Life Insurance UK 2026: When You Actually Need It

Most 'life insurance UK' guides are quote forms in disguise. The first question is whether you need any at all. Here is when you do, and when the answer is no.

Cite this article

Freedom Isn't Free (2026) Life Insurance UK 2026: When You Actually Need It. Available at: https://freedomisntfree.co.uk/articles/life-insurance-uk (Accessed: 18 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Type 'life insurance UK' into Google and the first page is almost entirely quote forms from insurers and comparison sites. The first question - do you actually need it? - is the one nobody asks.

- You need life insurance when someone else depends on your income or you owe a debt that does not die with you (a mortgage, mainly). If neither applies, you almost certainly do not need it.

- Cover should be sized to the gap your death would leave: outstanding mortgage, plus 10x the income your dependants would lose, plus a buffer for childcare. Not a vague 'leave something behind' number.

- Putting any UK life insurance policy in trust takes the payout outside your estate for inheritance tax. It is one form, it is free, and it can save your family 40% on amounts above the £325,000 threshold.

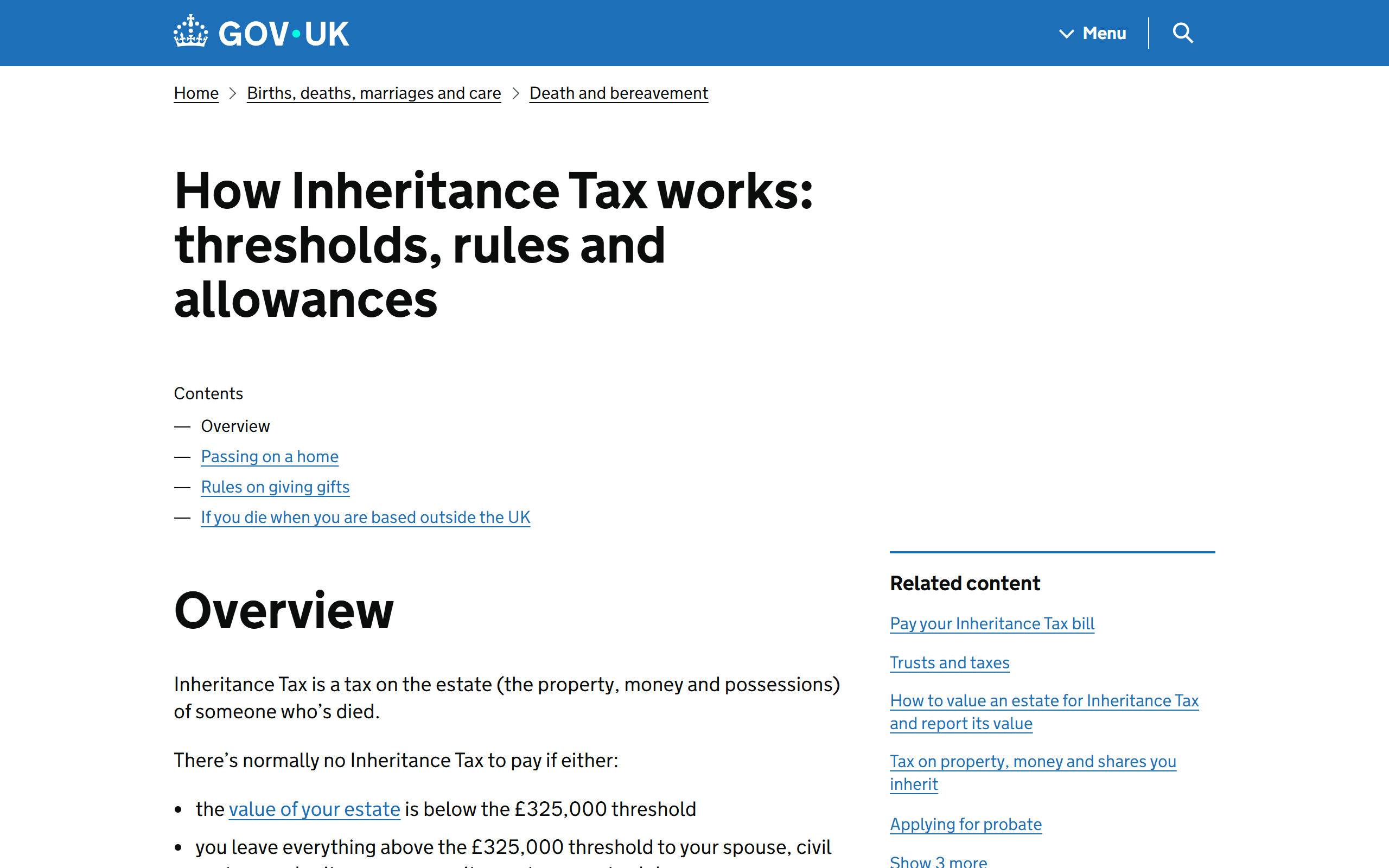

Indicative monthly UK term life insurance cost - £300,000 cover, 20-year level term

Cover roughly doubles in price per decade of age. Smoker status roughly doubles it again. The structural lesson: buy when the need begins, not before, and quit smoking.

Life Insurance UK 2026: When You Actually Need It

Life insurance UK is one of the most-Googled financial products in the country, and the search result it returns is unusual. The top of the page is a wall of quote forms: Legal & General with a £100 gift card, Compare the Market with a £400 voucher, the Post Office at £5 a month. The first independent voice that bothers to ask the real question - do you actually need any of this? - is buried somewhere on page two.

That gap is the entire point of this article. Below is the straight version: when life insurance earns its place, when it does not, how much cover the maths actually says you need, and the IHT trust trick the insurer quote pages will never lead with.

Contents

- What life insurance is really for

- When you actually need life insurance

- When you actually don't need life insurance

- How much cover do you actually need?

- Term, whole-of-life, or decreasing: which job fits

