Lifetime ISA UK Guide: Bonus, Rules and Pitfalls

The Lifetime ISA offers free money on day one and a penalty that quietly leaves you with less than you put in. Both halves are true. Most savers only learn the second one too late.

Cite this article

Freedom Isn't Free (2026) Lifetime ISA UK Guide: Bonus, Rules and Pitfalls. Available at: https://freedomisntfree.co.uk/articles/lifetime-isa-uk-guide (Accessed: 25 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- A Lifetime ISA lets you save up to £4,000 a year and gets you a 25% government bonus, worth up to £1,000 annually.

- You can open one between ages 18 and 39, contribute until 50, and use it tax-free for a first home (up to £450,000) or from age 60 in retirement.

- Withdraw for any other reason and you pay a 25% penalty, which actually leaves you worse off than your original contribution.

- A LISA is the exception to the multi-ISA rule: you can only subscribe to one LISA per tax year, even after April 2024.

Lifetime ISA UK Guide: Bonus, Rules and Pitfalls

The Lifetime ISA is one of the most generous savings products the UK government has ever offered, and one of the most misunderstood. Open one between 18 and 39, drip in £4,000 a year, and HMRC tops it up with £1,000 of free money. Over the maximum window from 18 to 50, that's up to £32,000 in pure bonus. Few financial products give you a guaranteed 25% return on day one.

But the LISA is also a trap if you misuse it. The withdrawal penalty isn't really 25%. It's an asymmetric clawback that leaves you with less than you put in. And the eligibility rules around first-time buyer status, property price caps, and mortgage type are tighter than most people realise.

This guide walks you through every angle: how the bonus works, the age and contribution limits, when a LISA beats a pension or a regular ISA, and the situations where you should walk away.

