Hargreaves Lansdown Active Savings Review: Any Good?

I put £100 through Hargreaves Lansdown Active Savings to test it. No fees, exactly £100 landed, and the top easy-access rate beat my Trading 212 ISA. Here is the honest verdict.

Cite this article

Freedom Isn't Free (2026) Hargreaves Lansdown Active Savings Review: Any Good?. Available at: https://freedomisntfree.co.uk/articles/hargreaves-lansdown-active-savings-review (Accessed: 2 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Active Savings is a deposit marketplace: one login gives you easy-access and fixed-term products from around 20 banks and building societies.

- It is free to use, the rates are genuinely competitive (3.95% easy access when we tested it in July 2026), and you can spread cash across banks for FSCS cover.

- Interest is taxable and counts against your Personal Savings Allowance, unlike cash held inside an ISA.

- It is worth it for large cash piles, FSCS spreading and fixed-rate laddering, less so if your cash fits in an ISA.

Hargreaves Lansdown Active Savings at a glance

| Feature | Detail |

|---|---|

| What it is | A cash savings marketplace: one account, around 20 partner banks |

| Cost to you | Free (HL is paid a margin by the partner banks) |

| Minimum deposit | £1 |

| Products | Easy access (variable) and fixed term (1 month to 5 years) |

| FSCS protection | £120,000 per person per bank or building society |

| The catch | Interest is taxable (an ISA shelters it); the headline cashback is trivial below £250k |

Hargreaves Lansdown Active Savings Review: Any Good?

Yes, it is good. That is the honest verdict up front, and it surprised me, because Hargreaves Lansdown is not a name I usually reach for.

Active Savings solves a real and boring problem: the faff of opening a new savings account every time a rate drops. Instead of a drawer full of logins, you get one account that works as a marketplace, with easy-access and fixed-term products from around 20 banks and building societies you can move between in a few taps. It is free to use.

I went in expecting the catch to be a mediocre rate dressed up as convenience. Then I opened an account, put £100 through it, and came away impressed. This review covers what Active Savings is, what actually happened when I tested it, the rates I saw, the one real catch, and the things I am still checking before giving it a clean bill of health.

What Active Savings actually is

Active Savings is a deposit marketplace, not a bank. You pay money into a hub account (held at Barclays), then choose which partner product to move it into. When a fixed term ends or you fancy a better rate, you switch to another partner without filling in a single new application. The minimum to get started is £1.

The products come in two flavours. Easy-access accounts pay a variable rate and let you withdraw, usually within a working day. Fixed-term products lock your money away for anything from a month to five years in return for a higher, guaranteed rate. It is the same menu you would find across the wider savings market, gathered behind one login.

The convenience it genuinely buys

Three things make it worth a look: quick switching, FSCS spreading, and fixed-rate laddering.

The first is switching. Chasing the best savings rate normally means opening account after account, each with its own ID checks and passwords. Active Savings turns that into a few taps, so the discipline of moving your money when a rate slips actually happens instead of sitting on your good-intentions list.

The second is FSCS spreading. The Financial Services Compensation Scheme protects £120,000 per person per banking licence. If you hold more cash than that, you are meant to split it across separate banks to stay fully covered, which is a hassle done manually. Through Active Savings you can park money with several different partner banks from one place, each covered up to £120,000 in its own right.

The third is fixed-rate laddering. Because opening a new fix is frictionless, building a ladder of one, two and three-year bonds so some money matures each year is easy to run rather than a spreadsheet chore.