- What life insurance does not cover

- The trust trick that saves your family 40%

- Frequently asked questions

What Life Insurance Is Really For

The marketing language calls it "peace of mind" or "leaving something behind". Both are evasive. Life insurance is income replacement for the people who would lose your income if you died. That is the structural job. Everything else is dressing.

Strip the brochures away and there are only two real reasons a UK adult buys it:

- Someone else depends on the money you earn. Your partner could not pay the mortgage, the bills, the childcare, or all three, on their income alone. If you die, the policy steps in and pays a lump sum that buys them years of breathing room.

- You owe a debt that does not die with you. Almost always a mortgage. The lender still wants paying, and your estate is the first thing they come for. A decreasing-term policy sized to the loan stops the family home being sold to clear the balance.

That is it. If neither of those applies to you, the rest of this article is going to keep telling you the same thing in different ways: most likely you do not need life insurance, and many readers in that position would be better served directing the £5 a month into a Stocks and Shares ISA instead (capital at risk; the value of investments can fall as well as rise).

When You Actually Need Life Insurance

There are five UK situations where the maths makes the policy genuinely earn its place:

- You have a mortgage and a partner who could not service it on their income alone. This is the single biggest case. Decreasing term cover matched to the mortgage term and balance is cheap, simple, and does exactly what it says.

- You have young children, regardless of whether you have a mortgage. A surviving partner caring for two children under ten loses both your income and a chunk of theirs (working hours collapse around school runs and illness). The cover has to plug the income gap until the children are independent, typically a 20 to 25-year term.

- You are the higher earner in a relationship and your partner could not maintain the household on theirs. Same principle, no children required. The dependant is your partner's standard of living, not just their survival.

- You run a small business and your family is exposed to its debts. Personal guarantees on business loans, director's loan accounts, or property held in a sole name all create estate exposure. A term policy ringfences the family from the business.