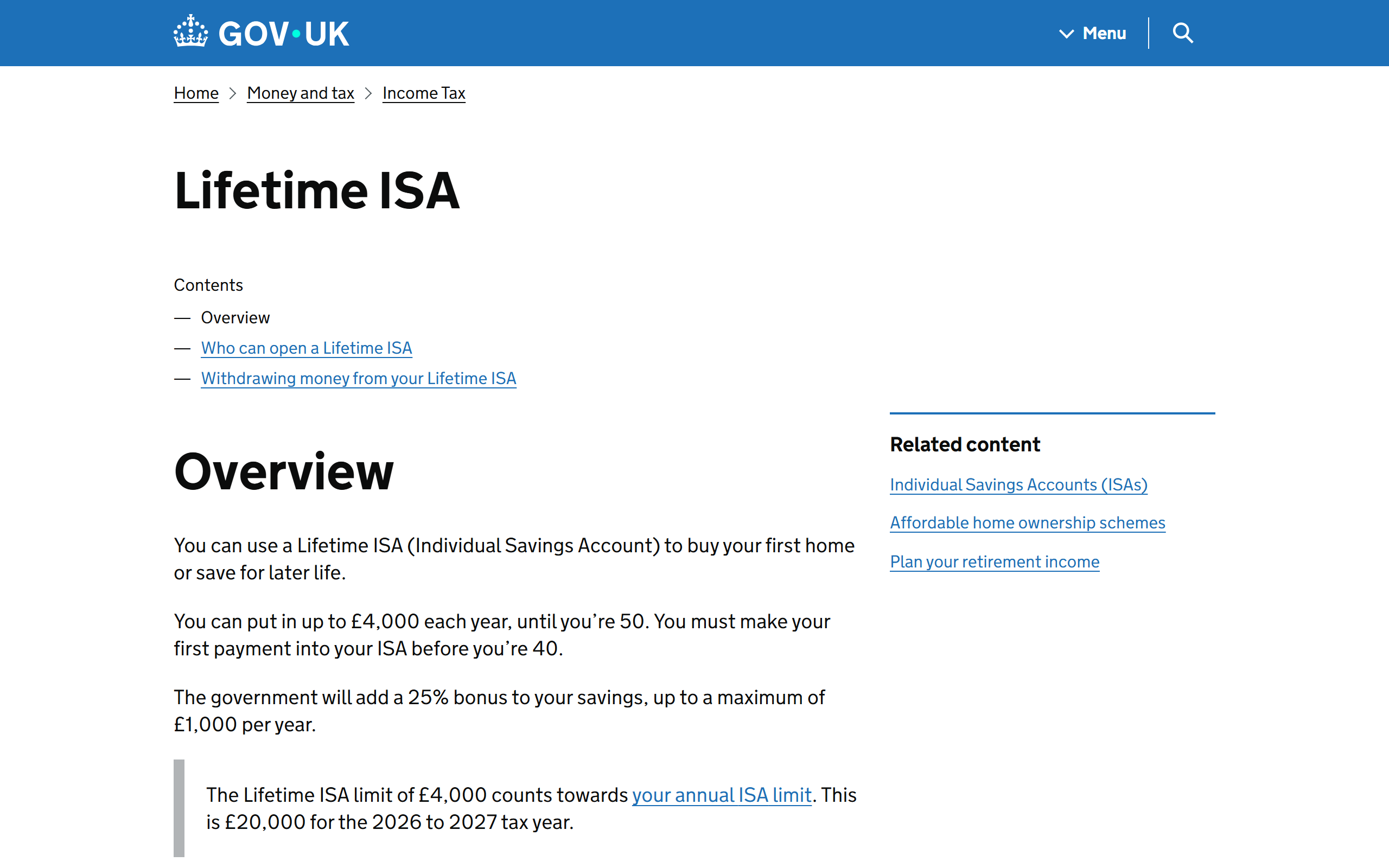

What Is a Lifetime ISA?

A Lifetime ISA (LISA) is a tax-free savings account introduced by the UK government in April 2017. It was designed to help younger savers do one of two things: buy their first home or save for retirement. You can do both with the same account, but you can only access the money penalty-free for those two specific purposes (or in the unfortunate event of terminal illness).

There are two flavours:

- Cash LISA: works like a savings account, with a fixed or variable interest rate.

- Stocks and Shares LISA: lets you invest in funds, ETFs, and shares for long-term growth.

Most providers offer one or the other, not both. If you're using a LISA for retirement (i.e. holding it for decades), a Stocks and Shares LISA almost always wins because cash interest tends to lose to inflation over long horizons. If you plan to buy a home in the next two or three years, a Cash LISA is the safer choice because you don't want a stock market wobble to delay your purchase. If you have decided on the investing route, our Stocks and Shares Lifetime ISA comparison lines up the providers that actually offer one and the fees they charge.

Full official details are on gov.uk's Lifetime ISA page and at MoneyHelper.

How the 25% LISA Bonus Works

The headline feature is the government bonus. For every £1 you contribute, the government adds 25p, up to a maximum bonus of £1,000 per tax year (which corresponds to the £4,000 contribution cap).

The bonus is paid monthly, usually four to nine weeks after your contribution lands. It goes straight into your LISA and starts earning interest or investment returns immediately. You don't need to claim it. You don't need to fill anything in. Your provider does it for you.

A few things worth knowing:

- The bonus counts as your money once it's paid. It grows alongside your contributions.

- If you withdraw for a non-qualifying reason, the bonus is clawed back as part of the penalty (more on this below).

- The bonus does not count towards your £4,000 LISA limit or your £20,000 overall ISA allowance. It's pure top-up.

If you max your LISA every year from 18 to 50, that's 32 years of £1,000 bonuses, or £32,000 of free money before any investment growth. Compounded at a real return of 5%, that bonus alone could be worth somewhere north of £75,000 by age 60.

LISA Rules: Age Limits and Contribution Caps

The age and contribution rules are where most people trip up.

- You must be aged 18 to 39 to open a LISA. If you're 40 or over, you cannot open one. Period.

- You can keep contributing until age 50. After your 50th birthday, no more contributions, but the account stays open and any investments keep growing.

- Contribution limit: £4,000 per tax year. This counts towards your overall £20,000 ISA allowance, leaving £16,000 for other ISA types.

- Only one LISA subscription per tax year. Since April 2024, you can pay into multiple ISAs of the same type in one year, but the LISA is the exception. You can still only fund one LISA per tax year.

