Is Trading 212 a Scam? The Honest UK Answer

If a UK broker offers free trades, something else is paying the lights. Trading 212 is regulated. The five ways it earns from your account aren't shown on the homepage.

Cite this article

Freedom Isn't Free (2026) Is Trading 212 a Scam? The Honest UK Answer. Available at: https://freedomisntfree.co.uk/articles/is-trading-212-a-scam (Accessed: 24 June 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

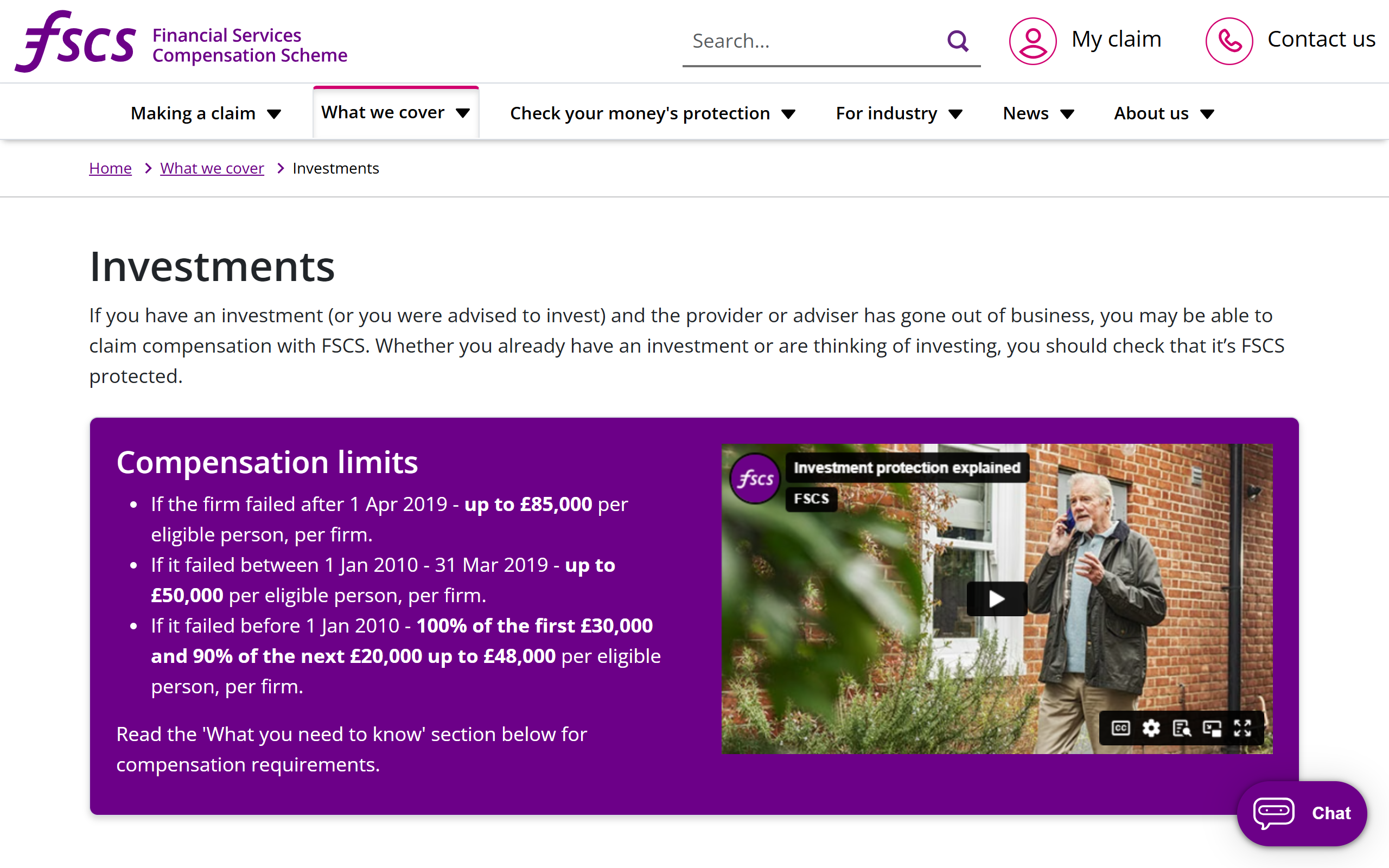

- No, Trading 212 is not a scam. It is authorised and regulated by the UK FCA, your assets are held in segregated custody, and the Invest/ISA accounts are covered by FSCS up to £85,000.