- You have a large estate likely to face inheritance tax and want the payout to cover the bill so the family does not have to sell the house to settle HMRC. This is whole-of-life territory and gets its own section below.

Notice what is not on this list. A vague desire to leave money behind. Funeral costs. "Just in case". None of those are the structural job of life insurance. There are cheaper and better products for each.

When You Actually Don't Need Life Insurance

The comparison sites have every commercial reason not to spell this out. Five UK situations where the answer is no:

- Single, no children, no mortgage. Nobody depends on your income. The policy pays out to whoever inherits, which is fine, but you have not solved a problem - you have just bought a savings substitute with an actuarial penalty attached.

- Mortgage paid off and children grown. The two original reasons have expired. A lot of UK over-55s carry term policies set up in their 30s purely out of inertia. Cancelling them is often the right call.

- No dependants, modest estate. Below the inheritance tax thresholds (£325,000 nil-rate band, up to £500,000 with the residence nil-rate band per person), nothing useful is being protected. A small life policy on top of an estate that would not have been taxed anyway is solving nothing.

- Your employer's death-in-service cover is already large enough. Many UK employers, particularly in the public sector and large corporates, provide death-in-service benefit at 4x salary or more. For a £50,000 earner that is £200,000 of cover before you have bought a thing. Check your scheme before you buy a private policy on top.

- You are buying it to fund a funeral. A £20-a-month Over 50s plan that pays out £3,000 on death is one of the worst-value products in UK personal finance. Saving £20 a month into a Cash ISA instead leaves your family the same money or more, with none of the breakeven trap.

The principle: if you cannot name the income stream or the liability that the policy is replacing, you do not need it.

How Much Cover Do You Actually Need?

The brochures say "10x your salary" because it is a simple number and it sells. The real answer depends on what you are replacing. Work it out in three parts:

The liability layer. Outstanding mortgage balance. If you have a £250,000 mortgage and 22 years left, that is the floor of your cover. Decreasing term insurance is the right product for this layer because the balance falls every year and you do not need to pay for cover you no longer owe.

The income layer. Net income your dependants would lose, multiplied by the number of years they would need to bridge. A £40,000 net earner with two children under ten and a non-working partner is looking at roughly 18 years until the youngest is independent. £40,000 x 18 is £720,000, which is the upper bound. Most families discount this somewhat because the surviving partner returns to some work and state benefits fill part of the gap. A common rule of thumb is 10x annual income for level term cover, which gets you to £400,000 - usually enough.

The childcare layer. If both parents work and one would have to drop hours significantly after the other died, add the cost of replacement childcare for the years that would last. For one child under five in nursery, that is roughly £15,000 to £18,000 per year of cover gap.

A worked example. A 35-year-old earning £45,000 net with a £230,000 mortgage, a partner working part-time at £15,000, and two children under seven:

- Mortgage cover: £230,000 (decreasing term, 20 years).

- Income cover: £45,000 x 15 = £675,000, discounted to roughly £400,000 (level term, 20 years).

- Childcare cover: £15,000 x 8 = £120,000 (rolled into the level term).

Total: roughly £230,000 of decreasing term plus £520,000 of level term, both with 20-year terms. For a healthy 35-year-old non-smoker the combined monthly premium is typically £20 to £35 a month. That is the cost of insuring a £45,000 income across the years it would matter most.

That is the maths. The "leave something behind" headline number on most quote pages does not survive contact with it.

Term, Whole-of-Life, or Decreasing: Which Job Fits

Three UK product types, three different jobs.

Decreasing term. Cover falls each year, roughly matching a repayment mortgage balance. Cheapest of the three because the average cover across the term is half the starting amount. The right product for mortgage protection and nothing else.

Level term. Cover stays flat for the whole term. The right product for income replacement, where the gap your death leaves does not shrink over time. Roughly 20% to 40% more expensive than decreasing term for the same starting cover.