That last point catches a lot of people out. The 2024 multi-ISA reform was widely reported as "you can now have as many ISAs as you like", but LISAs were excluded from the change. Open a second LISA and try to contribute to both in the same tax year and HMRC will eventually unwind it.

You can transfer an existing LISA between providers, which doesn't count as a new subscription. If your current provider's rates are rubbish, transfer rather than opening a new one.

Using a LISA for a First Home

This is what most people open a LISA for, and the rules are stricter than the marketing makes them sound.

To use your LISA for a house purchase without penalty:

- You must be a genuine first-time buyer. That means you've never owned property anywhere in the world. Inherited a 5% share of your gran's flat in Spain ten years ago? You're disqualified.

- The property must cost £450,000 or less. This cap hasn't moved since 2017, despite a decade of house price inflation. In London and the South East, this is increasingly tight.

- You must use a repayment mortgage. No interest-only, no cash purchase (with one exception for purchases via a conveyancer in specific circumstances).

- Your LISA must have been open for at least 12 months before you can use the funds for a house purchase.

- You must intend to live in the property as your main residence. It can't be a buy-to-let.

The £450,000 cap is the big one to watch. If you're buying jointly and both partners have LISAs, you can both use them on the same property, doubling the bonus. But the property itself still has to be £450k or less.

If you go over the cap by even £1, you can't use your LISA without triggering the withdrawal penalty. That's a real risk in a rising market: you save diligently for years, then prices push every suitable property above the cap, and your LISA becomes effectively locked up until age 60.

Using a LISA for Retirement

The other qualifying use is retirement. From your 60th birthday, you can withdraw your LISA balance, including all bonuses and growth, completely tax-free, for any reason.

This makes the LISA a genuine alternative or complement to a pension for some savers. Compared to a pension, which the LISA stacks against in interesting ways:

- LISA: 25% bonus on contributions, tax-free withdrawals from 60.

- Pension: typically 20-45% tax relief on contributions, 25% tax-free at access age (currently 55, rising to 57 in 2028), rest taxed as income.

For a basic-rate taxpayer with no employer match, the LISA is often more generous than a pension on the way out, because pension withdrawals beyond the 25% tax-free portion get taxed as income. For higher-rate taxpayers with employer matching, the pension wins comfortably.

The LISA is also useful for the early retirement crowd as a bridging account once you hit 60 but before any state pension or defined benefit pension kicks in.

One edge case: self-employed workers without an employer pension match often find LISAs the cleanest retirement vehicle in their 20s and 30s.

LISA vs Help to Buy ISA vs Stocks and Shares ISA

Quick comparison for first-time buyers and retirement savers:

| Feature | Lifetime ISA | Help to Buy ISA | Stocks and Shares ISA |

|---|---|---|---|

| Status | Open to new accounts | Closed to new accounts since Nov 2019 | Open |

| Bonus | 25% on up to £4,000/year | 25% on up to £12,000 lifetime | None |

| Property price cap | £450,000 UK-wide | £250k (£450k in London) | No cap |

| Use for retirement? | Yes, from 60 tax-free | No | Yes, anytime tax-free |

| Penalty for non-qualifying withdrawal | 25% (worse than no bonus) | None (just lose bonus) | None |

| Annual contribution limit | £4,000 | £2,400 | £20,000 |

If you already have a Help to Buy ISA, you can keep contributing until November 2029, but the LISA bonus is more generous for most savers. You can transfer a Help to Buy ISA into a LISA, though it counts towards the £4,000 LISA limit.

The Stocks and Shares ISA wins on flexibility and contribution headroom. It loses on the bonus. Most serious savers use both.

The 25% Withdrawal Penalty Trap

Here's the part the marketing buries. The 25% withdrawal penalty is asymmetric, and that asymmetry costs you money.

Walk through the maths:

- You contribute £4,000.

- The government adds the 25% bonus: £5,000 total.

- You withdraw early for a non-qualifying reason. The penalty is 25% of the withdrawal amount, not of your contribution.

- 25% of £5,000 = £1,250 penalty.

- You receive £3,750.

