FI Number Calculator: Your Independence Target

Financial independence has a number. You don't have to wonder. Plug in what you spend and what you save, and the year you stop needing a salary lands on the screen in seconds.

Cite this article

Freedom Isn't Free (2026) FI Number Calculator: Your Independence Target. Available at: https://freedomisntfree.co.uk/articles/fi-number-calculator-guide (Accessed: 21 May 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Your FI number is the amount of money you need to live off your investment returns indefinitely.

- To calculate your FI number, multiply your expected annual expenses in retirement by 25.

- The FI number calculator helps you determine your portfolio size and time to reach financial independence.

- Use the calculator to enter your annual expenses, current portfolio value, annual savings, and expected return rate.

- Review your results to understand your financial independence target and progress.

FI Number Calculator: Your Independence Target

Financial independence starts with a single number. Not a vague hope, not a rough guess, but a hard target you can plan around and track over time. Your FI number is the portfolio size at which your investments can cover your living costs indefinitely, freeing you from the need to work for money.

Our FI number calculator does the maths for you. Enter your annual expenses, current savings, and expected returns, and it tells you exactly how much you need and how long it will take to get there.

Contents

- What Is a FI Number?

- How to Use the Calculator

- Common Use Cases

- How Savings Rate Affects Time to FI

- Adjustments for UK Investors

- Frequently Asked Questions

What Is a FI Number?

Your FI number is the total amount of invested capital you need before you can live off your portfolio's returns. It is based on the 4% rule, which states that if you withdraw 4% of your portfolio in your first year of retirement and adjust for inflation each year after, your money has a roughly 95% chance of lasting at least 30 years.

The calculation is simple: multiply your expected annual expenses in retirement by 25.

FI Number = Annual Expenses x 25

If you plan to spend £30,000 per year, your FI number is £750,000. If you need £40,000, you are targeting £1,000,000. The 25x multiplier is just the inverse of the 4% withdrawal rate - nothing more complicated than that.

For a deeper look at how this rule was derived and what its limitations are, read our full breakdown on calculating your FIRE number. And if you want to understand why UK investors may need to adjust that 4% figure, our review of Beyond the 4% Rule covers the evidence.