- Trading 212 makes money mainly from CFD spreads (a separate, risky product), securities lending on shares it custodies, currency conversion fees, interest spreads on uninvested cash, and a paid Plus subscription tier.

- It is not selling your personal data, and EU/UK MiFID II rules effectively ban payment for order flow, so that common US suspicion does not apply.

- The legitimate things to know: securities lending exposes lent shares to counterparty risk above the FSCS limit, CFDs are genuinely dangerous (around 75-85% of retail CFD traders lose money), and the FX spread on USD stock purchases is the real "fee" most people miss.

UK broker safety comparison

| Broker | UK regulator | FSCS cover | Client money segregated? |

|---|---|---|---|

| Trading 212 | FCA (FRN 609146) | Up to £85,000 | Yes |

| Hargreaves Lansdown | FCA | Up to £85,000 | Yes |

| AJ Bell | FCA | Up to £85,000 | Yes |

| Interactive Investor | FCA | Up to £85,000 | Yes |

| Freetrade | FCA | Up to £85,000 | Yes |

Same regulatory regime as every other major UK retail broker.

Is Trading 212 a Scam? The Honest UK Answer

No, Trading 212 is not a scam. It is a UK-authorised and FCA-regulated investment firm (FRN 609146 for Trading 212 UK Ltd), it has been operating since 2004, and the cash and assets in its Invest and ISA accounts are protected by the Financial Services Compensation Scheme up to £85,000 per person. People search "is Trading 212 a scam" because anything offering a financial service for free seems to have a catch. There is a catch. It is just not "scam." Here is how Trading 212 makes money and what the legitimate risks are.

Contents

- The short answer

- How Trading 212 is actually regulated

- How Trading 212 actually makes money

- What about payment for order flow?

- The legitimate risks worth knowing

- Common complaints and what they actually mean

- Who Trading 212 is and is not for

- Frequently Asked Questions

The short answer

- Trading 212 is not a scam. It is a regulated UK broker, your money is held separately from the company's own accounts, and you have FSCS protection up to £85,000.

- It makes money in disclosed ways. Mostly CFDs (a separate product), securities lending, FX spreads on currency conversion, interest spread on cash, and the optional Trading 212 Plus subscription.

- It is not free in the way Robinhood was sometimes free. US-style payment-for-order-flow is effectively banned for UK retail brokers under MiFID II.

- Real risks exist but they are about understanding the product, not about Trading 212 ripping you off.

"Commission-free" shifts which fee generates the revenue rather than removing it. Hargreaves Lansdown's 0.45% platform fee is visible. Trading 212's FX spread on a USD stock purchase, or the interest it earns on your uninvested cash, is less visible. Less visible is not the same as fraudulent.

How Trading 212 is actually regulated

The UK retail-facing entity is Trading 212 UK Ltd. Specifics:

- Authorised and regulated by the Financial Conduct Authority (FCA). Reference number 609146. You can search the FCA register yourself to verify.

- Client money rules. Under FCA CASS rules, client cash is held in segregated bank accounts at major banks (Barclays, JPMorgan and others), separate from Trading 212's own balance sheet. If Trading 212 went bust tomorrow, that cash is not part of the bankruptcy estate.

- Custody of shares. Securities held in your Invest and ISA accounts are held by an independent custodian (Interactive Brokers handles a large share of this for Trading 212). Your shares are held in nominee accounts in your beneficial ownership.

- FSCS protection. Up to £85,000 per person, per institution, in the event of Trading 212 itself failing. This covers both cash and securities for the Invest and ISA accounts. Full protection details are explained on the FSCS website.

