The Hidden Costs of Early Retirement in the UK

The morning you hand in your notice, three things disappear that no FIRE spreadsheet ever modelled. Each one quietly compounds for twenty years. By 60 the gap is not small.

Cite this article

Freedom Isn't Free (2026) The Hidden Costs of Early Retirement in the UK. Available at: https://freedomisntfree.co.uk/articles/hidden-costs-of-early-retirement-uk (Accessed: 25 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Retiring early means decades without employer pension contributions, which can leave a significant gap at State Pension age

- National Insurance gaps from not working can reduce your State Pension entitlement

- You will spend more in early retirement than you think - boredom, hobbies, and lifestyle inflation are real

- Private healthcare, dental, and life insurance costs often catch early retirees off guard

Hidden annual costs of early retirement (typical UK figures)

Most FIRE spreadsheets miss these. £8k-£12k a year the calculators never show you.

The Hidden Costs of Early Retirement in the UK

The hidden costs of early retirement in the UK catch people off guard every single year. You have spent years building your pot, tracking your savings rate, and watching the numbers climb. Then you pull the trigger and discover that the spreadsheet lied to you. Not because the maths was wrong, but because it left things out.

Everyone talks about how much you need to retire early. Almost nobody talks about what it actually costs once you get there. The gap between "I have enough" and "this is sustainable for 40 years" is where most early retirement plans quietly fall apart.

This article covers the expenses that most FIRE planners underestimate, ignore, or simply do not know about until they are staring at them.

Contents

- The Pension Gap: Lost Employer Contributions

- National Insurance and Your State Pension Shortfall

- The Bridging Problem: 57 Is Not When You Think

- Lifestyle Inflation and Boredom Spending

- Healthcare, Dental, and Insurance

- The Workplace Benefits You Forgot You Had

- Inflation Over a 40-Year Retirement

- Sequence of Returns Risk in the Early Years

- The Psychological Cost

- Frequently Asked Questions

The Pension Gap: Lost Employer Contributions

When you leave employment, your employer stops paying into your pension. Obvious, right? But most people drastically underestimate how much this costs them over time.

Under auto-enrolment, the minimum employer contribution is 3% of qualifying earnings. Many employers pay 5% or more. If you earn £50,000 and your employer contributes 5%, that is £2,500 per year going into your pension that you are now forfeiting.

Retire at 35 and you lose that contribution for 22 years before you can even touch your pension (from age 57 in 2028). At a conservative 5% annual growth rate, those lost employer contributions alone could be worth over £90,000 by the time you reach pension access age.

This is money that was effectively part of your compensation package. The moment you hand in your notice, it vanishes. Your FI number needs to account for this gap, and most calculators do not.

