Financial Independence UK: The Maths Nobody Shows You

If I told you the newborn in your arms owed me £700k, you'd get angry. That's exactly what happened to you. You accepted it and pay it every day.

Cite this article

Freedom Isn't Free (2026) Financial Independence UK: The Maths Nobody Shows You. Available at: https://freedomisntfree.co.uk/articles/financial-independence-the-brutal-reality (Accessed: 5 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- You are born into a system where you owe a lot simply for existing, and this debt follows you throughout your life.

- The system makes it seem like you have choices when, in reality, you are trapped in a cycle of rent, taxes, and interest.

- To achieve true financial independence, you need to own your shelter and create a continuous income stream from your investments.

- Understanding these rules is key to breaking free from a life of financial exploitation.

Financial Independence in the UK: The Brutal Reality No One Talks About

If you've found your way here, chances are you already sense that something isn't quite right. Maybe it's the feeling that no matter how hard you work, you never seem to get ahead. Maybe it's the creeping realisation that your salary disappears before the month does, that the mortgage or rent feels like a life sentence, or that "retirement" is a distant fantasy rather than a plan.

You're not imagining it. There is a problem, and you're right to be looking for answers.

This article won't comfort you with platitudes. It will explain the problem in honest, unflinching terms: why the system you were born into is not designed for your freedom, and why that makes the pursuit of Financial Independence not just a smart financial strategy, but an act of quiet revolution. The rest of this site exists to give you the practical tools to act on that realisation: the investment strategies, the tax wrappers, the savings frameworks, and the mindset shifts that can accelerate your path to owning your own time.

Read on. Once you see it, you won't be able to unsee it.

You Start Life in Debt (The Zero-Point Myth)

We are raised on the myth of the "clean slate." We are told that at 18, we enter the world as free agents, ready to carve out a life. This is a lie.

In reality, you are born into a state of systemic deficit. You own no land. You own no shelter. You have no inherent right to the food produced by the earth around you. Because every square inch of the UK is owned by someone else, often held through dynastic legacies that stretch back to feudal times, and you are born in debt.

The anthropologist David Graeber spent 500 pages documenting exactly how deep this goes in Debt: The First 5,000 Years - tracing how debt has been used as a tool of social control from ancient civilisations to the modern financial system. The mechanisms change; the dynamic does not.

To simply exist on a piece of ground, you must pay. To eat, you must pay. To keep the government from seizing what little you have, you must pay taxes. On day one of your adulthood, you effectively carry a "ghost debt" equal to the cost of a home and the lifetime cost of sustenance.

The Illusion of Choice

The system is designed to mask this reality with the "Illusion of Choice." You aren't forced to take a mortgage; you "choose" to buy a home. You aren't forced to work 40 hours a week; you "choose" to pursue a career.

But when the alternative is homelessness and starvation, "choice" is a polite word for wage slavery.

Most of your productive years are spent in an exploitative spiral:

- Rent: You pay for the privilege of shelter, which directly enriches a landlord and builds their equity, not yours.

- Taxation: The state takes a cut of your labour before you even see it.

- Interest: When you finally "buy" a home, you pay the bank twice the home's value over 30 years in interest.

This isn't a "left-wing" manifesto. This is a cold, clinical assessment of the constraints you live under. You cannot win a game if you don't understand the rules, and the rules are currently written to keep you exchanging your limited time for the enrichment of others.

How Financial Independence Breaks the Cycle

To achieve Financial Independence (FIRE) is to opt out of this exploitation. It is a refusal to remain a digital serf. The goal is to move from exchanging time for survival to owning your time for fulfillment.

The two pillars of this revolution are:

- Ownership of Shelter: Eliminating the "subsistence fee" (rent/mortgage) so that your right to exist on the planet is no longer tied to a monthly bill.

- The Perpetual Income Stream: Owning assets (stocks, bonds, dividends) that produce value without requiring your physical presence.

How Long Does Financial Independence Take in the UK?

The transition from "wage slave" to "sovereign individual" is purely a function of one variable: your Savings Rate. This is the percentage of your take-home pay that you divert from the pockets of others (landlords, retailers, banks) into your own investment vehicles.

In the FIRE movement, we treat the Savings Rate as a speedometer. The higher the percentage, the faster you move toward the "Escape Velocity" where your investments generate more than you spend.

