, a strait closed to oil tankers, a border redrawn by force. It is risk that comes from the behaviour of governments and armies, not from interest rates or earnings.

Economists have even tried to measure it. Two Federal Reserve economists, Dario Caldara and Matteo Iacoviello, built a Geopolitical Risk Index that counts how often the world's big newspapers use words tied to war threats, military buildups, nuclear threats and terror. Their index spikes around the two world wars, the Korean War, the Cuban Missile Crisis and 9/11. Higher readings, they found, tend to come before lower investment and employment. So the risk is real, and it does leave a mark on the economy.

Here is the reframe, though. Most of the risks in your portfolio are things you can spread. Company risk, you diversify across thousands of firms. Sector risk, you hold every sector. Country risk, you own the whole world. Geopolitical risk is the one that laughs at all of that, because the version of it that would actually wipe you out does not hit one company or one sector or one country. It hits everything, everywhere, in the same afternoon. Geopolitical risk is really the risk you cannot diversify away. Hold that thought, because it is the whole article.

The Escalation Ladder Nobody Wants to Climb

We tend to imagine nuclear war as a single red button. One bad morning, someone presses it, and that is that. The people whose actual job was to plan these wars did not think like that at all. They thought in steps.

In 1965 the strategist Herman Kahn published a book called On Escalation that laid out a 44-rung "escalation ladder", running from a diplomatic crisis at the bottom all the way up to all-out "spasm" war at the top. The point of the ladder was that conflict climbs one rung at a time, and that each side is constantly reading the other to decide whether to step up or step off. Real war plans worked the same way. The American plan, the Single Integrated Operational Plan or SIOP, started in the early 1960s as one enormous all-or-nothing strike and was later broken into graduated options, so a president had choices short of ending the world.

That word "graduated" matters, because it means somebody, somewhere, wrote down the order in which countries would be hit. And when those documents were finally declassified, the order tells you something no market-outlook footnote ever will.

The Detail That Should Change How You Think

Start with the American plan. The first integrated war plan, SIOP-62, was built to strike the entire Communist bloc at once: the Soviet Union, China, and their allies, whether or not those allies had done anything. When the plan was analysed, one detail stood out. The estimated dead were counted not just in the Soviet Union and China but across Eastern Europe, including roughly 2.6 million in Poland. Poland had no nuclear weapons of its own. It was on the list anyway, purely for the sin of being on the wrong side of the map.

Now the Soviet plan. In 2005, after a change of government, Poland declassified a 1979 Warsaw Pact exercise with the cinematic name "Seven Days to the River Rhine". It modelled a European war, and it named the targets. Soviet nuclear strikes would fall on West Germany, Belgium, the Netherlands, Denmark and northeast Italy. Hamburg, Cologne, Frankfurt, Munich and Bonn destroyed. NATO's headquarters in Brussels and the port of Antwerp gone. Amsterdam gone.

