Junior ISA UK: The Complete 2026/27 Guide

Most British parents open the wrong type of Junior ISA out of habit. By the child's 18th birthday, the default has quietly cost them the price of a small car. The fix is one form.

Cite this article

Freedom Isn't Free (2026) Junior ISA UK: The Complete 2026/27 Guide. Available at: https://freedomisntfree.co.uk/articles/junior-isa-uk-guide (Accessed: 25 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

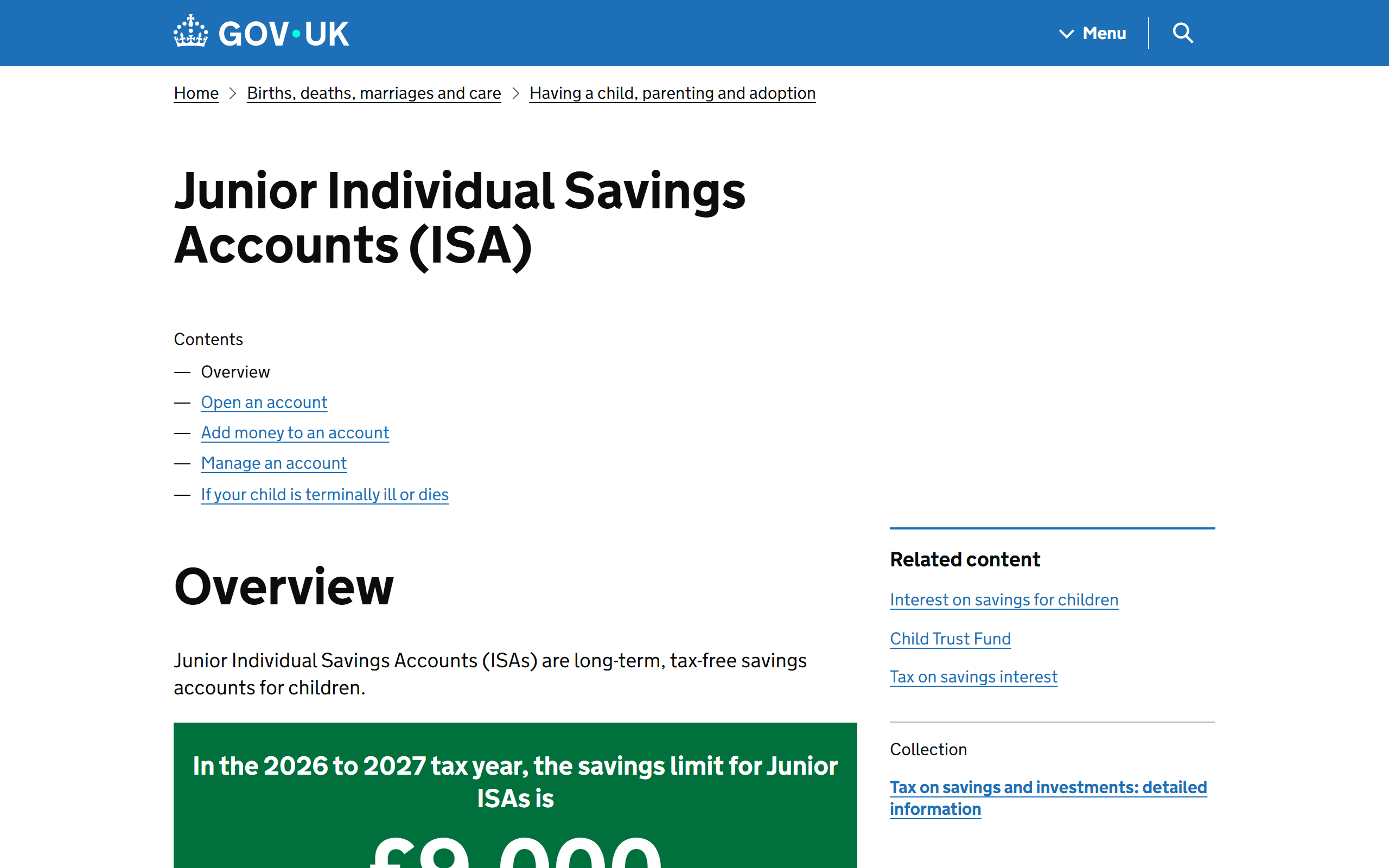

- The 2026/27 Junior ISA allowance is £9,000 per child, paid in by anyone, growing tax-free

- A Stocks and Shares JISA almost always beats a Cash JISA over an 18-year horizon

- The money legally belongs to the child and they get full control at 18

- £100 per month from birth at 7% growth becomes roughly £43,000 by age 18

Junior ISA UK: The Complete 2026/27 Guide

A Junior ISA is the most tax-efficient way to save or invest for a child in the UK, and most parents either ignore it completely or stick the money in a low-paying cash account and call it a day. Both are mistakes. Used properly, a JISA gives your child an 18-year head start that almost no adult ever gets, with every penny of growth shielded from tax for the entire ride.