The rates are better than HL's reputation suggests

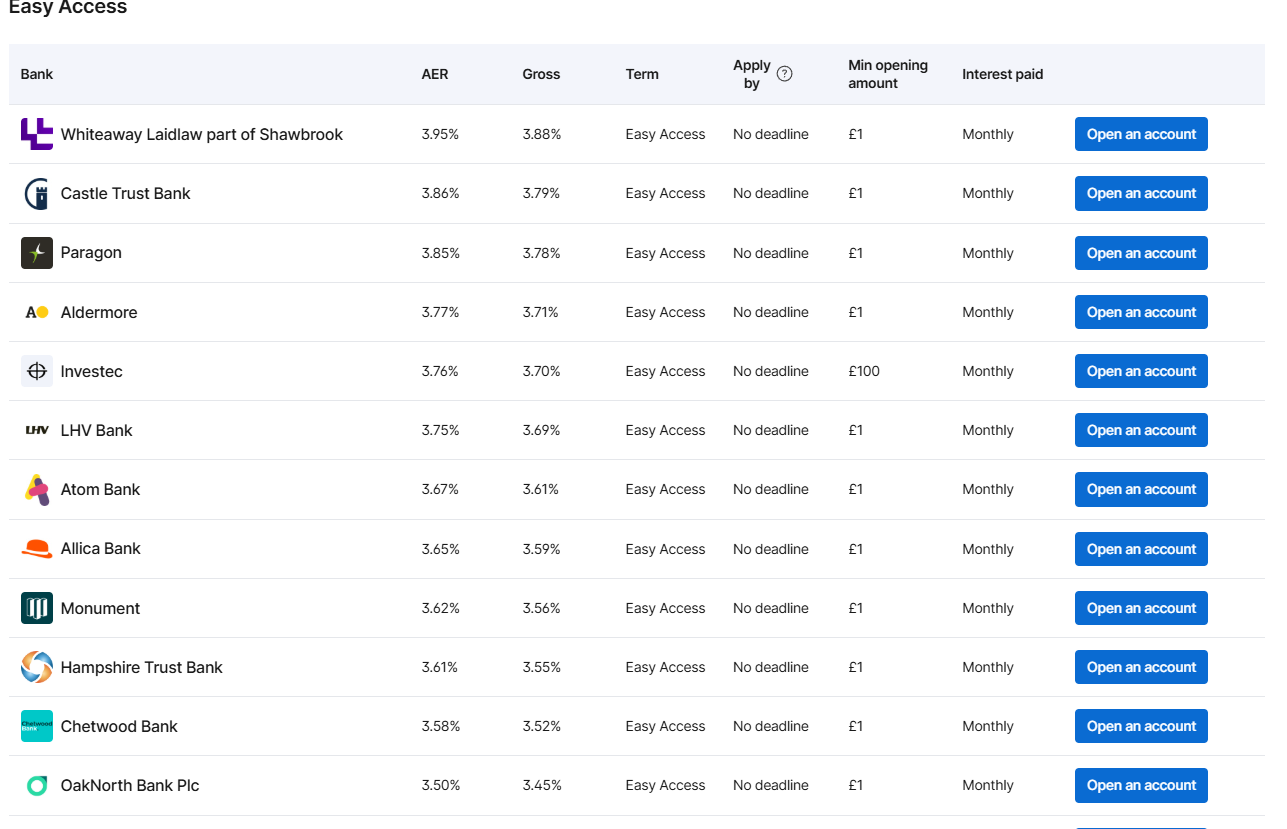

The thing that surprised me most was the rates. On 2 July 2026 the top easy-access rate on the platform was 3.95% AER, from Whiteaway Laidlaw (part of Shawbrook), with a full ladder of challenger banks just behind it and fixed terms running up to 4.6% for three years.

That 3.95% easy-access rate beat the 3.8% my own Trading 212 ISA was paying on cash at the same moment, so the fear that you sacrifice rate for the convenience did not hold up. Active Savings is free because the partner banks pay HL a margin for the deposits it sends them, so in theory a single bank could pay a touch more if you went to it directly. In practice the marketplace gathers enough competing challenger banks that the top rate on it sits right at the top of the market. One small point to note: interest is paid monthly here, where a platform like Trading 212 pays daily. Nice to have, but not the kind of thing that should sway the decision.

