Find Lost Pensions UK: A Step-by-Step Tracing Guide

31 billion pounds sits in lost UK pensions and most owners have no idea any of it is theirs. Auto-enrolment since 2012 created a pot at every job. The free tool to find them.

Cite this article

Freedom Isn't Free (2026) Find Lost Pensions UK: A Step-by-Step Tracing Guide. Available at: https://freedomisntfree.co.uk/articles/find-lost-pensions-uk (Accessed: 25 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- The Pensions Policy Institute estimates around 31 billion pounds sits in lost UK pension pots. Most people lose track because they moved house, changed name, or had an old employer get bought out or rebranded.

- The Pension Tracing Service is free and run by the DWP. You search by an old employer name (or by pension provider for personal pensions and SIPPs) and it returns the contact details of the scheme administrator.

- Tracing is only step one. You then need to write to the administrator with your details (full name, dates of employment, National Insurance number, dates of birth) to actually claim the pot.

- Be cautious about consolidating. Defined benefit pensions often come with guaranteed income or guaranteed annuity rates that you would lose by transferring. Anything over 30,000 pounds in a DB scheme legally requires regulated advice before transfer.

- The Pensions Dashboards Programme is meant to consolidate every pension into one online view, but as of April 2026 it is still in phased rollout and not yet fully available to the public.

Find Lost Pensions UK: A Step-by-Step Tracing Guide

If you want to find lost pensions in the UK, the answer is the free government-run Pension Tracing Service - and you probably have more pots out there than you think. Auto-enrolment came in back in 2012, which means almost every job you have held since has likely created a small pension pot somewhere. Add in any older workplace schemes, a personal pension you opened in your twenties and forgot about, and a SIPP you set up during lockdown, and the count adds up.

The Pensions Policy Institute reckons around 31 billion pounds is currently sitting in lost UK pension pots. That is not a typo. Millions of pots, owned by people who have no idea they exist or no clue how to find them. If you have changed jobs more than twice or moved house since starting work, some of that money is probably yours.

Here is how to find it, what to do when you do, and what to watch out for.

Contents

- Why So Many UK Pensions Get Lost

- The Pension Tracing Service (Free, Government-Run)

- What Information You'll Need

- What Happens When You Find a Lost Pension

- Should You Consolidate Found Pensions?

- The Pension Dashboard: Coming Soon

- Avoiding Future Lost Pensions

- Frequently Asked Questions

Why So Many UK Pensions Get Lost

Pensions get lost for boring, predictable reasons:

- House moves. You change address, the pension provider keeps writing to the old one, eventually the post stops and the pot drifts off the radar.

- Name changes. Marriage, divorce, deed poll. Providers struggle to match old records to a new name.

- Employer changes. Your old company gets bought, renamed, sold off, or goes bust. The pension scheme often gets transferred to a different administrator and the trail goes cold.

- Auto-enrolment churn. Since 2012 most jobs auto-enrol you into a workplace pension. Stay in a role for six months, leave, and you have a small pot you may never have actively engaged with.

- Provider mergers. Insurance companies and pension administrators consolidate. Your old "Equitable Life" pension might now be administered by someone with a completely different name.

If any of those apply to you (and for most people, several do), there is a decent chance you have at least one lost pension. The good news is the search is free.