You contributed £4,000. You walked away with £3,750. The "25% penalty" is actually a 6.25% loss on your own money, on top of clawing back the bonus.

This is by design. The Treasury wants the LISA used for the two qualifying purposes. If you're not certain you'll use it for a first home or wait until 60, think hard before opening one.

The trap snaps shut hardest on people who:

- Save into a LISA, then find every suitable property is above £450k.

- Save into a LISA, then need the money for an emergency.

- Save into a LISA, then decide to buy with a partner who already owns property (you're no longer a first-time buyer in the eyes of the scheme if you go on the deeds, but you can still keep the LISA for retirement).

If you're saving for a house in an area where the £450k cap is tight, hedge your bets. Keep some money in a Stocks and Shares ISA or a Cash ISA where there's no penalty.

Should You Open a LISA?

Open a LISA if:

- You're a UK resident aged 18 to 39.

- You're saving for a first home in an area where £450k buys something realistic.

- You're a basic-rate taxpayer or self-employed and want a retirement supplement with cleaner tax treatment than a pension at withdrawal.

- You can comfortably commit £4,000 a year to a long-term goal without needing it for emergencies.

Skip the LISA if:

- You already own property and aren't sure you'll wait until 60.

- You're a higher-rate taxpayer with an employer pension match (use the pension first).

- You're house-hunting in central London or other high-cost areas where £450k won't get you a flat, let alone a house.

- Your emergency fund isn't built. The penalty makes a LISA an awful place to keep cash you might need.

For most readers in their 20s and early 30s saving for a first home, opening a LISA on day one of eligibility and contributing the maximum is close to a no-brainer. The 25% bonus is hard to beat anywhere else, especially when paired with tax-free growth that escapes the gradually expanding stealth tax thresholds.

Just don't put money in that you might need back early. Treat the LISA as locked away until you either complete on a first home or turn 60.

Frequently Asked Questions

Can I have a LISA and a Stocks and Shares ISA in the same year?

Yes. The LISA counts as one ISA type, and a Stocks and Shares ISA is another. You can fund both in the same tax year, as long as your total contributions don't exceed the £20,000 ISA allowance and your LISA contribution doesn't exceed £4,000. From April 2024 onwards you can also pay into multiple Stocks and Shares ISAs in one year, but you can still only fund one LISA.

What happens to my LISA if I move abroad?

If you become non-UK resident, you can keep your LISA open and any existing balance keeps growing, but you cannot make new contributions and you don't get the bonus on any new money. If you return to UK residency later, you can resume contributions (assuming you're still under 50).

Can I use my LISA to buy a flat with a partner who isn't a first-time buyer?

You personally must be a first-time buyer to use your LISA for a house purchase without penalty. If your partner already owns property and you're buying jointly, you cannot use your LISA for that purchase without triggering the 25% withdrawal penalty. You can keep the LISA going and use it for retirement at 60 instead.

What if my house purchase falls through after I've withdrawn the LISA?

If a qualifying purchase fails, your conveyancer must return the funds to your LISA provider within 90 days. The money goes back into the LISA without penalty and without losing the bonus. This is one of the key reasons the funds flow through your conveyancer rather than directly to you.

Is a LISA better than a pension for retirement?

It depends on your tax band and employer benefits. For a basic-rate taxpayer with no pension match, a LISA often beats a pension because withdrawals are fully tax-free from 60, while pension withdrawals are mostly taxed as income. For higher-rate taxpayers, especially those with generous employer matches, the pension wins. Most early retirees benefit from holding both: pension for the tax relief during peak earning years, LISA and Stocks and Shares ISA for flexibility and tax-free withdrawals.

Read Next

- ISA vs Pension: Which Is Right for You?

- Stocks and Shares ISA: A UK Investor's Guide

- Junior ISA UK Guide

- UK Pensions Explained

- The New Tax Year UK Investor Checklist

Further Reading:

I Will Teach You To Be Rich - Ramit Sethi - A practical playbook for automating contributions to tax-advantaged accounts like the LISA so the bonus compounds without you thinking about it. (Affiliate link - we may earn a small commission at no extra cost to you.)

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all