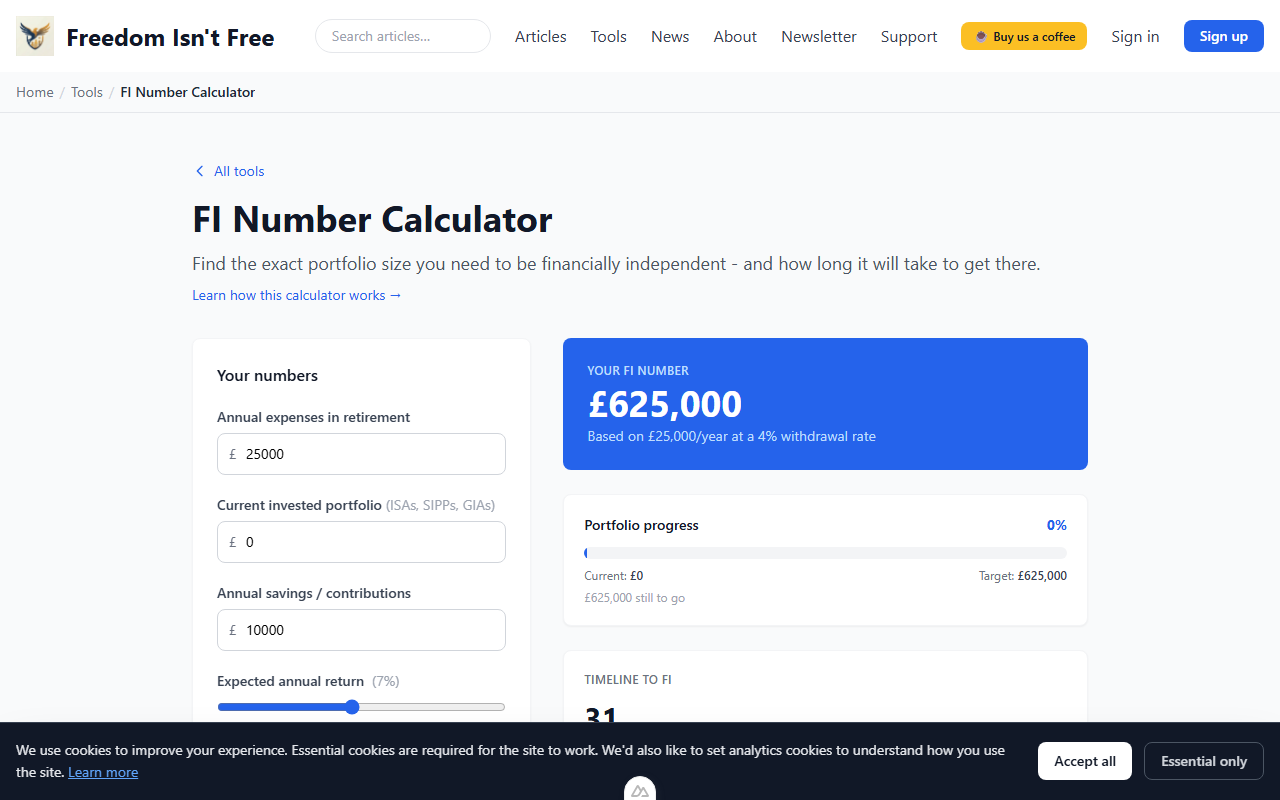

How to Use the Calculator

The FI number calculator is designed to give you a clear answer in under a minute. Here is how to use it step by step.

1. Enter Your Annual Expenses

Start with what you expect to spend each year in retirement. If you are not sure, look at your last 12 months of bank statements and subtract costs that disappear when you stop working (commuting, work lunches, professional clothing). Our budgeting 101 guide can help you build an accurate picture of your spending.

2. Add Your Current Portfolio Value

Enter the total value of your invested assets. This includes ISAs, SIPPs, GIAs, and any other investments you plan to draw from in retirement. If you are not sure of the total, use the net worth tracker to get an up-to-date figure.

3. Set Your Annual Savings

How much are you putting away each year? This is the amount going into investments, not just sitting in a savings account. The calculator uses this figure alongside your expected return rate to project how quickly your portfolio will grow.

4. Choose Your Expected Return Rate

A common assumption is 7-8% nominal or 4-5% real (after inflation). The calculator lets you adjust this to match your own expectations. If you hold a global equity index fund, historical real returns of around 5% are a reasonable starting point. Use the compound interest calculator to see how different return assumptions change your projections over time.

5. Review Your Results

The calculator shows your FI number, your current progress as a percentage, and the estimated number of years until you reach financial independence at your current savings rate. It also includes a reverse mode where you can enter a target retirement age and see what savings rate you would need to hit that deadline.

6. Choose Your Portfolio Type

The tool supports ISA, SIPP, and GIA portfolio types, so you can see how each wrapper affects your path to FI. This matters because SIPP contributions come with tax relief, while ISA withdrawals are tax-free. The right mix depends on your income, your planned retirement age, and whether you want access to funds before 57.

7. Save to Your Profile

If you are logged in, you can save your inputs to your financial profile. This means you can come back and update your numbers as your situation changes without starting from scratch each time.

Common Use Cases

Early Retirement Planning

The most common reason to calculate a FI number is to plan for early retirement. If you want to stop working at 45 or 50, you need a clear target and a timeline. The calculator shows whether your current savings rate is enough, or whether you need to increase contributions, reduce expenses, or both.

Setting Savings Targets

Once you know your FI number, you can work backwards to a monthly savings target. If you need £750,000 in 15 years and you have £100,000 today, the calculator will show you exactly how much to save each month to close that gap at a given return rate.

Comparing Scenarios

Run the calculator multiple times with different inputs. What happens if you cut expenses by £5,000 a year? What if you increase your savings rate by 5%? What if returns are lower than expected? Comparing scenarios helps you build a plan that works even if things do not go perfectly.