What happened when I put money in

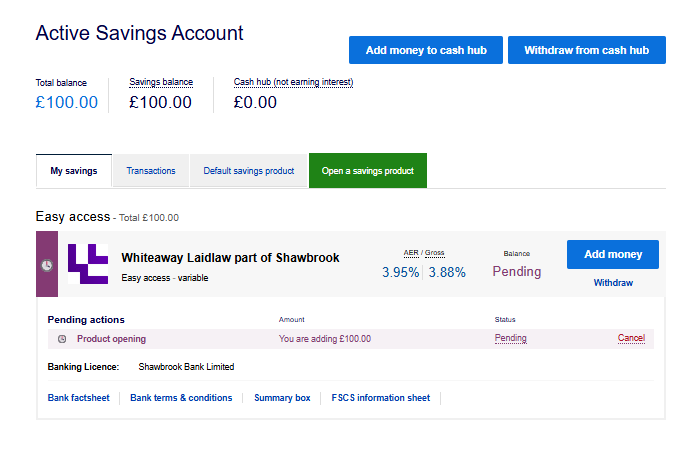

Talk is cheap, so I put £100 through it. The money went into the cash hub with no fee, and exactly £100 arrived, not £99-something after a mystery charge. I then moved it into the Whiteaway Laidlaw easy-access account at 3.95%, and again the full £100 went across, showing as pending while the account opened.

Two details on that screen matter. It names the banking licence behind the product, Shawbrook Bank Limited, and links the FSCS information sheet, so you can see exactly which bank holds your money and which FSCS bucket it sits in. That is the whole point of the FSCS-spreading benefit made concrete: you always know whose licence your cash is under, which matters when the partner banks are challenger names like Whiteaway Laidlaw or Castle Trust rather than the high-street brands you already recognise.

Ignore the cashback offer

Do not be swayed by the cashback. HL runs one for new Active Savings money, and the headline, "up to £750", is built to make you move fast. Read the terms and it deflates: the £750 only lands if you deposit £250,000 or more. Put in £10,000 and you get £20. Here were the tiers in mid-2026:

| You deposit | Cashback you get |

|---|---|

| £10,000 to £19,999 | £20 |

| £20,000 to £49,999 | £40 |

| £50,000 to £74,999 | £100 |

| £75,000 to £149,999 | £150 |

| £150,000 to £249,999 | £300 |

| £250,000 or more | £750 |

Unless you are moving a serious six-figure sum, the cashback is not a reason to do anything. It is the oldest trick in the promotions book: the big number on the poster, the real number in the PDF. Judge the account on the rate and the convenience, which stand up on their own, and treat any cashback as a rounding error.

The one real catch: the interest is taxable

The catch that costs most people something has nothing to do with Hargreaves Lansdown at all. Money in Active Savings sits in ordinary, taxable savings accounts. The interest counts against your Personal Savings Allowance, which shelters £1,000 of savings interest a year for a basic-rate taxpayer, £500 for a higher-rate taxpayer and nothing at all for an additional-rate taxpayer. Above that, you pay income tax on it.

Before you panic about that, remember the allowance is real money you can use. A basic-rate taxpayer can earn £1,000 of savings interest a year with no tax to pay, even outside an ISA, and a higher-rate taxpayer £500. At around 3.95% you would need roughly £25,000 of savings before a basic-rate taxpayer owes a penny. So for a modest pot the taxable point is academic: you pay nothing anyway. It only starts to bite once your interest climbs past the allowance.

Cash held inside an ISA does not touch that allowance at all, because ISA interest is tax-free full stop, no matter how much. So the tax question really only matters once you are past your Personal Savings Allowance. Our guide to the best ISA rates is the place to start that comparison.

So the tax point is the one real caveat, not a reason to stay away. For cash that fits inside your ISA allowance, an ISA still wins, because the interest is tax-free. For everything above that, Active Savings is genuinely hard to fault.

The tax-free version: the Active Savings Cash ISA

Here is the part that answers the tax catch, and that the headline marketing skips over. Hargreaves Lansdown runs the exact same marketplace idea as a Cash ISA. You get the same pick, mix and switch model across 10-plus banks, the same lack of an HL fee, and the same easy-access and fixed products, but the interest is tax-free and it uses your £20,000 ISA allowance instead of your Personal Savings Allowance. The best easy-access rates on the ISA version were around 4.4% at the time of writing.

That reshapes the decision, and the deciding question is your Personal Savings Allowance, not your ISA allowance. If your savings interest stays under the allowance (£1,000 for a basic-rate taxpayer, £500 for a higher-rate one), you owe no tax anyway, so the ordinary taxable Active Savings is completely fine and an ISA adds nothing. The Cash ISA only earns its keep once your interest is heading past that line. So the rule of thumb is simple. For a modest pot, do not bother with the ISA. But if you are deliberately building a large cash position, one big enough to throw off more than your allowance in interest, start it in the Cash ISA version from day one, so the interest stays sheltered as the pot grows rather than becoming a tax problem later. HL also lets you move cash between its Stocks and Shares ISA and the Cash ISA without losing the tax-free status, which helps if you want to hold investment money in cash for a while.

