Mortgage Overpayment Calculator: Save Thousands in Interest

An extra £200 a month against your mortgage. Most people refuse to do the sum because the answer makes the case for ordering takeaways feel obscene.

Cite this article

Freedom Isn't Free (2026) Mortgage Overpayment Calculator: Save Thousands in Interest. Available at: https://freedomisntfree.co.uk/articles/mortgage-overpayment-calculator-guide (Accessed: 5 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Overpaying on your mortgage can significantly reduce the total interest paid over the life of the loan.

- The mortgage overpayment calculator helps you see how much interest you can save and how many years you can cut off your mortgage term by overpaying.

- Making overpayments reduces your outstanding capital, which lowers future interest charges and allows more of your monthly payment to go towards reducing the principal.

- Using the calculator is simple: enter your mortgage details and the amount you plan to overpay each month to see the benefits.

Mortgage Overpayment Calculator: Save Thousands in Interest

For most people in the UK, a mortgage is the single largest financial commitment they will ever make. Over a typical 25- or 30-year term, the total interest paid can be staggering - often tens of thousands of pounds on top of the amount you actually borrowed. But it does not have to be that way.

Mortgage overpayments - paying more than your required monthly amount - are one of the simplest and most effective ways to reduce the total cost of your home. Even modest extra payments can shave years off your mortgage and save you a significant amount of money.

We built a mortgage overpayment calculator to help you see exactly what difference overpaying could make to your specific situation. This article walks through how overpayments work, how to use the calculator, and the practical considerations you should think about before committing extra money to your mortgage.

Contents

- How Mortgage Overpayments Work

- How to Use the Calculator

- Worked Example: The Power of 200 a Month

- Lump-Sum Overpayments: One-Off vs Monthly

- Overpay vs Invest: The Eternal Debate

- Practical Considerations Before You Overpay

- The Pension Lump Sum Strategy

- Frequently Asked Questions

How Mortgage Overpayments Work

When you make your standard monthly mortgage payment, a portion goes towards interest and a portion goes towards paying down the capital (the amount you originally borrowed). In the early years of a mortgage, the split is heavily weighted towards interest. This is why mortgages feel like they barely move for the first few years.

When you make an overpayment, the extra money goes directly towards reducing your outstanding capital. This has a compounding effect: because the balance is now lower, the interest charged in the following month is also lower. A larger share of your next standard payment then goes towards capital rather than interest. Over time, this snowball effect can be substantial.

There are two ways overpayments typically work:

- Reduced term - Your monthly payment stays the same, but you finish paying off the mortgage sooner.

- Reduced payment - Your term stays the same, but your monthly payment drops at the next rate review.

Most UK lenders default to reducing the term, which is generally the better option if your goal is to minimise total interest paid. Our calculator models the reduced-term approach so you can see how many months you could cut from your mortgage.