Whole-of-life. Cover never ends. Pays out whenever you die, including at 99. Two legitimate UK use cases: covering an expected inheritance tax bill so your family does not have to sell assets to settle HMRC, or providing for a lifelong dependant (often a disabled adult child). For everyone else it is a poor fit because you are paying premiums for cover you no longer need. The "Over 50s Plans" sold heavily on UK daytime TV are a guaranteed-acceptance subset of whole-of-life that mostly fails the breakeven test for anyone in normal health.

The full term-vs-whole-of-life comparison, including worked breakeven examples, is in Term vs Whole-Life Insurance UK.

What Life Insurance Does Not Cover

Three protection gaps people regularly assume their life cover plugs, and it does not:

Critical illness. A standard life policy pays out on death, not diagnosis. If you survive cancer, a heart attack, or a stroke, the life policy does not pay. Critical illness cover is a separate product that pays a lump sum on diagnosis of a defined condition. It can be bought standalone or bolted onto a life policy, and it roughly triples the premium.

Lost income from illness or accident. This is what income protection is for. It pays a monthly income (typically 50% to 65% of your gross salary) when you cannot work due to illness or injury, after a deferred period. For most working-age UK adults without large savings, this is a more useful product than life insurance, and the consumer guides barely mention it.

Suicide in the first year. Most UK life policies exclude suicide in the first 12 to 24 months. After that, suicide is covered. This is not a moral judgement by the insurer; it is an anti-selection rule that has been standard in UK protection contracts for over a century.

Fraud and non-disclosure. If you did not declare a medical condition you knew about - a GP visit, a recurring symptom, a medication - the insurer can void the policy at the point of claim. This is where families actually get burned. Declare everything, including things you think are irrelevant. Get your GP record via the NHS App before applying and read it. The underwriter decides what is material, not you.

The Trust Trick That Saves Your Family 40%

A life insurance payout, by default, lands in your estate. If the total estate is above the inheritance tax thresholds, the excess is taxed at 40% before it reaches your family.

The 2026/27 IHT thresholds per HMRC:

- Nil-rate band: £325,000 per person.

- Residence nil-rate band: up to a further £175,000 if you leave your main home to direct descendants, taking the effective threshold to £500,000 per person.

- Combined for a married couple or civil partners: up to £1,000,000 if both thresholds are fully used.

- Rate above the threshold: 40%.

Now consider a homeowner with a £350,000 house, £50,000 in savings, and a life insurance policy paying £300,000 on death. The estate is £700,000. With the full RNRB available, the taxable amount is £200,000. The IHT bill is £80,000. The life insurance payout is what pushed the estate over the threshold.

Write the same policy in trust and the payout goes directly to the named beneficiaries, completely outside the estate. The estate drops to £400,000, comfortably below the RNRB threshold. The IHT bill is zero. The family keeps the full £300,000 rather than handing 40% of the excess to HMRC.

Setting up a trust takes one form. Every major UK insurer (Aviva, Legal & General, Royal London, AIG, Vitality) provides the trust deed free and will set it up at point of purchase, or at any time after. There is no cost, no tax penalty, and almost no downside for the vast majority of policyholders. If you take only one thing from this article, take this: ask the insurer to set the policy up in trust on day one.

The only people who should pause before writing a policy in trust are those with genuinely complex family arrangements (children from a previous marriage, vulnerable beneficiaries, expected disputes). Those cases want proper estate-planning advice, not a standard trust form. For everyone else, it is the cheapest, fastest, most pro-consumer move on the entire product.

Read Next

- Aviva Life Insurance Review 2026: Honest UK Take - the editorial review the comparison sites forgot, with the "from £5 a month" reverse-engineering and the IHT trust trick most buyers miss.

- Term vs Whole-Life Insurance UK: Which Wins in 2026 - the worked breakeven maths on whole-of-life, the over-50s plan trap, and the narrow niche where lifetime cover actually pays.

- Income Protection vs Critical Illness UK - the two protection products UK working-age adults actually need to think about, with the maths on which one pays out.