This guide covers exactly how the JISA UK rules work in 2026/27, the difference between Cash and Stocks and Shares versions, who can contribute, what happens at 18, and the maths that makes this wrapper genuinely powerful. If you have a child or grandchild under 18 who is UK resident, this is one of the easiest financial decisions you will ever make.

Contents

- What Is a Junior ISA?

- How Much Can You Put in a JISA in 2026/27?

- Cash JISA vs Stocks and Shares JISA

- Who Can Open a Junior ISA?

- What Happens When the Child Turns 18?

- JISA vs Other Ways to Save for a Child

- The Power of Compounding for 18 Years

- Frequently Asked Questions

What Is a Junior ISA?

A Junior ISA is a tax-free savings or investment account for UK-resident children under the age of 18. It works on the same basic principle as an adult ISA: you pay money in, the money grows free of income tax and capital gains tax, and when it comes out the other side there is no tax to pay either.

The key differences from an adult ISA are the lower annual allowance, the fact that the account must be opened by a parent or legal guardian, and the rule that the money is locked away until the child turns 18. There is no flexibility on that last point. You cannot dip into a JISA for school fees, a family holiday, or any other reason. The money is the child's, legally, and it stays untouched until they become an adult.

There are two flavours: the Cash JISA, which behaves like a savings account, and the Stocks and Shares JISA, which lets you invest in funds, shares, and ETFs. A child can hold one of each at the same time, but only one of each. You can transfer between providers, but you cannot have two Cash JISAs running side by side.

For the official rulebook, the gov.uk Junior ISA page is the source of truth, and HMRC's Savings and Investment Manual covers the technical detail.

How Much Can You Put in a JISA in 2026/27?

The 2026/27 JISA allowance is £9,000 per child, per tax year. That limit is shared across both types of JISA combined. So you could put £9,000 into a Stocks and Shares JISA, or £4,500 in each, or £9,000 into a Cash JISA. What you cannot do is put £9,000 into one and another penny into the other.

The allowance resets every 6 April and does not roll over. Anything you do not use is gone for good. For most families this is academic, because £9,000 a year is a serious commitment - that is £750 a month, or £173 a week. The vast majority of JISA contributions are nowhere near the cap.

Anyone can contribute. Parents, grandparents, godparents, aunts, uncles, friends - it does not matter. The money is paid into the child's account and immediately becomes the child's property. This is genuinely useful at birthdays and Christmas, and it is the cleanest way for grandparents to gift money without inheritance tax complications, provided they live for seven more years or stay within the annual gifting allowance.

One thing to flag: a child cannot have a Junior ISA and a Child Trust Fund at the same time. CTFs were the predecessor to the JISA and were issued to children born between 1 September 2002 and 2 January 2011. If your child has a dormant CTF sitting somewhere, you can transfer it into a JISA, and you almost certainly should because JISAs tend to have lower fees and better investment options.

Cash JISA vs Stocks and Shares JISA

This is where most parents get it wrong. The default instinct is to open a Cash JISA because it feels safer, and "safe" is what we want for our kids. But over an 18-year horizon, cash is not safe. It is almost guaranteed to underperform inflation, which means the money your child receives at 18 buys less than the money you paid in.

A Cash JISA pays interest. In 2026 the best rates sit around 4 to 5%, which sounds fine until you remember that UK inflation has averaged closer to 3% over the long run and spiked well above that recently. After inflation, cash returns are usually flat or slightly negative.

A Stocks and Shares JISA invests in the markets. Over the last century, a globally diversified equity portfolio has returned roughly 7% a year after inflation. Eighteen years is more than enough time to ride out the inevitable crashes, and the longer your runway, the more confident you can be in the long-term return.

Here is the maths. £100 a month for 18 years:

- In a Cash JISA earning 4%, you end up with around £31,000

- In a Stocks and Shares JISA earning 7%, you end up with around £43,000

That is a £12,000 difference for the same money in, simply because you chose to invest rather than save. If you max out the £9,000 allowance every year (£750 a month), the gap is enormous: roughly £232,000 in cash at 4% versus £325,000 in equities at 7%.

£100 a month for 18 years: Cash JISA vs Stocks and Shares JISA

The only argument for a Cash JISA is if your child is already 16 or 17 and the money will be withdrawn within a year or two. At that point you cannot afford to ride out a market dip. For anyone with five or more years to go, Stocks and Shares is the obvious choice. Pick a low-cost global index fund inside the JISA and leave it alone. Our Stocks and Shares ISA UK guide goes into detail on fund selection, and the same logic applies to a JISA.

Who Can Open a Junior ISA?

Only a parent or legal guardian can open a JISA. Whoever opens it becomes the "registered contact" and is the only person who can change investments, switch providers, or update the account details. Grandparents cannot open a JISA, no matter how generous they are feeling, but they can absolutely contribute to one that has already been opened.

The child must be:

- Under 18

- UK resident, or a UK Crown servant's dependent living abroad

- Without an existing Child Trust Fund (or the CTF must be transferred in)

Once the JISA is open, the child can take over management of the account at age 16. They can switch providers, change funds, and view the balance. What they cannot do, until their 18th birthday, is take any money out. That rule is iron-clad.

What Happens When the Child Turns 18?

