Compound Interest Calculator: How It Works

Einstein supposedly called compound interest the eighth wonder of the world. The wonder isn't the maths. It's what 30 years of nothing does to £10,000.

Cite this article

Freedom Isn't Free (2026) Compound Interest Calculator: How It Works. Available at: https://freedomisntfree.co.uk/articles/compound-interest-calculator-guide (Accessed: 21 May 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Compound interest is interest earned on both your original investment and the interest that has already been added.

- Compound interest allows your returns to generate their own returns, leading to accelerated growth over time.

- To use the compound interest calculator, enter your initial investment, monthly contributions, expected interest rate, time period, and compounding frequency.

- The longer you invest and the more frequently interest compounds, the faster your money grows.

Compound Interest Calculator: How It Works

Albert Einstein is often credited with calling compound interest the eighth wonder of the world. Whether he actually said it or not, the idea holds up. Compound interest is the single most powerful force available to ordinary investors, and understanding it can change the way you think about saving and investing for the rest of your life.

We built a free compound interest calculator to help you see exactly how your money could grow over time. In this article, we will explain what compound interest is, walk you through how to use the calculator, and share practical tips for making the most of it.

Contents

- What Is Compound Interest?

- How to Use the Compound Interest Calculator

- Common Use Cases

- The Maths Behind Compound Interest

- Tips to Maximise Compound Interest

- Author's Take

- Frequently Asked Questions

What Is Compound Interest?

Compound interest is interest earned on both your original investment and on the interest that has already been added. In other words, your returns start generating their own returns.

Compare this with simple interest, where you only earn interest on the original amount. With simple interest, growth is linear. With compound interest, growth accelerates over time because your base keeps getting larger.

Here is a concrete example. Suppose you invest 10,000 pounds into a Stocks and Shares ISA earning an average of 7% per year. After one year, you have 10,700 pounds. In the second year, you earn 7% on 10,700 pounds - not just the original 10,000. That gives you 11,449 pounds. The difference seems small early on, but over 20 or 30 years the effect becomes dramatic.

After 10 years, your 10,000 pounds grows to roughly 19,672 pounds. After 20 years, it reaches around 38,697 pounds. After 30 years, it becomes approximately 76,123 pounds - all without adding a single extra penny. That is compound interest at work.

Inside a Stocks and Shares ISA, this growth is entirely tax-free, making it one of the best vehicles for UK investors to build long-term wealth.