How Savings Rate Affects Time to FI

Your savings rate is the single most important variable in reaching financial independence. It matters more than investment returns, more than income, and more than clever tax planning. A higher savings rate works in two directions at once: it increases the money flowing into your portfolio and it reduces the expenses your portfolio needs to cover.

Here is how savings rate affects the number of years to reach FI, assuming a 5% real return and starting from zero.

| Savings Rate | Years to FI |

|---|---|

| 10% | 51 |

| 20% | 37 |

| 30% | 28 |

| 40% | 22 |

| 50% | 17 |

| 60% | 12.5 |

| 70% | 8.5 |

| 80% | 5.5 |

The relationship is not linear. Moving from a 10% to a 20% savings rate shaves off 14 years. Moving from 70% to 80% only saves 3 years. The biggest gains come from getting your savings rate above 30-40%, where the timeline starts to compress dramatically.

Adjustments for UK Investors

The standard FI number formula works globally, but UK investors have two major advantages worth building into their plans.

State Pension Bridging

If you retire early, you will not receive the State Pension until age 66 (rising to 67 and eventually 68). But once it kicks in, the full new State Pension pays around £11,500 per year. That reduces your required portfolio withdrawals significantly.

This means your true FI number has two phases. Before State Pension age, your portfolio needs to cover all your expenses. After State Pension age, it only needs to cover the gap between your pension income and your total spending. The calculator helps you plan for both phases.

ISA and SIPP Sequencing

UK investors have access to two powerful tax-advantaged wrappers, and the order in which you draw from them matters.

- SIPPs offer upfront tax relief (20% or 40% depending on your marginal rate) and tax-free growth, but you cannot access funds until age 57 (from April 2028). Withdrawals are taxed as income.

- ISAs offer no upfront tax relief, but growth and withdrawals are completely tax-free with no age restriction.

- GIAs (General Investment Accounts) have no tax advantages but no restrictions either.

A common strategy is to live off ISA and GIA funds in early retirement, then switch to SIPP withdrawals once you reach pension age. This keeps your taxable income low in the early years while your SIPP continues to grow tax-free. Running separate scenarios for each wrapper in the calculator helps you see how this sequencing affects your timeline.

Frequently Asked Questions

Is the 4% rule safe for early retirees?

The original research behind the 4% rule was based on a 30-year retirement. If you plan to retire at 40 and live to 90, that is a 50-year drawdown period. Over longer periods, a withdrawal rate of 3.25-3.5% is more conservative. You can adjust the calculator's assumptions to reflect a lower withdrawal rate by simply increasing your annual expenses figure.

Should I include my house in my FI number?

No. Your FI number should only include liquid, invested assets that generate returns you can withdraw from. Your home keeps a roof over your head, but it does not produce income unless you sell it or rent part of it out.

What about inflation?

If you use a real (inflation-adjusted) return rate in the calculator, your FI number is already in today's money. A 5% real return means 5% after inflation, so the output reflects purchasing power, not just nominal pounds.

How does the State Pension change my FI number?

Once you reach State Pension age, the pension effectively reduces your annual expenses by the amount it pays. If your expenses are £30,000 and the State Pension pays £11,500, your portfolio only needs to cover £18,500 from that point on. That is a FI number of £462,500 instead of £750,000 - a significant reduction.

Can I use this calculator if I have a defined benefit pension?

Yes. Treat any guaranteed pension income the same way as the State Pension. Subtract the annual pension amount from your expected expenses, and use the reduced figure as your annual spend in the calculator. This gives you a lower, more accurate FI number.

Start Calculating

Your FI number is not a fantasy figure. It is a concrete, calculable target. Once you know what it is, every pound you save and invest moves you measurably closer.

Try the FI number calculator and find out exactly where you stand.

Further Reading:

Quit Like a Millionaire - Kristy Shen - A practical guide to reaching financial independence and retiring early, with clear worked examples on calculating your FI number and optimising your savings rate. (Affiliate link - we may earn a small commission at no extra cost to you.)

The Psychology of Money - Morgan Housel - Explores why behaviour and mindset matter more than spreadsheets on the path to financial independence. (Affiliate link - we may earn a small commission at no extra cost to you.)

Read Next

Enjoying the content?

If this site has been useful, a coffee goes a long way.