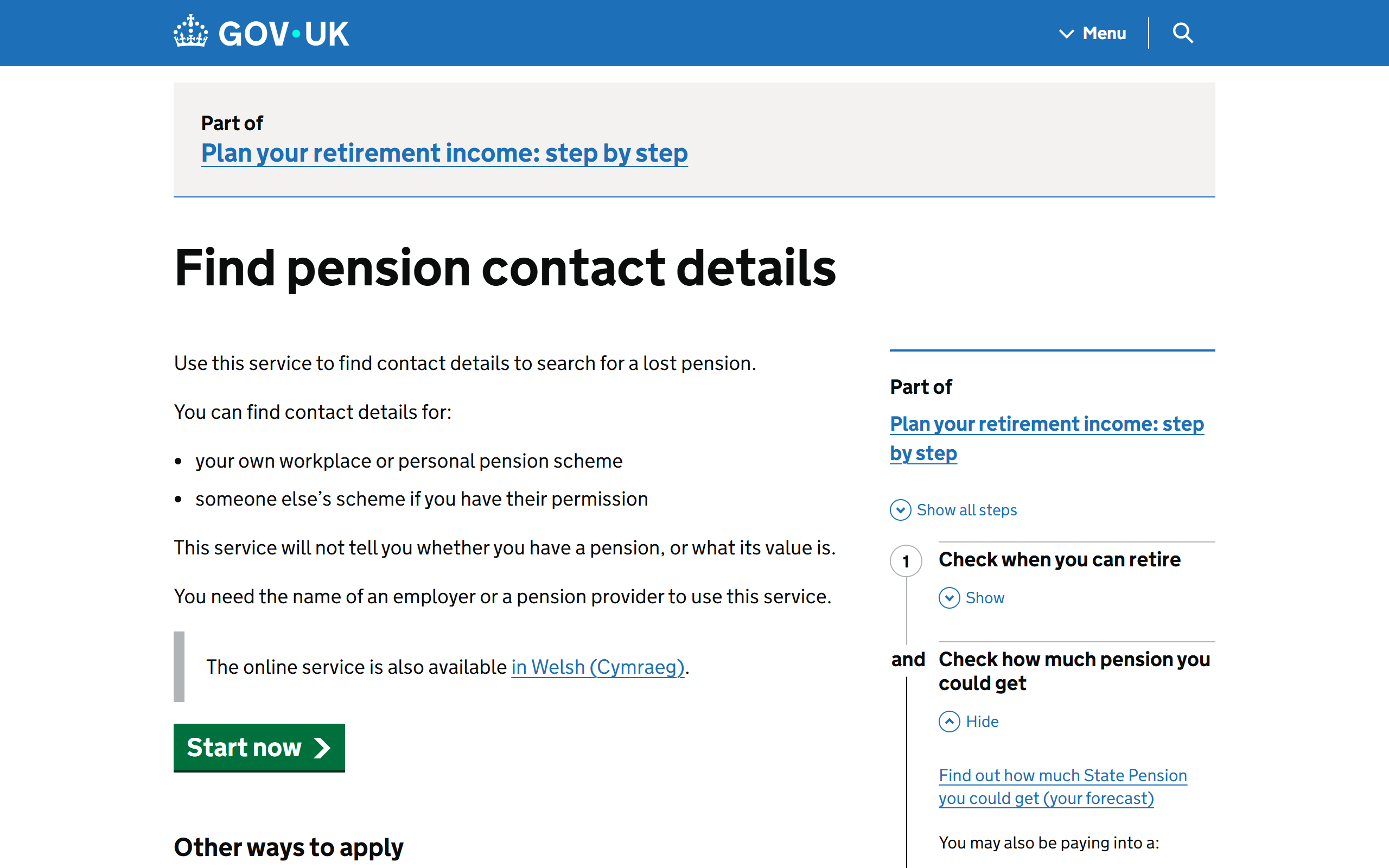

The Pension Tracing Service (Free, Government-Run)

The Pension Tracing Service is run by the Department for Work and Pensions. It is free, public, and the only official tracing tool you should be using.

You go to gov.uk, type in either:

- The name of a former employer (for workplace pensions), or

- The name of a pension provider (for personal pensions and SIPPs)

The service then returns the current contact details of the scheme administrator. That is it. It will not tell you whether you have a pension with that scheme, how much is in it, or what type of pension it is. It just gives you the address and phone number of the people who would know.

That last point trips a lot of people up. The Tracing Service is a directory, not a database of your money. Step one is finding the administrator. Step two is contacting them.

Be wary of any other "pension finder" service that charges a fee or asks for your bank details. Several private firms exist that essentially do the same lookup the government does for free, then charge you a percentage of any pot you recover. You do not need them.

What Information You'll Need

Before you start tracing, gather as much of the following as you can:

- Full name (and any previous names). Maiden name, married name, any deed poll changes.

- Date of birth.

- National Insurance number. This is the single most important piece of information. It links you to every employer record HMRC has.

- Employer name and dates of employment. Approximate dates are fine. "I worked at Tesco from around 2014 to 2017" is enough to start.

- Old addresses. The address you lived at while working there helps the administrator match records.

- Any old paperwork. Annual statements, joining letters, scheme booklets. Even a partial reference number speeds things up enormously.

You will not need all of this for the Tracing Service itself, which only asks for the employer or provider name. But you will need it when you contact the administrator to claim the pot.

MoneyHelper has a useful checklist if you want a printable version.

What Happens When You Find a Lost Pension

Once the administrator confirms you have a pot, they will send you a statement. Read it carefully and look for these things:

- Pension type. Defined benefit (DB, also known as final salary) or defined contribution (DC). This matters enormously, see the next section.

- Current value. For a DC pot this is a pound figure. For a DB pension it will usually be expressed as an annual income at retirement.

- Charges. The annual management charge (AMC) and any other fees. Older pensions sometimes have eye-watering fees of 1% or more, which a modern SIPP would beat by a wide margin.

- Guaranteed annuity rate (GAR). Some old personal pensions from the 1980s and 1990s come with a GAR built in, often 8% to 11%. That is a guaranteed income rate that no modern annuity will match. Do not transfer these without serious thought.

- Death benefits and protected tax-free cash. Some older pensions come with enhanced lump sum entitlements above the standard 25%.

If you are reading a pension statement for the first time and feeling baffled, our UK pensions explained guide covers the basics in plain English.

£50,000 pot over 20 years - what each legacy fee tier costs you

Same starting pot, same 7% gross return, four AMC tiers commonly found in old workplace and personal pensions.

Source: Compound at 7% gross minus AMC, single lump sum, no further contributions.

Should You Consolidate Found Pensions?