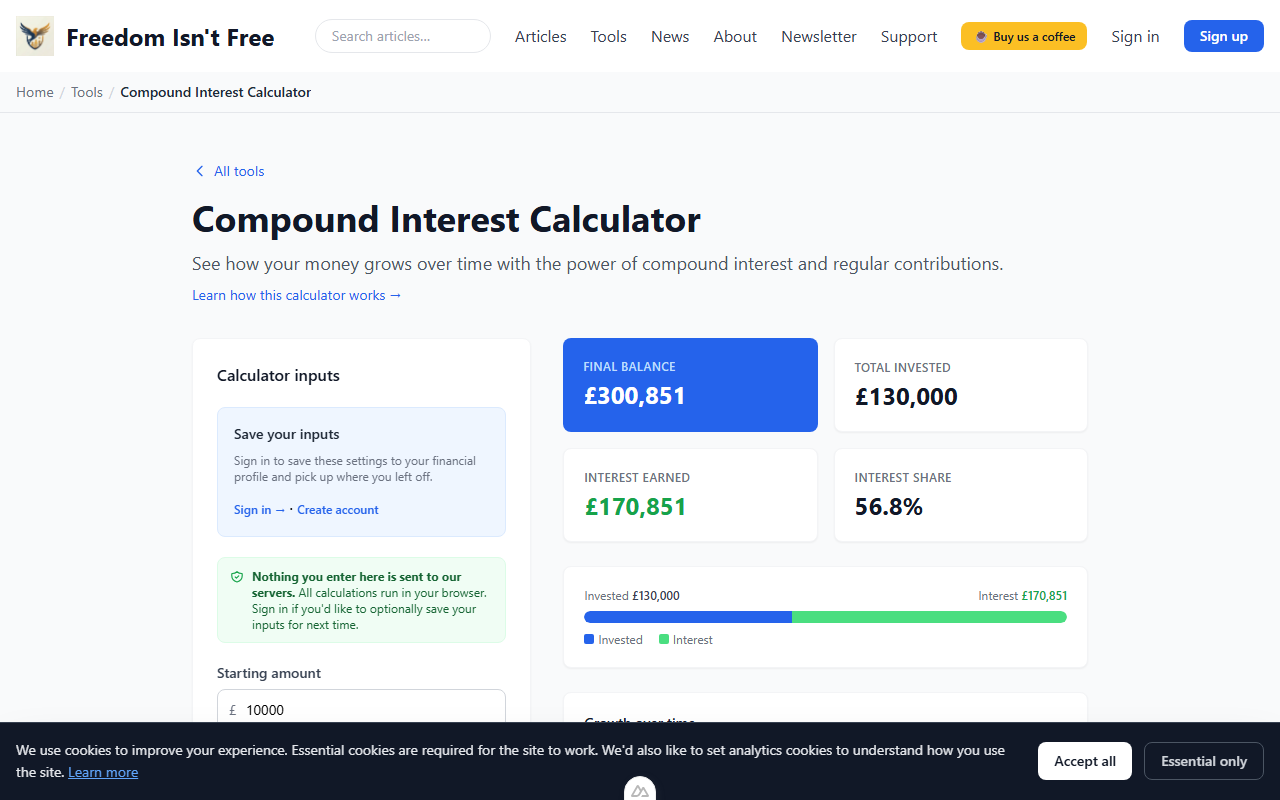

How to Use the Compound Interest Calculator

Our compound interest calculator is designed to be straightforward. Here is how to use it step by step:

Step 1: Enter Your Initial Investment

Type in the lump sum you are starting with. This could be your current ISA balance, a savings pot, or even zero if you are starting from scratch.

Step 2: Set Your Monthly Contribution

Enter the amount you plan to add each month. Even small regular contributions make a significant difference over time. If you have already set up a budget, you will know exactly how much you can afford to put aside.

Step 3: Choose Your Interest Rate

Enter the annual rate of return you expect. For a diversified portfolio of low-cost index funds, a common assumption for long-term nominal returns is 7-8% per year. For cash savings, current rates tend to sit between 3-5%. Be realistic here - the output is only as useful as the inputs.

Step 4: Set the Time Period

Enter the number of years you plan to invest. The longer the time horizon, the more dramatic the compounding effect becomes.

Step 5: Choose Compounding Frequency

Select how often interest is compounded: daily, monthly, or yearly. Most investment platforms compound daily or monthly. The more frequently interest compounds, the faster your money grows, though the difference between daily and monthly compounding is usually small.

Step 6: Review Your Results

The calculator displays a growth chart showing how your money increases over time, along with a year-by-year breakdown table so you can see exactly what is happening at each stage. You can also export your results to CSV for your own records or further analysis.

If you are logged in, you can save your inputs to your financial profile to revisit them later or compare different scenarios.

Common Use Cases

ISA Planning

The annual ISA allowance for the 2026/27 tax year is 20,000 pounds. Use the calculator to model what happens if you max out your ISA each year versus contributing a smaller monthly amount. Seeing the long-term projections can be a strong motivator to prioritise your ISA contributions.

SIPP Retirement Planning

A Self-Invested Personal Pension (SIPP) benefits from tax relief on contributions, which effectively boosts your investment. If you contribute 800 pounds, the government tops it up to 1,000 pounds (for basic rate taxpayers). Plug these boosted figures into the calculator to see how your retirement pot could grow. Once you know your target number, check our FI number calculator to see when you might be able to step away from work.

General Investment Account (GIA)

Not everything fits inside an ISA or SIPP. A General Investment Account has no contribution limits, but gains are subject to Capital Gains Tax. Use the calculator to project your GIA growth, keeping in mind that the actual returns after tax will be somewhat lower than the headline figure.

Saving for a House Deposit

If you are saving for a first home, the calculator can help you figure out how long it will take to reach your target deposit. You might also consider a Lifetime ISA, which adds a 25% government bonus on contributions up to 4,000 pounds per year. Model different monthly savings amounts to find a realistic timeline.