A separate Trading 212 Markets Ltd entity is authorised by the Cyprus Securities and Exchange Commission (CySEC) and historically handled CFDs for UK clients. After Brexit, UK CFD activity moved under the FCA-regulated entity.

This is the same regulatory regime as Hargreaves Lansdown, AJ Bell, Interactive Investor and Freetrade.

| Broker | UK regulator | FSCS protection | Client money segregation |

|---|---|---|---|

| Trading 212 | FCA (FRN 609146) | Up to £85,000 | Yes |

| Hargreaves Lansdown | FCA | Up to £85,000 | Yes |

| AJ Bell | FCA | Up to £85,000 | Yes |

| Interactive Investor | FCA | Up to £85,000 | Yes |

| Freetrade | FCA | Up to £85,000 | Yes |

How Trading 212 actually makes money

Trading 212 has multiple revenue streams, disclosed in financial statements filed at Companies House:

1. CFD spreads (historically the biggest)

Trading 212 offers Contracts for Difference (CFDs) as a separate product to its Invest/ISA accounts. CFDs are leveraged derivatives where you bet on price movements without owning the underlying asset. The bid-ask spread is Trading 212's main revenue per trade, plus overnight financing fees on positions held longer than a day.

Trading 212's own legally required disclosure states that 75-85% of retail CFD accounts lose money. The broker takes a spread on every trade and overnight fees on every leveraged position. You do not have to use CFDs - the Invest and ISA accounts are completely separate.

2. Securities lending

Shares held in your Invest account (and from late 2024, optionally your ISA account) can be lent to institutions like short-sellers and market-makers. They pay a fee to borrow them. From 2024, Trading 212 shares around 50% of that fee with the customer whose shares were lent. Hargreaves Lansdown, Interactive Brokers, Charles Schwab and Vanguard all do this to varying degrees.

The risk: lent shares are technically owed back rather than held in custody. T212 has collateral arrangements, but for amounts above the £85,000 FSCS limit, counterparty failure is a real (if small) risk.

3. FX conversion spread

When you buy a US-listed stock (or any non-GBP asset), Trading 212 charges 0.15% on currency conversion. That is competitive with the cheaper end of UK brokers (Hargreaves Lansdown is around 1%, Interactive Investor around 1.5%). For buyers of GBP-priced UCITS ETFs, the FX cost is rarely encountered.

4. Interest spread on uninvested cash

Trading 212 holds uninvested cash in money market funds and bank deposits. They pass on a portion of the interest (currently around 4-5% on GBP cash) and keep the rest as a spread of roughly 0.5-1.5 percentage points. This is a meaningful and growing revenue stream for all "free" brokers post-2022.

5. Trading 212 Plus subscription

A paid tier (£3.99/month in 2026) adding more daily order limits, additional pies, and a small interest boost. The free tier remains fully usable.

Trading 212 also earns small revenue from interchange fees on its debit card. They are not selling your personal data, trade history, or contact details.

What about payment for order flow?

Payment for Order Flow (PFOF) is where a broker routes customer orders to specific market makers in exchange for a kickback. It became famous through Robinhood in the US, where it underpins commission-free trading.

PFOF is effectively banned for UK retail brokers under MiFID II conflict-of-interest rules. Trading 212 has publicly stated they do not accept PFOF for UK retail customers, and the regulatory regime makes it implausible. The most common scam-adjacent suspicion for free brokers does not apply in this market.

The legitimate risks worth knowing

None of these are "scam" risks. They are genuine, disclosed product risks that any T212 user should understand:

- CFDs are dangerous. The 75-85% loss rate is not a marketing exaggeration. CFDs use leverage that magnifies losses, charge compounding overnight fees, and have a structural negative expected return for retail traders. If you only use Invest and ISA, this does not apply. The same maths plays out in retail prop trading "funded trader" challenges, which are a separate category of product worth understanding before paying any fee.

- Securities lending introduces counterparty risk above the £85,000 FSCS limit. For most retail investors with portfolios under £85k, this is irrelevant.