The instinct is usually to roll everything into one pot, ideally a low-cost SIPP. That is often sensible for small DC pots languishing in expensive legacy schemes, but not always.

Consolidation can make sense when:

- You have several small DC pots with high charges (1% AMC or more).

- You want a single online view and one set of investment choices.

- Your current SIPP or workplace pension has lower fees and better fund options.

Be very careful about transferring when:

- It is a defined benefit pension. You are giving up guaranteed income for life, often with inflation protection. The transfer value usually looks generous, but the income it can buy in a DC pot is rarely worth it. Anything above 30,000 pounds legally requires advice from an FCA-regulated adviser with the relevant DB transfer permission.

- The pension has a guaranteed annuity rate or guaranteed minimum pension (GMP). These are often worth more than the headline transfer value.

- There are protected benefits, like protected tax-free cash above 25%, or a protected pension age below 55.

If consolidation does make sense, our guides on SIPP vs workplace pension and the Trading 212 SIPP cover the low-cost options worth considering.

The Pension Dashboard: Coming Soon

The Pensions Dashboards Programme is the government's plan to fix the lost-pension problem at source. The idea is simple: log in once, see every pension you have ever paid into, including the State Pension, in one place.

It has been "coming soon" for years now. As of April 2026 the programme is in phased rollout, with pension providers being onboarded in stages. A public-facing dashboard is not yet fully live for individual savers. The connection deadline for providers is October 2026, with public access expected to follow.

When it does launch, it will not replace the Tracing Service overnight, but it should make tracing far easier for anyone who has stayed within the UK pensions system.

Avoiding Future Lost Pensions

Once you have hunted down what is yours, build habits to stop the same thing happening again:

- Update your address with every provider whenever you move. Treat it like updating your driving licence. Five minutes per provider.

- Keep a single document listing every pension. Provider, scheme name, reference number, value at last statement. A spreadsheet is fine.

- Consolidate small pots when it makes sense. Fewer providers means fewer addresses to update.

- Take the annual statement seriously. Skim it when it arrives. If it stops arriving, that is your cue to chase.

- Use a permanent email address. Work emails get cut off. Personal Gmail or a custom domain lasts decades.

Watch out for pension scams while you are tracing. The FCA's ScamSmart service lets you check whether a firm contacting you is legitimate. Cold calls about pensions have been illegal in the UK since 2019, so anyone phoning you out of the blue offering a "free pension review" or a transfer to a higher-yielding scheme is a scammer, full stop. Hang up.

Frequently Asked Questions

How long does it take to find a lost pension in the UK?

The Pension Tracing Service usually returns administrator contact details within a few minutes online. Actually claiming the pot, however, can take anywhere from two weeks to several months depending on how good the administrator's records are and whether your name or address has changed since you last paid in.

Is the Pension Tracing Service really free?

Yes, it is run by the Department for Work and Pensions and there is no charge to use it. If anyone asks you to pay to find a UK pension, they are reselling free public information at best, or running a scam at worst.

What if my old employer has gone bust?

The pension scheme is held separately from the employer's own finances, so a bankruptcy does not normally wipe out your pot. The scheme will have been transferred to a new administrator or, for defined benefit schemes, possibly to the Pension Protection Fund. The Tracing Service should still find a contact for you.

Can I find a lost pension without my National Insurance number?

You can start the search without it, but you will struggle to claim. The administrator needs the NI number to match you to their records. If you have lost yours, you can request it back from HMRC via your Personal Tax Account on gov.uk.

Should I use a paid pension finder service?

No. They use the same free government tools you can use yourself, then charge a percentage of any pot they recover. Doing it directly takes an hour of your time and costs nothing.

What does Martin Lewis say about combining pensions?

Martin Lewis's MoneySavingExpert has a dedicated guide on whether to combine pensions, and its line is the same one this article takes: consolidating defined-contribution pots under one roof can cut fees and admin, but you should not blindly merge everything. MSE warns against transferring any pot that carries valuable safeguarded benefits (guaranteed annuity rates or a defined-benefit promise), notes that "partial consolidation" - moving some pots and leaving others - is often the right answer, and flags that a defined-benefit pension worth 30,000 pounds or more legally requires regulated advice before transfer. It also points readers to the free MoneyHelper and Pension Wise guidance. Check the current MoneySavingExpert guide before you act on any pot you are unsure about.

Read Next

- UK Pensions Explained - the basics of how pensions work in the UK, written for first-time readers.

- SIPP vs Workplace Pension - which one to consolidate into if you decide to combine pots.

- Trading 212 SIPP: Low-Cost Pension - one of the cheapest UK SIPPs for consolidation.

- Beyond the 4% Rule: A UK Retirement Guide - what to do once your pots are in one place.

- FI Number Calculator - work out the size of pension and ISA pot you need.

Further Reading:

Smarter Investing - Tim Hale - The standard UK reference for low-cost, evidence-based investing. Useful background for deciding how to invest a found pension once you have consolidated. (Affiliate link - we may earn a small commission at no extra cost to you.)

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all