National Insurance and Your State Pension Shortfall

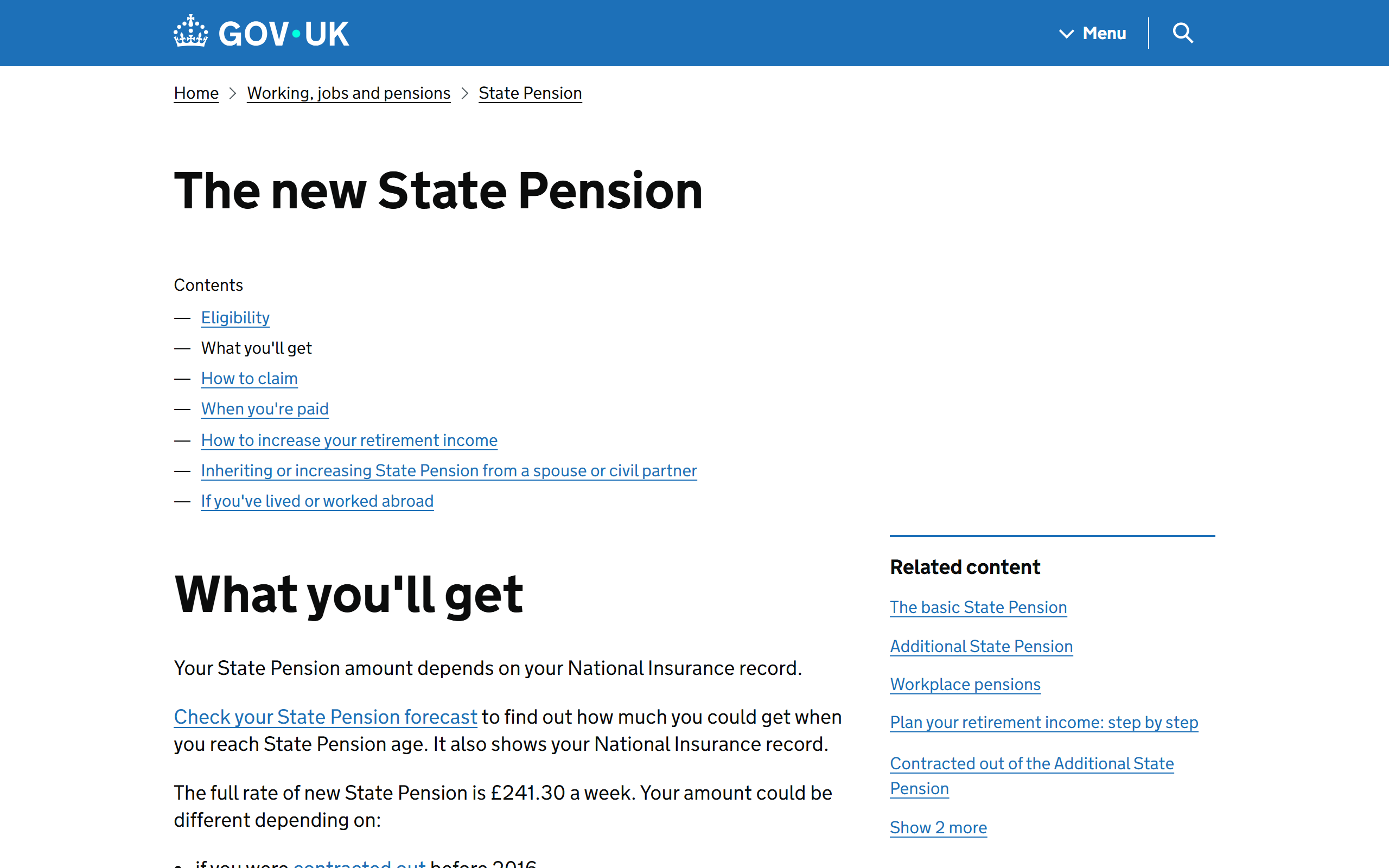

You need 35 qualifying years of National Insurance contributions to receive the full new State Pension, which is around £230 per week in 2026/27. Each missing year reduces your entitlement by roughly 1/35th of the full amount.

If you retire at 40 and started working at 22, you have 18 qualifying years. That leaves you 17 years short of a full State Pension. At current rates, each missing year costs you around £329 per year in retirement income - for the rest of your life after State Pension age.

You can fill gaps with voluntary Class 3 National Insurance contributions, currently around £17.45 per week (£907 per year). That is a good deal - you pay £907 once and gain roughly £329 per year for life in return. But you need to be aware of the deadlines and eligibility rules. HMRC has specific windows for filling historical gaps, and missing them means those years are gone permanently.

The trap here is not knowing about it until it is too late. Check your NI record on the government website now, while you still have time to act.

The Bridging Problem: 57 Is Not When You Think

From 2028, the minimum pension access age rises to 57 (up from 55). If you retire at 40, that is 17 years where your pension pot is locked away and untouchable. Every penny of living expenses during that period needs to come from ISAs, general investment accounts, or cash.

This is the bridging problem, and it is the single biggest structural challenge for UK early retirees. Your ISA and GIA need to cover all expenses from your retirement date until you can access your SIPP.

The maths is straightforward but uncomfortable. If you spend £30,000 per year and retire at 40, you need £510,000 in accessible (non-pension) assets just to bridge the gap to 57. That is before you even think about what happens after pension access.

Capital gains tax on GIA withdrawals adds another layer of friction. You are selling investments to fund your life, and every sale above your annual CGT allowance (currently £3,000) is taxable. Structure this badly and you hand a meaningful chunk back to HMRC each year.