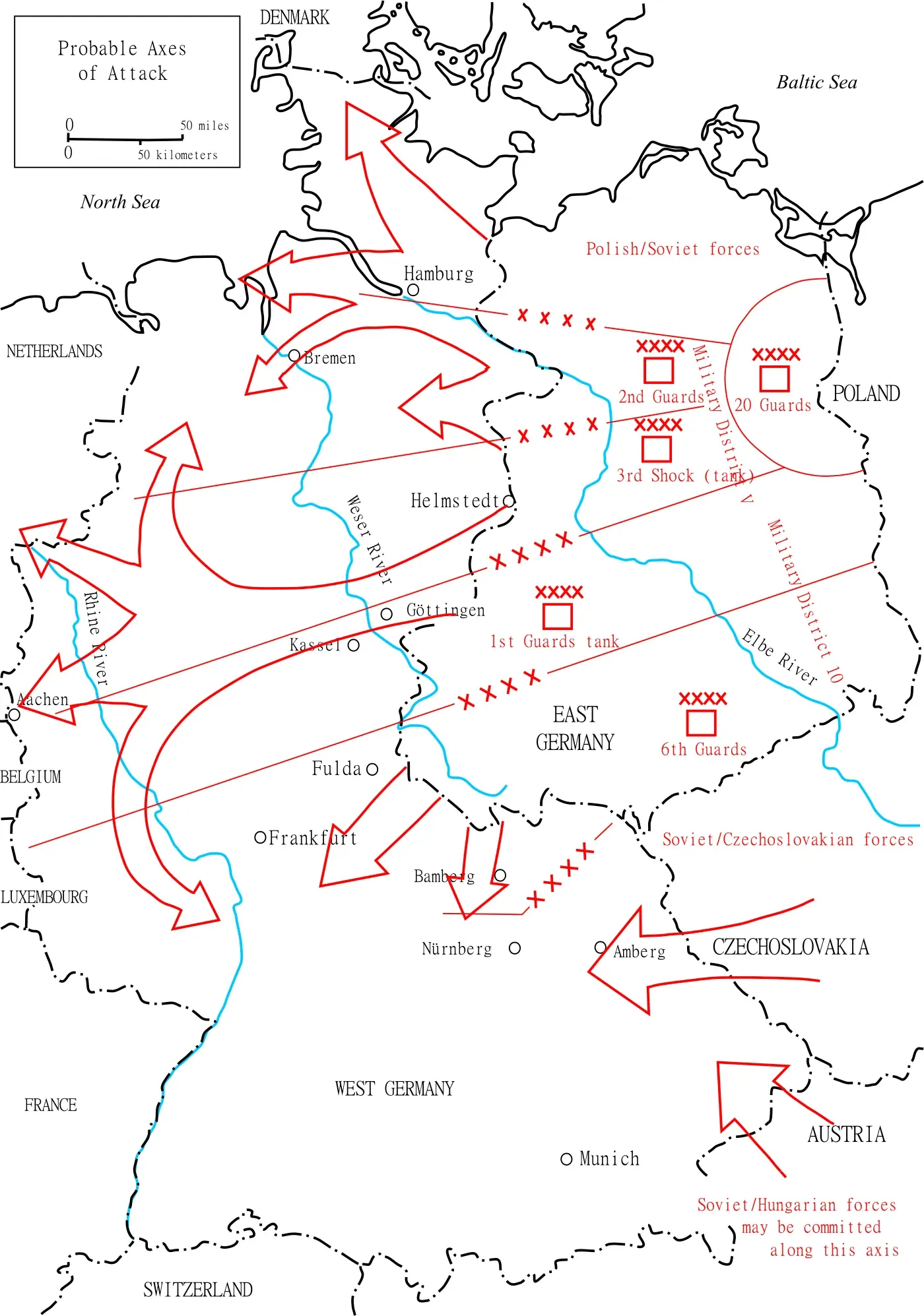

How the ground war was expected to open: a US assessment of the Warsaw Pact's likely invasion routes into West Germany and the Low Countries, the same non-nuclear countries the Soviet nuclear plan had marked for destruction. Source: US Army (Graham H. Turbiville, 1976), public domain.

Look at that target list and then look at who is missing from it. Britain and France, both NATO members, both sitting right in the theatre of war, are not marked for nuclear strikes. The difference between them and the countries that were marked is a single fact: Britain and France had their own nuclear weapons and could hit back. West Germany, Belgium, the Netherlands and Denmark could not.

That is the crux, and it is the crux of the entire deterrence argument. A deterrent does not make you safe because you plan to use it. It makes you safe because being able to retaliate quietly moves you off somebody else's target list. Both superpowers built plans that hit the enemy's non-nuclear associates and stepped carefully around anyone who could answer back. Non-nuclear countries get hit first. That is not a slogan. It is what the declassified paperwork says.

De Gaulle and the Bomb That Kept France off the List

The clearest proof that this logic is real, rather than a tidy pattern spotted after the fact, is that one man bet his country on it decades before any target list was declassified. Charles de Gaulle looked at the American nuclear guarantee, the promise that the United States would defend Western Europe with its own arsenal, and decided he did not believe a word of it.