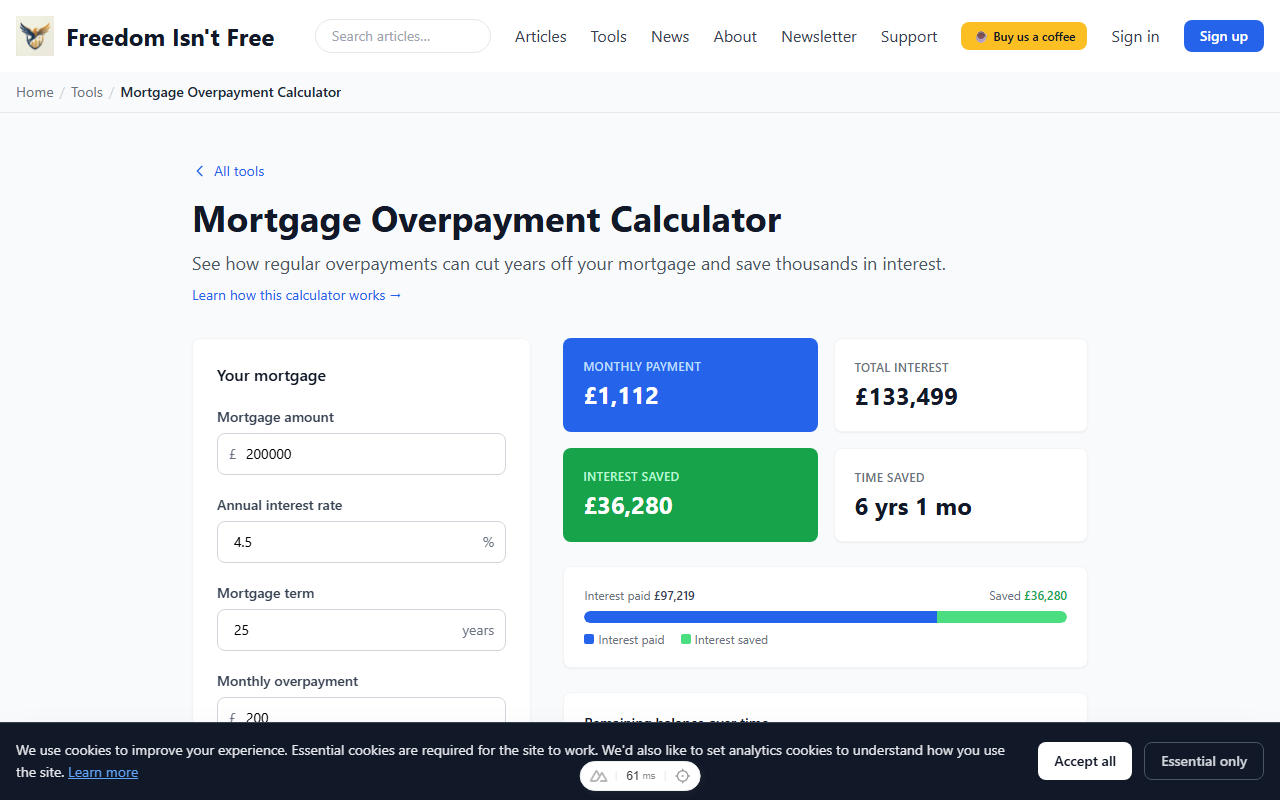

How to Use the Calculator

The mortgage overpayment calculator is designed to be straightforward. Here is how to use it step by step:

- Enter your mortgage amount - This is your current outstanding balance, not the original amount you borrowed. You can find this on your latest mortgage statement.

- Enter your annual interest rate - Your current mortgage rate as a percentage. If you are on a fixed rate, use that figure. If you are on a tracker or SVR, use your current rate.

- Enter your mortgage term - The remaining number of years on your mortgage.

- Add a monthly overpayment amount - The extra amount you want to pay each month on top of your required payment.

Once you have entered these details, the calculator will show you a side-by-side comparison of your standard repayment schedule versus the overpayment scenario. You will see:

- Total interest saved over the life of the mortgage

- Years and months cut from your mortgage term

- A visual chart comparing both scenarios over time

If you are logged in, you can also save your inputs to your financial profile so you can revisit them later or compare different overpayment amounts.

Worked Example: The Power of £200 a Month

Let us put some real numbers to this. Consider a fairly typical UK mortgage:

- Mortgage balance: £200,000

- Interest rate: 4.5% per year

- Term: 25 years

- Monthly overpayment: £200

Without overpayments, your standard monthly repayment would be approximately £1,111. Over the full 25-year term, you would pay around £133,400 in total interest. That is a lot of money on top of the £200,000 you borrowed.

Now add a £200 monthly overpayment, bringing your total monthly payment to £1,311. The results are striking:

- You would pay off your mortgage roughly 7 years early, finishing in around 18 years instead of 25.

- You would save approximately £39,000 in interest over the life of the mortgage.

- Your total cost of borrowing drops from around £133,400 to approximately £94,400.

That is nearly £40,000 saved by finding an extra £200 per month. To put it another way, every £1 you overpay effectively "earns" you a guaranteed, tax-free return equal to your mortgage interest rate.