Lifestyle Inflation and Boredom Spending

Here is the one nobody wants to admit: you will spend more in early retirement than you spend while working.

When you work full time, your weekdays are largely occupied. You eat lunch at your desk. Your commute, while expensive, fills time. Your evenings are recovery time - you are too tired to do much. Your spending is constrained by your schedule.

Remove the job, and you have 40 to 50 extra free hours per week. Those hours do not fill themselves for free. You take up hobbies. You eat out more. You renovate the house because you have been staring at the kitchen for three weeks straight. You travel, because why not - you have the time. You buy equipment for interests you never had time to explore before.

The FIRE community calls this "boredom spending," and it is real. Research consistently shows that discretionary spending increases in the first few years of retirement. You budgeted for £25,000 per year but find yourself spending £32,000 because life is happening at full speed for the first time.

Council Tax does not care that you are retired early. You still owe £1,500 to £2,500 per year depending on where you live, and there is no working-age discount for early retirees who happen to have savings.

Budget for this properly. Add 15-20% to your projected annual spending for the first five years. If you come in under, great. If you do not, you will be glad you planned for it.

Healthcare, Dental, and Insurance

The NHS is free at the point of use, and that is genuinely one of the UK's biggest advantages for early retirees. But "free" has limits.

Dental care is the most immediate problem. NHS dental places are vanishingly rare in many parts of the country. If you cannot find an NHS dentist, private dental care runs £30 to £60 for a check-up, £50 to £150 for fillings, and significantly more for anything complex. A dental plan from a provider like Denplan costs £15 to £30 per month, which is manageable - but it is an expense that your employer may have been subsidising.

Private health insurance becomes more attractive when you no longer have an employer scheme. Wait times for NHS treatment have been rising, and if you want prompt access to consultants and diagnostics, you are looking at £1,000 to £3,000 per year depending on your age, location, and level of cover. That cost increases every year as you get older.

Optical care is another one that slips through. Once you are over 40, regular eye tests and potential prescription changes become a recurring expense.

None of these will bankrupt you individually. But stack dental, optical, health insurance, and the occasional private consultation together and you are looking at £2,000 to £5,000 per year that was not on your original spreadsheet.

The Workplace Benefits You Forgot You Had

Your employer provides more than a salary. When you leave, you lose:

- Life insurance - most employers provide 2x to 4x salary as death-in-service benefit. Replacing this privately costs £20 to £60 per month depending on your age and coverage level.

- Income protection - if you cannot work due to illness, employer schemes pay a percentage of salary. Once you are retired, this is irrelevant in theory, but if your partner still works and depends on your portfolio income, the risk remains.

- Professional subscriptions - many employers cover professional body memberships, software licences, and training costs.

- Gym memberships and wellness benefits - corporate gym discounts, cycle-to-work schemes, and employee assistance programmes all disappear.

- Technology - your work laptop, phone, and home office equipment were provided or subsidised. Replacing and maintaining your own tech is a recurring cost.

Individually, these are small. Collectively, they can add £1,500 to £3,000 per year to your outgoings that you never noticed while employed because they were invisible.

Inflation Over a 40-Year Retirement

Inflation is the silent destroyer of early retirement plans, and most people do not grasp how hard it compounds over decades.

At 4% average inflation, £30,000 per year in today's money becomes roughly £66,000 in 20 years. In 40 years, it becomes £144,000. Your spending power halves roughly every 18 years.

A traditional retiree at 67 might need their money to last 20 to 25 years. An early retiree at 40 needs it to last 45 to 50 years. The difference is not linear - it is exponential. Every additional decade of retirement amplifies the damage that inflation does to your purchasing power.

This means your portfolio does not just need to sustain withdrawals. It needs to grow, in real terms, for decades. A portfolio that barely covers your expenses at age 40 will be underwater by 60 unless it has consistently beaten inflation after withdrawals.

The UK has experienced periods of sustained high inflation - the 1970s, the post-COVID spike - and there is no guarantee those episodes will not repeat during a 40-year retirement. Building in a margin of safety is not pessimism. It is realism.