His reasoning was brutally simple and has never really been improved on. Once the Soviet Union could destroy American cities in return, would a US president actually trade New York for Paris? Would any American leader invite the incineration of an American city to avenge a European one that had already fallen? De Gaulle concluded, reasonably, that he would not, and that a guarantee nobody will honour once the missiles are flying is not a guarantee at all. So France built its own. The force de frappe, tested for the first time in the Algerian desert in 1960, made France the world's fourth nuclear power, and in 1966 de Gaulle pulled France out of NATO's integrated military command rather than let its deterrent take orders from Washington.

At the time this was written off as vanity, expensive Gallic pride, a distraction from the real Atlantic alliance. Then the Warsaw Pact's own war plan surfaced, and there was France, sitting squarely in the theatre of war, not marked for a single nuclear strike. De Gaulle had not been proud. He had been correct. The independent bomb he was mocked for building is the exact reason Soviet planners drew their arrows around France and onto West Germany instead. He understood the target-list logic in 1960, and the declassified paperwork proved him right in 2005.

There is a colder lesson buried in that, and it is not really about weapons. De Gaulle refused to outsource his country's survival to an ally whose interests only mostly overlapped with his own, on the correct assumption that when the moment came, that ally would be perfectly rational about protecting itself first. The equivalent in your own life is refusing to let your security rest entirely on a single employer, a single pension promise, or a single counterparty who will look after their own interests before yours when it counts. Own the thing that protects you. That is the whole of it.

Why This Is the One Risk You Cannot Hedge

Bring it back to your money, because this is a personal finance site and there is a genuinely useful investing lesson buried in all this Cold War paperwork.

Every hedge you can buy is a bet that the world keeps functioning enough for the hedge to pay out. Gold works because someone on the other side still wants gold and can trade you food for it. Government bonds work because the government is still there to pay the coupon. Cash works because the currency still means something. A full nuclear exchange erases all of those conditions in the same moment. There is no counterparty, no exchange, no settlement, no tomorrow morning where you calmly sell your bullion. The ultimate geopolitical risk is uninsurable by definition, because it destroys the thing that makes insurance pay.