The following table assumes a starting point of £0, a target of £735,000 (covering an average UK home of £285k and a £450k investment pot to cover basic subsistence), and a 7% inflation-adjusted return from an S&P 500 index fund.

Calculations based on a standard UK take-home pay of approx. £2,300/month.

| Savings Rate | Monthly Invested | Years to £735k | The Reality |

|---|---|---|---|

| 10% | £230 | 44 Years | You retire at the "standard" age. The system wins. |

| 25% | £575 | 32 Years | You buy back a decade of your life. |

| 40% | £920 | 25 Years | You reach freedom while still young enough to enjoy it. |

| 50% | £1,150 | 22 Years | You have cut the "standard" working life in half. |

| 65% | £1,495 | 18 Years | Total autonomy in less than two decades. |

Plotted on a curve, the shape of the prison break is unmistakable: every extra percentage point of savings rate carves more time off the sentence than the last.

Years to escape velocity (£735k target) by savings rate

Source: UK take-home pay of approx. £2,300/month, 7% real return, £0 start, £735k target

Why the FIRE Movement Exists

These calculations aren't just dry math; they are the blueprints for your prison break.

The financial independence movement exists because once you see these numbers, you cannot unsee the bars of the cage. Understanding that every £100 you "save" is actually a brick in the wall of your future home, or a day of freedom purchased back from a corporation, changes your relationship with reality.

This site is designed to be your toolkit for hacking these timelines. We aren't here to talk about "budgeting" in a restrictive, moralistic sense. We are here to provide the tips, tricks, and tools to help you fast-track the process:

- Slash the Subsistence Fee: Finding unconventional ways to lower housing and tax costs to increase that savings rate.