- Insurance for FIRE - which protection policies still earn their place once you have built real savings, and which you can let lapse.

- Inheritance Tax UK Guide - the nil-rate band, residence nil-rate band, gifting rules, and the strategies (including life insurance in trust) that keep more of your estate with your family.

- Emergency Fund UK - the cash tier that sits underneath every insurance decision. Without one, no policy fixes the right problem.

Further Reading:

Die With Zero - Bill Perkins - Perkins's argument is that the goal is to die with as close to zero as possible. That reframes the entire question of what life insurance is for. If you are leaving a fortune by accident, you have under-spent on your own life. The book sharpens the case for sizing cover to actual dependants and known liabilities rather than a vague "leave them something" target. (Affiliate link - we may earn a small commission at no extra cost to you.)

Frequently Asked Questions

Is it worth getting life insurance in the UK?

It is worth it if someone depends on your income or you have a mortgage that would saddle your family with debt if you died. It is not worth it if you have no dependants, no mortgage, and a modest estate. The real test is whether you can name the income stream or liability the policy is replacing. If you cannot, the £5 a month is better invested in an ISA.

Who is best for life insurance in the UK?

There is no single best provider. The cheapest like-for-like quote varies by age, health, smoker status, and cover amount. Based on publicly-quoted comparison-site pricing as of mid-2026, Royal London is often competitive on level term and is mutual-owned, Legal & General is frequently competitive for older applicants, Aviva is solid but rarely the lowest quote, and Vitality can come in cheaper for engaged users of its wellness app. Rankings between insurers shift regularly; get at least three quotes from an FCA-authorised broker before buying.

What does Martin Lewis say about life insurance?

Martin Lewis's MoneySavingExpert site has publicly recommended shopping around through a regulated broker, getting at least three quotes, and disclosing every medical detail on the application. It has generally taken a sceptical view of guaranteed-acceptance "Over 50s Plans" unless the applicant has no other underwriting options. The site does not push any specific provider, and has consistently noted that many UK adults do not need life cover at all. MSE also flags writing the policy in trust as a free, high-impact step most buyers miss. Always check the current MoneySavingExpert guide direct for the latest position.

What is the best age to buy life insurance?

The best time to buy is when the structural reason first applies: when you take out a mortgage, when a child arrives, or when a partner becomes financially dependent. Buying earlier than that is paying for years of cover you do not need. Buying later means premiums have climbed (cover roughly doubles in price per decade of age) and any new health issues will be on the application. Buy when the need begins, not before and not after.

Can someone with a pacemaker get life insurance?

Yes, but the underwriting will load the premium and may restrict the term. Standard underwritten cover is usually available to applicants with stable, well-managed cardiac conditions, though at materially higher prices than a healthy applicant. For those who cannot get standard cover at any price, guaranteed-acceptance "Over 50s" whole-of-life products exist as a fallback, with the structural drawbacks discussed above. A specialist protection broker is worth their fee for any non-standard health profile.

How long should I get life insurance for?

Match the term to the structural need. For mortgage protection, match the remaining mortgage term. For income replacement with dependent children, run the term until the youngest is financially independent, typically a 20 to 25-year policy. For partner-only income replacement, run it until your planned retirement age, when pension income takes over. Longer terms cost more in total premiums but lock in a healthier-life price for the full duration.

Disclosure: This article is general consumer information, not financial advice. Life insurance is a regulated product; for advice specific to your circumstances, consult an FCA-authorised protection broker or independent financial adviser. Tax rules, allowances and thresholds change at each UK Budget and Autumn Statement; the 2026/27 figures cited above are current at time of publication. Indicative premium ranges are illustrative based on publicly-quoted comparison-site pricing and will vary significantly by applicant health, occupation, and lifestyle. Where the article references Stocks and Shares ISAs as an alternative use of cash, your capital is at risk and the value of investments can fall as well as rise; past performance is not a guarantee of future results. Freedom Isn't Free is not FCA-authorised.

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all