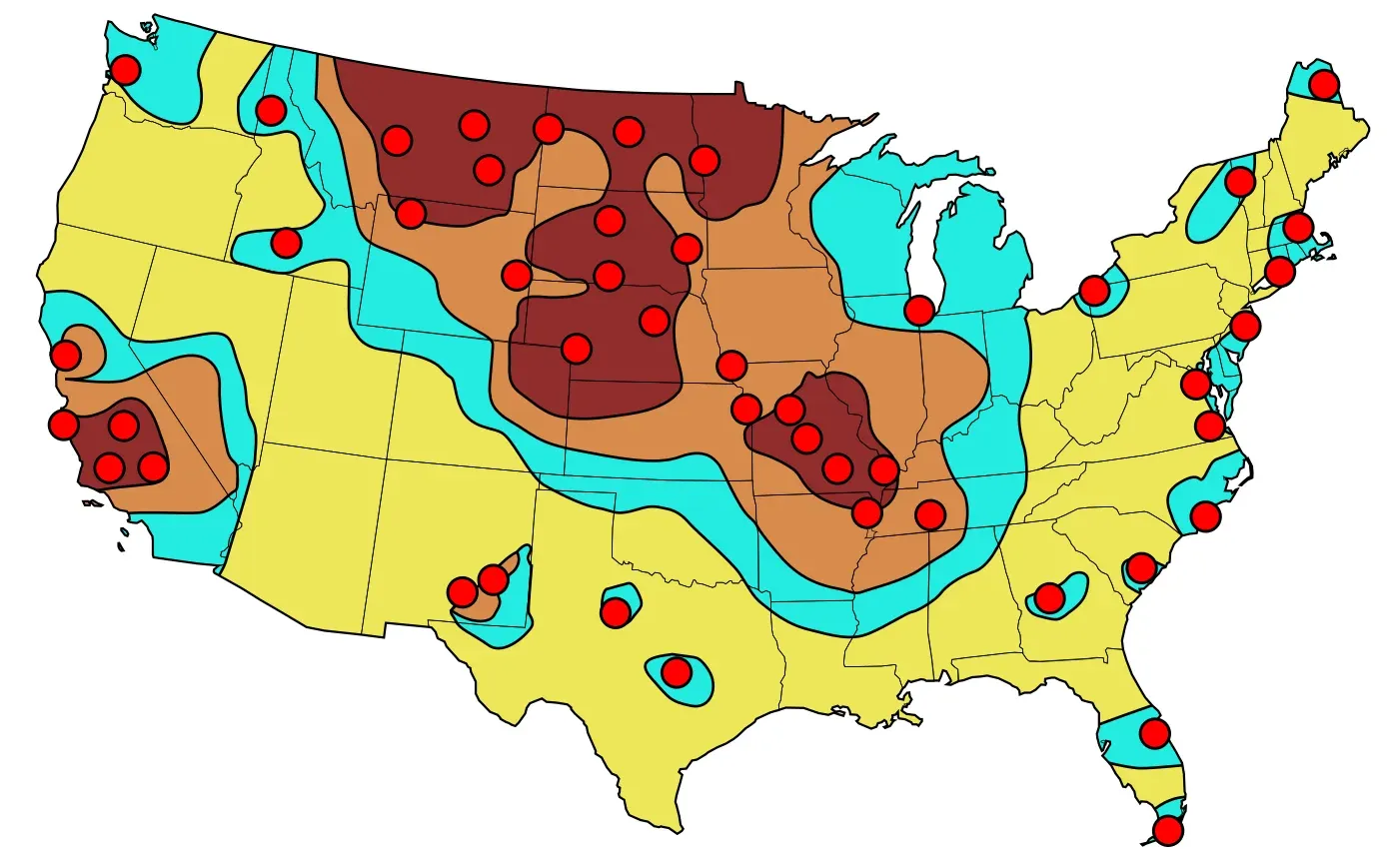

The other side of the same coin: a US civil-defence map of primary Soviet nuclear targets (red) and the resulting fallout, from lethal dark red to safer yellow. This is the risk no portfolio survives, which is exactly why no portfolio should be built around it. Source: US Federal Emergency Management Agency, public domain.

So you are left with a strange but freeing conclusion. The geopolitical scenario bad enough to justify torching your investment plan is precisely the one where torching your investment plan changes nothing, because nobody survives it richer for having sold in time. And every geopolitical scenario short of that, every single one, has been survivable for a diversified investor. The Cuban Missile Crisis, the closest the world has come, was followed by one of the great bull runs in history. The Iran crisis, the Gulf War, 9/11 and the invasion of Ukraine all felt like the end at the time. Markets fell, then markets recovered, and the investors who did nothing came out ahead of the ones who got clever. This is just the psychology of a market crash playing out on a geopolitical stage, and the evidence on time in the market is not subtle.

This is where I get properly opinionated, because there is an industry that exists to profit from getting this exactly wrong. The doom merchants who tell you to sell everything, buy gold, stockpile freeze-dried stew and pay for a bunker slot are selling you a hedge against the one outcome no hedge survives. It is the same logic I distrust in most insurance: a bet, priced by the seller, that pays you badly on average and best of all in a world where nobody is around to collect. The honest version of geopolitical caution is dull. Own the whole world through a low-cost global index fund. Keep an emergency fund in cash so a real-life shock in your own life never forces you to sell at the bottom. That cash buffer and a steady income are the only geopolitical hedges that reliably work, because they protect you from the crises that actually happen to ordinary people, not the one that ends everything.

And notice the quiet irony in the usual "flight to safety". Piling into your home country's assets because the world feels dangerous only swaps a spread-out risk for a concentrated one. Home bias is a bet that your one country stays lucky. A global fund already spreads you across every nuclear power, every safe harbour and every economy likely to still be standing on the other side of a crisis. Far from the timid option it feels like, diversification is the actual answer to the question fear is asking.

The Risks That Actually Move Markets

Dwelling on the apocalypse can leave you with a lopsided picture, as though geopolitical risk were only ever the mushroom cloud. It almost never is. The geopolitics that genuinely reaches your portfolio lives in the wide band below the nuclear threshold: the chokepoints, regional wars and blockades that snarl trade, spike a commodity and rattle markets for a quarter or two before the world adjusts. These are the ones worth understanding, precisely because they are survivable, which is exactly what makes them tempting to trade on. Four are worth knowing by name.