On the morning of their 18th birthday, the JISA automatically converts into an adult ISA. The child gains full control. They can withdraw every penny, leave it invested, transfer it elsewhere, or do whatever they want with it.

This is the part that worries some parents, and it should be discussed honestly. If you put away £325,000 over 18 years and your 18-year-old immediately blows it on a Lamborghini and a gap year, that is legally their right. The money is theirs. Always was.

In practice this is rarely a disaster. Most 18-year-olds, if you have raised them with any kind of conversation about money, do not vaporise their entire fund overnight. The bigger risk is them treating it as free money for university and lifestyle rather than a foundation for later life. The fix is simple: talk to them about it. Show them what it is, explain what compounding does over the next 40 years, and make the case for leaving most of it alone.

If you genuinely do not trust your child with that kind of sum, a JISA might not be the right vehicle. A bare trust or family investment company gives you more control, at the cost of complexity and tax efficiency.

JISA vs Other Ways to Save for a Child

The JISA is not the only option, but it beats most of the alternatives for most families.

Child savings accounts are easy to open and offer instant access, but the interest is taxable above £100 per year if the money came from a parent (the "settlements rule"). Useful for pocket money, useless for serious saving.

Pensions for children are a thing. You can open a SIPP for a child and pay in up to £2,880 a year, which the government tops up to £3,600 with basic-rate tax relief. The catch is that the child cannot touch it until age 57 or later. That is excellent for retirement, terrible for a house deposit at 25.

Premium Bonds for children are popular and tax-free, but the average return is well below inflation and you are essentially gambling on the prize draw.

General investment accounts in the parent's name work, but you pay tax on dividends and capital gains, and you have to remember to gift the money formally if you want it ringfenced for the child.

The JISA wins on tax efficiency, simplicity, and the fact that the money is locked in for the child's benefit. The honest competitor is a child SIPP, and most families should do both: a JISA for university, a deposit, or a head start in their twenties; a SIPP for retirement at 60+. Once they are working, they can build their own wrappers, including a Lifetime ISA for their first home or retirement.

The Power of Compounding for 18 Years

Compounding is the entire reason this wrapper exists in its current form. Eighteen years of tax-free growth, with no withdrawals, is one of the cleanest demonstrations of compound interest you will ever see in a real-world financial product.

Run the numbers in our compound interest calculator and the pattern becomes obvious. The money you put in during the first five years does the heaviest lifting, because it compounds for 13 to 18 years. Money paid in at age 16 has barely two years to grow.

This is why starting early matters more than starting big. £50 a month from birth ends up worth more than £150 a month starting at age 12, despite the smaller total contributions, because the early money has another decade in the market.

If you can max the JISA every year from birth - £9,000 a year for 18 years at 7% - your child receives roughly £325,000 on their 18th birthday. If they leave it untouched and let it compound for another 40 years at the same rate, they retire with millions, without contributing another penny. That is the kind of head start that quietly changes a family's financial trajectory across generations.

Further Reading

The Psychology of Money - Morgan Housel - The single best primer on long-term thinking, patience, and the behavioural side of compounding. If you want your child to actually leave that JISA untouched at 18, this is the book to hand them. (Affiliate link - we may earn a small commission at no extra cost to you.)

I Will Teach You To Be Rich - Ramit Sethi - Practical, no-nonsense guide to automating savings and investments. The principles map directly onto setting up a JISA and never thinking about it again. (Affiliate link - we may earn a small commission at no extra cost to you.)

Frequently Asked Questions

Can I open a Junior ISA for my niece or nephew?

No. Only a parent or legal guardian can open a JISA and become the registered contact. You can, however, contribute to a JISA that the parent has already opened. Have a quiet word with the parent, get the account details, and pay in directly. The money is the child's the moment it lands.

What happens to the JISA if I die before my child turns 18?

The JISA continues exactly as before. The money belongs to the child, not to you, so it is not part of your estate and there is no inheritance tax to pay on it. The registered contact role passes to the surviving parent or guardian. If both parents have died, a court-appointed guardian takes over.

Can my child have both a Cash and a Stocks and Shares JISA?

Yes. They can hold one of each at the same time, with the £9,000 annual allowance split between them however you like. They cannot, however, have two Cash JISAs or two Stocks and Shares JISAs running in parallel. If you want to switch providers, you transfer the existing account rather than opening a second.

Does paying into a JISA count as a gift for inheritance tax?

Yes, contributions count as gifts. They fall under the normal IHT rules: £3,000 annual gifting allowance, £250 small gifts exemption per recipient, or the seven-year rule for larger gifts. Regular contributions out of surplus income can also qualify for the "normal expenditure out of income" exemption, which is genuinely useful for grandparents with healthy pensions.

Can the child access the money before 18 in an emergency?

No. There is no hardship withdrawal, no early access, no exception for medical bills or family crises. The only situation in which a JISA pays out before 18 is if the child becomes terminally ill, in which case HMRC allows early withdrawal on application. For everything else, the lock is absolute. This is by design - the JISA is meant to be a long-term wrapper, and the inflexibility is the price of the tax break.

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all