The Maths Behind Compound Interest

The standard compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

- A = the final amount

- P = the principal (your initial investment)

- r = the annual interest rate (as a decimal, so 7% = 0.07)

- n = the number of times interest compounds per year

- t = the number of years

For example, 10,000 pounds at 7% compounded monthly for 10 years:

A = 10,000 x (1 + 0.07/12)^(12 x 10) = 10,000 x (1.005833)^120 = approximately 20,097 pounds.

When you add regular monthly contributions, the formula becomes more involved. That is exactly why the calculator exists - so you do not need to do this by hand.

Tips to Maximise Compound Interest

Start as Early as Possible

Time is the most important ingredient in compounding. Someone who invests 200 pounds per month from age 25 will almost certainly end up with more than someone who invests 400 pounds per month from age 35, even though the late starter contributes more money overall. Every year you delay costs you future growth.

Make Regular Contributions

Lump sums are great, but consistent monthly investing is what most people can actually sustain. Set up a direct debit into your ISA or SIPP so that investing happens automatically. This also smooths out the price you pay for investments over time, a concept known as pound cost averaging.

Reinvest Dividends

If your investments pay dividends, reinvest them rather than taking them as cash. Reinvested dividends buy more shares, which generate more dividends, which buy more shares. This is compounding in its purest form. Most platforms offer an automatic reinvestment option - make sure it is switched on.

Keep Costs Low

Fund fees eat directly into your returns, and the damage compounds just like your growth does. A fund charging 1.5% per year will cost you tens of thousands of pounds more over a 30-year period compared to one charging 0.1%. Stick with low-cost index trackers where possible.

Track Your Progress

Use our net worth tracker alongside the compound interest calculator to monitor how your actual results compare with your projections. Seeing your wealth grow in real time reinforces good habits and keeps you motivated during the inevitable market dips.

Know Your Target

If you are pursuing financial independence, calculate your FIRE number first. Then use the compound interest calculator to work backwards and figure out how much you need to save each month to get there.

Frequently Asked Questions

What is a good interest rate to assume for long-term investing?

For a globally diversified equity portfolio, many UK investors use 7-8% as a nominal long-term average. If you want to be conservative or account for inflation, try 4-5%. Cash savings rates vary and are currently between 3-5%, but they rarely keep up with inflation over long periods.

Does the calculator account for inflation?

The calculator shows nominal returns. To estimate real (inflation-adjusted) growth, subtract an assumed inflation rate from your interest rate. For example, if you expect 7% nominal returns and 2.5% inflation, enter 4.5% to see your purchasing power growth.

How often should interest compound for best results?

More frequent compounding produces slightly higher returns. Daily compounding beats monthly, which beats yearly. In practice, the difference between daily and monthly compounding is small. Most investment platforms compound on a daily basis.

Is compound interest only relevant for stocks?

No. Compound interest applies to any situation where returns are reinvested. This includes savings accounts, bonds, peer-to-peer lending, and property (if rental income is reinvested). The principle is the same - your returns generate further returns.

How much difference do monthly contributions really make?

A huge difference. Starting with 5,000 pounds and adding 200 per month at 7% for 25 years gives you roughly 186,000 pounds. Without those monthly contributions, the same 5,000 pounds grows to only about 27,000 pounds. Regular contributions are the engine that drives long-term wealth building.

Get Started

Numbers on a page are one thing. Seeing your own projections is another. Try the compound interest calculator now and model different scenarios for your ISA, SIPP, or general investments. Even a few minutes of experimenting can give you a much clearer picture of where your money is heading.

Further Reading:

The Psychology of Money - Morgan Housel - A brilliant exploration of how behaviour and patience matter more than financial knowledge when it comes to building wealth through compounding. (Affiliate link - we may earn a small commission at no extra cost to you.)

The Little Book of Common Sense Investing - John Bogle - The definitive case for low-cost index fund investing, which pairs perfectly with a long-term compounding strategy. (Affiliate link - we may earn a small commission at no extra cost to you.)

Read Next

Enjoying the content?

If this site has been useful, a coffee goes a long way.