The Strait of Hormuz. A sea lane between Iran and Oman, barely 21 miles wide at its narrowest, carries roughly a fifth of the world's oil, about 20 million barrels a day. Iran periodically threatens to close it. It never quite has, because doing so would throttle its own customers and invite a response it cannot survive, but every flare-up in the Gulf lifts the oil price and, with it, the cost of running every airline, haulier and factory on earth. This is the Iran crisis that keeps returning, and the market keeps recovering from it.

Taiwan. The island makes more than 90% of the world's most advanced computer chips, the overwhelming majority at a single company, TSMC. Almost nothing modern ships without them: not a phone, a car, a fighter jet or a data centre. China regards Taiwan as its own territory and has never renounced taking it by force. A blockade, let alone an invasion, would do to the chip supply what an oil embargo does to petrol, except there is no Saudi Arabia standing by to open the taps instead. It is the most concentrated economic chokepoint on the planet, which is precisely why the deterrence around it is so heavily armed.

Suez and the Red Sea. Somewhere between 12 and 15% of world trade, and about a third of all container traffic, passes through the Suez Canal. In 2021 a single grounded ship, the Ever Given, wedged across it for six days and jammed supply chains worldwide. Since 2023, Houthi missiles fired from Yemen have done the same thing on purpose, forcing much of the world's shipping onto the long route around the Cape of Good Hope, adding roughly ten days and a heap of cost to every diverted voyage. Nobody has to fire a shot at you for a distant war to turn up in your shopping.

Eastern Europe. Russia's invasion of Ukraine in 2022 was the largest land war in Europe since 1945, and it set off exactly the risks this article is about: an energy shock, a food-price shock (Ukraine and Russia are among the world's biggest grain exporters), and a continent-wide scramble to rearm. It also runs right up to NATO's red line. The Baltic states and Poland are treaty members, so an attack on them is, on paper, an attack on every NATO nuclear power at once. That is the deterrent logic from the last section again, only this time drawn as a border.

Notice what the four have in common. Each is frightening, each moves markets, and each has so far been survived by an investor who simply did nothing. The oil spike fades, the ships reroute, the chips keep coming, the front line holds. A globally diversified fund already owns companies on every side of these lines, priced for the risk, so you are paid to carry it whether or not you ever think about it. The mistake is not failing to guess which chokepoint flares up next. The mistake is selling the entire world because one of them made the news.

The Money That Actually Gets Spent

There is a second, more concrete investing angle, and it is the one your friend who "got into defence stocks" wants to talk about. Rising geopolitical risk does one very predictable thing: it makes governments spend. At the 2025 Hague summit, NATO members committed to lifting spending to 5% of GDP a year by 2035, split into 3.5% on core defence and 1.5% on wider security and resilience. That is a huge, multi-decade wall of money aimed at weapons, shipyards, networks and, yes, power stations. Whether that spending strengthens a country or slowly hollows it out depends entirely on how it is paid for: war debt has felled great powers before, Britain's own empire among them.

Two temptations follow, and both are traps for a normal investor. The first is to go stock-picking for "war winners", loading up on the defence primes after the headline has already sent them up. The problem is that you are usually buying the spike. By the time a conflict is on the front page, the market has repriced BAE Systems, Rolls-Royce, Lockheed Martin and the rest. The second temptation is subtler: to feel you are missing out. You are not. If you own a global index fund, you already own every one of those companies at their proper weight, bought at the average price rather than the panic price. You do not need a clever trade to participate in the rearmament of the West. You need to have already done the boring thing.

This is where the nuclear thread ties back together, because it is the part most people miss. A country's civilian nuclear industry and its military one are the same body of knowledge wearing different coats. The engineers, the fuel cycle, the reactors that drive submarines, the skills base that keeps a deterrent credible, all of it grows from the same root. Britain's bomb came out of its post-war civil nuclear programme, not the other way round. Which means "we need nuclear power plants" is not only an energy-policy sentence, it is a national-security one. Sizewell C and Hinkley Point C, the American push for small modular reactors, the revival of uranium supply chains: these are the industrial base of sovereignty as much as they are a way to keep the lights on.