£200,000 mortgage balance over time: standard vs +£200/month overpay

Same starting balance, same 4.5% rate. The overpayment line clears the loan around year 19.

Source: 25-year repayment mortgage, £200,000 starting balance, 4.5% interest rate.

Want to see what the numbers look like for your situation? Try the mortgage overpayment calculator with your own figures.

Lump-Sum Overpayments: One-Off vs Monthly

The calculator now supports a one-off lump sum input alongside the monthly overpayment field. The two interact in useful ways:

- Monthly overpayment is a steady extra amount on top of your standard payment, applied every month for the life of the mortgage. It builds compounding interest savings slowly but reliably.

- Lump sum is a single chunk applied at the start of the calculation. Useful for modelling an inheritance, a bonus, a maturing fixed-rate ISA, or any other windfall.

A lump sum is mathematically more powerful per pound than the equivalent monthly overpayment because it reduces the principal immediately, removing more interest from the rest of the term. £10,000 paid as a lump sum on day one of a 25-year £250,000 mortgage at 4.5% saves roughly £15,000 in interest and shaves about 18 months off the term. The same £10,000 spread over the next 50 months as £200/month overpayments saves around £11,000 and a similar 18 months. The lump sum wins on interest because it gets to work earlier.

You can combine both. Many readers use the calculator to model "I'll pay this £15,000 lump sum from my savings now, and I can find another £150 a month from my pay rise". The combined effect is bigger than either alone.

One caveat: most UK mortgages cap penalty-free overpayments at 10% of the outstanding balance per year while you're on a fixed-rate deal. A £30,000 lump sum on a £250,000 mortgage might trigger an early repayment charge on the £5,000 over the 10% allowance. Check your mortgage terms before paying anything that crosses the cap.

Overpay vs Invest: The Eternal Debate

One of the most common questions in personal finance is whether you are better off overpaying your mortgage or investing the money instead.

The argument for investing is simple: if you can earn a higher return in the stock market than your mortgage interest rate, you come out ahead by investing. Historically, global equities have returned around 8-10% per year before inflation over long periods. If your mortgage rate is 4.5%, the expected gap is meaningful.

The argument for overpaying is equally compelling: paying down your mortgage is a guaranteed, risk-free, tax-free return equal to your interest rate. There is no volatility, no sequence-of-returns risk, and no chance of loss. You also reduce your monthly obligations, giving you more flexibility if your income changes.

In practice, many people find a middle path works best. They overpay enough to stay on track for an earlier payoff date, while also investing regularly in an ISA or pension. The "right" answer depends on your mortgage rate, your risk tolerance, your tax situation, and how far you are from financial independence.

If you want to model the investment side of this equation, our compound interest calculator can help you compare the two approaches.

Practical Considerations Before You Overpay

Before you start sending extra money to your lender, there are a few things to check.

Early Repayment Charges

Most UK fixed-rate mortgages include early repayment charges (ERCs) if you pay off too much of the balance during the fixed period. These are typically 1-5% of the amount overpaid above the allowed limit. ERCs can easily wipe out the benefit of overpaying, so check your mortgage terms carefully.

The 10% Annual Overpayment Allowance

The good news is that most UK fixed-rate mortgages allow you to overpay by up to 10% of your outstanding balance per year without incurring any charges. On a £200,000 mortgage, that means you could overpay up to £20,000 in the first year without penalty - more than enough for most people.

If you are on a tracker rate or your lender's standard variable rate, there is usually no limit on overpayments.

Should You Overpay or Top Up Your ISA and Pension First?

This is where it gets personal. There are strong arguments for prioritising tax-advantaged accounts before mortgage overpayments:

- Pension contributions receive tax relief at your marginal rate (20%, 40%, or 45%). A £100 pension contribution only costs you £80 if you are a basic-rate taxpayer, or £60 if you are a higher-rate taxpayer. That is hard to beat.

- ISA contributions grow completely tax-free. If you have not used your £20,000 annual ISA allowance, investing within an ISA may be more efficient than overpaying a mortgage at 4-5%.