- The 0.15% FX conversion fee on USD purchases is small but real. For frequent US-stock buyers, it adds up. Buying London-listed UCITS ETFs (CSPX, VUAG, VWRP) avoids this entirely.

- The platform can have outages. Trading 212 has had occasional outages during major market volatility (notably during GameStop in early 2021). All brokers do. T212's incidence is roughly in line with peers.

- Customer service is chat-based. No phone support. Escalations can take longer than at a traditional broker.

- AutoInvest pies are not legal entities. They are a UI convenience for batched orders. Not a wrapper, not a fund.

Common complaints and what they actually mean

UK forums and Trustpilot surface a few recurring complaints:

- "They froze my account." Usually a KYC/AML check triggered by an unusual deposit. Standard at every UK broker. Provide the requested documents and accounts unfreeze within days.

- "Withdrawals took longer than expected." Withdrawals to UK bank accounts typically settle within 1-3 business days. International transfers can be slower.

- "I lost money on CFDs." The regulator-disclosed product risk. Not a scam.

- "They changed the interest rate." Interest paid on cash tracks the underlying rate environment. Normal cash management.

None of these patterns suggest fraud.

Who Trading 212 is and is not for

Trading 212 is a good fit for:

- UK residents wanting a Stocks and Shares ISA with no platform fee

- Beginners buying London-listed UCITS ETFs (S&P 500 trackers, FTSE All-World, etc.)

- People investing small monthly amounts who want fractional shares

- Anyone wanting interest on uninvested cash without moving it elsewhere

- Investors who want a clean mobile-first experience

Trading 212 is a worse fit for:

- Investors with portfolios well above £85,000 who want to spread custody risk across multiple brokers

- People who specifically want a SIPP - T212 launched a SIPP in 2024 but the established competitors (AJ Bell, Vanguard, Interactive Investor) still have deeper SIPP feature sets

- Active traders who want phone support during volatility

- Anyone who wants to use CFDs as a serious trading vehicle (don't)

For more on the platform comparison generally, see our piece on the best UK investment platform and the deeper dive on why Trading 212 is the best beginner platform. If you are weighing up the SIPP option specifically, our review of the Trading 212 SIPP as a low-cost pension goes into the detail.

Further Reading

Smarter Investing - Tim Hale - The standard UK reference on evidence-based investing, and a useful counterweight to broker FOMO: the platform matters less than what you actually hold inside it. (Affiliate link - we may earn a small commission at no extra cost to you.)

Read Next

- Why Trading 212 is the best beginner platform

- Trading 212 SIPP: a low-cost UK pension review

- The best UK investment platform

- FSCS protection: a UK investor's guide

- Stocks and Shares ISA: the UK guide

Frequently Asked Questions

Is Trading 212 safe in the UK?

Yes. Trading 212 UK Ltd is FCA-regulated (FRN 609146). Client cash sits in segregated bank accounts, securities are held in nominee custody, and Invest/ISA accounts are covered by FSCS up to £85,000 per person - the same protection regime as Hargreaves Lansdown and AJ Bell.

How does Trading 212 make money if it has no commissions?

CFD spreads (largest, but a separate product), securities lending, a 0.15% FX fee on non-GBP purchases, the interest spread on uninvested cash, and the optional Trading 212 Plus subscription. They do not sell personal data and do not accept payment for order flow under UK MiFID II rules.

Does Trading 212 use payment for order flow?

No. PFOF is effectively banned for UK retail brokers under MiFID II. Trading 212 has publicly confirmed it does not accept PFOF in this market.

Should I worry about securities lending on my Trading 212 ISA?

Probably not, if your portfolio is under the £85,000 FSCS limit. T212 ISA accounts have securities lending enabled by default with an opt-out. For larger portfolios, opting out or splitting custody across brokers reduces counterparty exposure.

Is Trading 212 better than Hargreaves Lansdown?

For most beginners and small-to-mid-size portfolios, yes, largely on cost. Trading 212 has no platform fee on its ISA versus HL's 0.45%, pays interest on uninvested cash, and charges 0.15% FX versus around 1% at HL. Hargreaves still wins on phone support, research tools, and SIPP feature depth.

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all