Sequence of Returns Risk in the Early Years

The order in which investment returns arrive matters enormously when you are withdrawing money. Two portfolios can have identical average returns over 30 years, but if one experiences poor returns in the first five years while the retiree is drawing down, it may never recover.

This is sequence of returns risk, and it is the specific danger of the early retirement years. A 30% market crash in your first year of retirement hits differently when you are selling shares to cover living costs versus when you are still buying.

The standard mitigation is to hold 2 to 3 years of expenses in cash or near-cash (premium bonds, money market funds) so you never have to sell equities during a downturn. That cash buffer is dead money in terms of returns, but it buys you time - and time is the one thing that lets a portfolio recover.

Factor this buffer into your number. If you spend £30,000 per year, that is £60,000 to £90,000 sitting in low-return holdings purely as insurance. Your effective FI number just got bigger.

The Psychological Cost

This is the hidden cost that no spreadsheet captures, but it may be the most expensive of all.

Your job gave you more than money. It gave you structure, identity, social connection, and a daily sense of purpose. Remove it, and you are left with a void that no amount of portfolio growth can fill.

The connection between burnout and FIRE is well documented. Many people race toward early retirement to escape something, only to find that retirement does not fix the underlying problem. Worse, the absence of structure can amplify it.

Identity loss is real. When someone asks "what do you do?" at a dinner party, "I'm retired at 38" is a conversation stopper, not a conversation starter. Many early retirees report feelings of isolation, purposelessness, and even guilt - particularly if their partner or friends are still working.

Building a post-work identity takes time, effort, and often money (courses, hobbies, volunteering, projects). If you have not thought about what you are retiring to, you may find that the psychological cost far outweighs the financial savings.

Frequently Asked Questions

How much should I budget for hidden costs of early retirement in the UK?

A reasonable estimate is £3,000 to £8,000 per year on top of your base living expenses, depending on your circumstances. This covers voluntary NI contributions, private healthcare and dental, replacement of lost workplace benefits, and the inevitable lifestyle inflation that comes with unlimited free time. The exact figure depends on your health, location, and how active your retirement lifestyle turns out to be.

Can I get the full State Pension if I retire early?

Yes, but only if you have 35 qualifying years of National Insurance contributions by State Pension age. If you retire early and stop making NI contributions, you may fall short. Check your NI record on the government website and consider making voluntary Class 3 contributions (around £907 per year) to fill any gaps. This is one of the best financial returns available - you pay once and receive increased pension income for life.

What is the biggest financial risk of retiring early in the UK?

Running out of money due to a combination of lifestyle inflation, poor sequence of returns in the early years, and underestimating how long your money needs to last. A 40-year retirement is fundamentally different from a 20-year one. Inflation compounds relentlessly, spending tends to be higher than planned, and a major market crash in your first few years can permanently damage your portfolio. The safe withdrawal rate for UK retirees is closer to 3-3.5%, not the 4% often quoted from US data.

How do I bridge the gap between early retirement and pension access at 57?

You need sufficient funds in accessible accounts - ISAs and general investment accounts - to cover all living expenses from your retirement date until you can access your SIPP at 57 (from 2028). Our bridging guide covers this in detail. The key is to structure your withdrawals tax-efficiently, using your annual ISA allowance, CGT allowance, and personal allowance to minimise the tax drag on your drawdown.

Is early retirement in the UK actually worth it?

Yes - if you go in with your eyes open. The point of this article is not to discourage early retirement. It is to make sure you plan for what it actually costs, not what you hope it costs. The people who succeed at early retirement are the ones who budget realistically, build in a margin of safety, and spend time thinking about what they are retiring to - not just what they are retiring from. Financial independence is one of the most powerful things you can build. Just make sure the plan is complete.

Further Reading:

Die With Zero - Bill Perkins - A provocative take on retirement planning that challenges you to think about what you are retiring to, not just the numbers that get you there. (Affiliate link - we may earn a small commission at no extra cost to you.)

Quit Like a Millionaire - Kristy Shen - Practical FIRE strategies from someone who actually did it, including honest discussion of the costs and trade-offs most bloggers skip. (Affiliate link - we may earn a small commission at no extra cost to you.)

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all