Who it is actually worth it for

Active Savings earns its place for a specific saver. If you hold a large cash balance, well above the ISA allowance and past your Personal Savings Allowance anyway, the FSCS spreading and painless switching are worth real money in saved hassle. The same is true if you run a fixed-rate ladder, or if you simply know you will never get round to opening accounts one at a time and would otherwise leave cash rotting in a 1% legacy account.

If your cash comfortably fits in an ISA, an ISA still edges it, because you keep the interest tax-free, and our guide to direct best-buy savings accounts is worth a look if you would rather run a single account yourself. If this is your emergency fund, the easy-access option keeps it reachable within a working day. And worth noting that Active Savings is a cash product only; for a pension the separate HL SIPP is where Hargreaves Lansdown holds your retirement money.

What I am still checking

This is a first look after opening the account and moving real money in, and it passed every test I could run in an afternoon: no fees, the exact amount deposited, a genuinely competitive rate, and clear FSCS labelling. But a savings account earns its verdict over months, not minutes, so a few things are still open. Does the first month's interest actually land, and land on time? Are there any charges that only surface later, on a withdrawal or a transfer out? And the big promise of the whole idea: once that first interest payment arrives, I will move the money to a different partner bank and see whether switching really is the one-click job it claims to be. I will update this review once I have the answers. On what I have seen so far, though, it looks like a genuinely excellent product.

Frequently Asked Questions

Is Hargreaves Lansdown Active Savings any good?

On a hands-on test, yes. It is free, £100 went in with nothing skimmed off, and the top easy-access rate (3.95% in July 2026) beat a Trading 212 ISA at the time. Switching between banks from one login is genuinely quick, and the FSCS labelling is clear. The main thing to know is that interest is taxable once you are past your savings allowance, unless you use the Cash ISA version. Ignore the cashback, which is trivial below £250,000.

Is Hargreaves Lansdown Active Savings safe?

Your money is protected by the FSCS up to £120,000 per person for each partner bank or building society you deposit with, the same protection you would get going to those banks directly. Cash waiting in the hub account is held at Barclays and is also covered. Active Savings is a marketplace, so the protection comes from the underlying banks, not from Hargreaves Lansdown itself.

Does Active Savings charge a fee?

No. It is free to use, with no account fee or upfront cost. When we tested it, £100 paid in arrived as exactly £100 with nothing skimmed off. Hargreaves Lansdown is paid a margin by the partner banks instead, so in theory a specific bank could pay slightly more direct, but in practice the platform rates sit at the top of the market.

Is Active Savings interest taxable?

Yes. Active Savings products are ordinary taxable savings accounts, so the interest counts against your Personal Savings Allowance (£1,000 for basic-rate, £500 for higher-rate, £0 for additional-rate taxpayers). Cash held inside a Cash ISA or a Stocks and Shares ISA earns interest tax-free instead.

Are the Active Savings rates any good?

Yes, better than Hargreaves Lansdown's reputation would suggest. On 2 July 2026 the top easy-access rate on the platform was 3.95% AER, which beat the cash rate on a Trading 212 ISA at the same time, with fixed terms up to 4.6% for three years. Because there is a marketplace margin, a single bank could occasionally pay a touch more direct, but the platform gathers enough competing challenger banks that its top rate sits at the top of the market.

How do I withdraw money from Active Savings?

Withdrawing from an easy-access product to the cash hub takes up to one working day, and moving from the hub to your bank account takes up to another, so allow up to two working days in total. There is no limit withdrawing to a linked HL account; the Cash ISA has a £100,000 daily limit to a nominated bank. Money in fixed-term products is locked until the term ends, and the cash hub itself pays no interest, so do not leave cash sitting in it.

What are the disadvantages of Active Savings?

The main ones: interest is taxable once you pass your savings allowance, unless you use the Cash ISA version; the cash hub pays no interest while money waits there; withdrawals take up to two working days rather than being instant; fixed-term money is locked until maturity; and the headline cashback is worth just £20 on a £10,000 deposit. None are dealbreakers, but they are the trade-offs to weigh.

Sources

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all