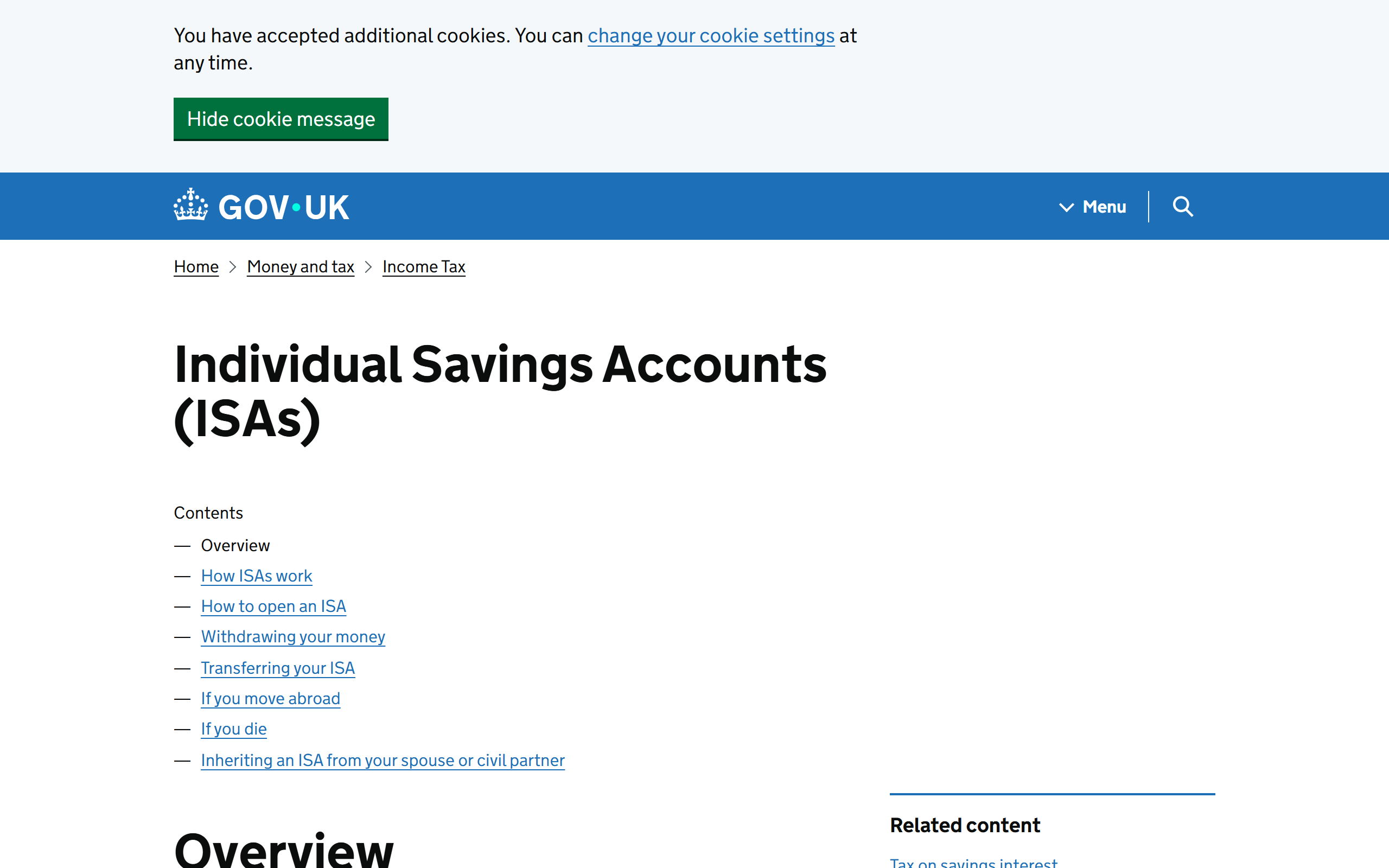

- Optimise the Vehicle: Understanding why the S&P 500 is a primary engine for wealth and how to shield it from the government's share (using ISAs and SIPPs).

- Increase the Input: Strategies to raise your income without increasing your "lifestyle creep."

- De-Program the Consumer: Breaking the psychological chains that tell you that buying "things" is a substitute for owning your "time."

What Real Wealth Actually Looks Like

By fast-tracking this process, you stop being a cog in the machine and start becoming the architect of your own existence.

Once you have cleared the "Great Debt of Birth," you are finally free to define Wealth. In the capitalist game, wealth is just a number on a screen. In the game of Life, wealth is the ability to spend your time on artistic pursuits, community building, or rest, not because it produces "value" for a shareholder, but because it fulfills you.

You were born into a system designed to use you. Financial Independence is how you use the system to find yourself.

Your Next Step: Calculate Your FIRE Number

Now that you understand why financial independence matters, the most important thing you can do next is make it concrete. Abstract ideas don't change lives. Numbers do.

Your FIRE number is the specific amount of money you need invested before your portfolio generates enough passive income to cover your living expenses indefinitely, without ever needing to work again. It is your personal escape velocity. It turns "I want to be free someday" into "I need £X, and I am £Y of the way there."

The most widely used rule of thumb is the 25x rule: take your estimated annual spending and multiply it by 25. That figure, invested in a diversified portfolio, should, based on historical data, sustain indefinite withdrawals at 4% without running out.

Annual spending of £25,000 → FIRE number of £625,000. Annual spending of £40,000 → FIRE number of £1,000,000.

Start thinking about what your number is. What does your life actually cost today? What would it cost if you weren't commuting, eating lunch out, or buying clothes for the office? That number is probably lower than you think, and that gap between what you imagine and what you actually need is where your freedom lives.

Everything else on this site is built to help you close that gap.

Ready to find your number? Read our next article: The Ransom Price: Calculating Your Financial Independence Number

Frequently Asked Questions

What is the "Great Debt of Birth"?

The concept describes the structural deficit every person is born into - no land, no shelter, no inherent access to food. Because everything essential to survival has a price, you are effectively born owing a lifetime of payments before you have earned a penny.

Is Financial Independence only achievable on a high income?

No. The key variable is not income - it is savings rate. Someone earning £35,000 and saving 50% reaches financial independence faster than someone earning £80,000 and saving 10%. Income accelerates the timeline but does not determine it.

What is the 25x rule?

The 25x rule states that you need roughly 25 times your annual expenses invested in a diversified portfolio to be financially independent. This derives from the 4% rule, which suggests a 4% annual withdrawal rate has historically sustained portfolios indefinitely. For example, annual spending of £30,000 implies a target of £750,000.

How long does Financial Independence take?

It depends almost entirely on your savings rate. At 10%, the typical timeline is 40-plus years. At 50%, it falls to around 17 years. At 65%, closer to 10. The table in this article illustrates these timelines using UK median income assumptions.

Where do I start on the path to Financial Independence?

Start by calculating your current annual spending - that is your baseline. Then multiply it by 25 to find your target number. Next, identify your savings rate and begin directing surplus into tax-efficient accounts (ISA and pension). The FIRE number calculator on this site will walk you through the maths.

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all