- If you are on the path to financial independence, building investments that generate passive income is likely more valuable than reducing a low-interest debt. Our FI number calculator can help you figure out your target.

A sensible order of priority for many people looks like this:

- Build an emergency fund (3-6 months of expenses)

- Capture any employer pension match

- Pay off high-interest debt (credit cards, personal loans)

- Max out ISA contributions

- Then consider mortgage overpayments with any surplus

That said, if your mortgage rate is high (above 5-6%) and you have already covered the basics, overpaying becomes a more attractive option. The psychological benefit of reducing debt should not be underestimated either - for some people, knowing their mortgage is shrinking faster is worth more than the potential extra return from investing.

Tracking Your Progress

As you build wealth and pay down debt, it is worth keeping a clear picture of where you stand. Our net worth tracker lets you see all your assets and liabilities in one place, so you can watch your mortgage balance fall alongside your investment portfolio growing.

The Pension Lump Sum Strategy

If you are approaching retirement age with a mortgage still outstanding, there is another angle worth exploring. When you access your defined contribution pension, you can take up to 25% as a tax-free lump sum. Using that lump sum to clear or substantially reduce your mortgage can be one of the most tax-efficient moves available.

We covered this in detail in our article on the pension tax-free lump sum mortgage strategy. The short version: because the lump sum is tax-free and mortgage interest is paid from post-tax income, using one to eliminate the other delivers a guaranteed return with no tax drag.

This is particularly relevant if you are in your late 40s or early 50s and deciding whether to aggressively overpay now or rely on the pension lump sum later. The answer depends on the size of your pension pot, your mortgage balance, and how comfortable you are carrying the debt into your late 50s.

Frequently Asked Questions

Is it worth overpaying my mortgage by a small amount?

Yes. Even £50 or £100 per month makes a difference over the life of a 25-year mortgage. On a £200,000 mortgage at 4.5%, an extra £100 per month would save you around £20,000 in interest and cut roughly 4 years off your term. Small, consistent overpayments add up significantly over time.

Can I get my overpayments back if I need the money?

It depends on your lender. Some mortgages have an overpayment reserve or "borrow back" facility that lets you reclaim overpayments in an emergency. Others do not - once the money is paid, it is gone until you remortgage or sell. Check with your lender before relying on overpayments as a form of savings.

Should I overpay my mortgage or pay off my student loan?

For most UK borrowers, mortgage overpayments are a better use of money than early student loan repayment. Student loans are written off after 25-40 years depending on the plan, and repayments are income-contingent. Unless you are on a high income and close to clearing the balance, the student loan often behaves more like an additional tax. We covered this in more detail in our article on whether you should pay off your student loan.

What happens to my overpayments if I remortgage?

Your overpayments reduce your outstanding balance, so when you remortgage, you will be borrowing less. This means lower monthly payments, a shorter term, or both. It can also help you access better rates if the lower balance pushes you into a more favourable loan-to-value bracket (for example, dropping below 75% or 60% LTV).

Is there a best time to start overpaying?

The earlier you start, the more you save. Overpayments made in the early years of a mortgage have the greatest impact because your balance is at its highest and so is the interest being charged. That said, it is never too late to start - even overpayments made halfway through your term will save you money.

Start Running the Numbers

The best way to understand the impact of overpayments on your specific mortgage is to see it for yourself. Enter your details into the calculator and compare the two scenarios side by side.

Try the mortgage overpayment calculator

Whether you decide to overpay aggressively, invest instead, or do a bit of both, the important thing is that you are making an informed decision based on your own numbers rather than rules of thumb. That is what financial freedom looks like in practice.

Further Reading:

I Will Teach You To Be Rich - Ramit Sethi - Covers the practical mechanics of automating your finances, including how to handle mortgage payments alongside investing and saving. (Affiliate link - we may earn a small commission at no extra cost to you.)

The Psychology of Money - Morgan Housel - Helps you think clearly about the emotional side of financial decisions like whether to overpay your mortgage or invest. (Affiliate link - we may earn a small commission at no extra cost to you.)

Read Next

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all