And this is the pro-worker heart of it. Energy independence protects ordinary households from being squeezed the moment a dictator turns off a pipeline, exactly as a deterrent protects a country from being pushed around by one that can. Both are shields for the many, not the few. They come with skilled, unglamorous, well-paid jobs in places that badly need them. You can believe all of that, and invest in all of that, without taking a single flutter on an individual stock. The global fund holds the reactor builders and the defence firms already. Sovereignty, it turns out, is something you can own passively.

Frequently Asked Questions

What is geopolitical risk?

Geopolitical risk is the risk that the actions of states, rather than markets, will hurt the economy and your investments. It covers wars, sanctions, coups, trade blockades and diplomatic crises. Federal Reserve economists even publish a Geopolitical Risk Index that tracks how often the world's newspapers mention war threats, military buildups and nuclear threats, and it reliably spikes around events like the Cuban Missile Crisis and 9/11. The key feature for an investor is that the worst version of it, a global war, cannot be diversified away, because it damages every asset at once.

What is an example of geopolitical risk?

Recent examples include Russia's invasion of Ukraine in 2022, the tensions around Iran and the Strait of Hormuz, and the trade and technology stand-off between the United States and China. Each pushed up energy prices or rattled markets. Historically, the sharpest example was the Cuban Missile Crisis of 1962, when the United States and Soviet Union came close to nuclear war. In every one of these cases short of actual world war, a globally diversified investor who held their nerve recovered.

What does geopolitical mean in simple terms?

Geopolitical means "to do with power and geography between countries", the way nations compete over territory, resources, trade routes and influence. When something is described as a geopolitical event, it is being driven by governments and their rivalries rather than by business or the economy on its own. For your money, the practical translation is: this is a risk set by politicians and armies, not by companies.

Should I sell my investments because of a war or crisis?

Almost never. Markets have recovered from every geopolitical shock in modern history, from the Gulf War to 9/11 to the invasion of Ukraine, and the investors who sold in panic usually missed the rebound that followed. Selling forces you to be right twice, on when to get out and when to get back in, and most people get both wrong. Unless your own personal circumstances have changed, the evidence points overwhelmingly to holding your position and keeping your contributions running.

How does war affect the stock market?

In the short term, war and the threat of it usually cause a sell-off, higher oil and energy prices, and a rush into perceived safe havens like gold and government bonds. In the medium term, markets tend to recover as the uncertainty resolves, and defence and energy companies often see sustained investment as governments raise military spending. The long-run pattern is that diversified equity markets have absorbed even major wars and kept compounding, which is why reacting to the headline usually costs more than the war itself does.

Further Reading:

The Psychology of Money - Morgan Housel - Why smart people make terrible decisions under stress, and how to keep your nerve when the headlines are screaming at you to do something. (Affiliate link - we may earn a small commission at no extra cost to you.)

A Wealth of Common Sense - Ben Carlson - A whole book on staying calm through market noise, and why simple long-term strategies beat clever ones during exactly the kind of crisis this article describes. (Affiliate link - we may earn a small commission at no extra cost to you.)

Thinking, Fast and Slow - Daniel Kahneman - The foundational text on why our instinctive reactions to fear and loss are systematically wrong, which is the psychology underneath everything here. (Affiliate link - we may earn a small commission at no extra cost to you.)

This article is for general information and education only. It is not financial advice and does not account for your personal circumstances. Capital is at risk: the value of investments can fall as well as rise and you may get back less than you put in. Past performance is not a guarantee of future results. Consider taking regulated financial advice before making investment decisions.

Sources

- Federal Reserve - Measuring Geopolitical Risk (Caldara & Iacoviello, GPR Index)

- National Security Archive - U.S. Cold War Nuclear Target Lists Declassified

- The National Interest - How the Warsaw Pact Planned to Win World War Three in Europe

- NATO - The Hague Summit Declaration 2025 (5% spending commitment)

- NATO - 1966: De Gaulle pulls France out of NATO's integrated military structure

- U.S. Energy Information Administration - The Strait of Hormuz oil chokepoint

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all