UK Mortgage Types 2026: Every Scheme Explained

80% of UK borrowers walk out with a 25-year fix. The other 20% know about a dozen schemes the broker rarely volunteers, including a 100% LTV one that still exists in 2026.

Cite this article

Freedom Isn't Free (2026) UK Mortgage Types 2026: Every Scheme Explained. Available at: https://freedomisntfree.co.uk/articles/uk-mortgage-types-2026 (Accessed: 25 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- Most UK mortgages are capital-and-interest (repayment) on a fixed-rate deal of 2, 3, 5, or 10 years - that combination is the default for around 80% of borrowers.

- First-time buyer schemes in 2026 include the Mortgage Guarantee Scheme (95% LTV), First Homes (30% discount), Shared Ownership, the LISA bonus, and a few 100% LTV products like Skipton Track Record.

- Family-assisted options (Joint Borrower Sole Proprietor, guarantor, deposit-free with parental security) let buyers borrow more than their income alone allows without parents physically gifting cash.

- Specialist mortgages (buy-to-let, offset, self-build, bridging, retirement interest-only, lifetime mortgages) cover the edge cases that the mainstream market does not.

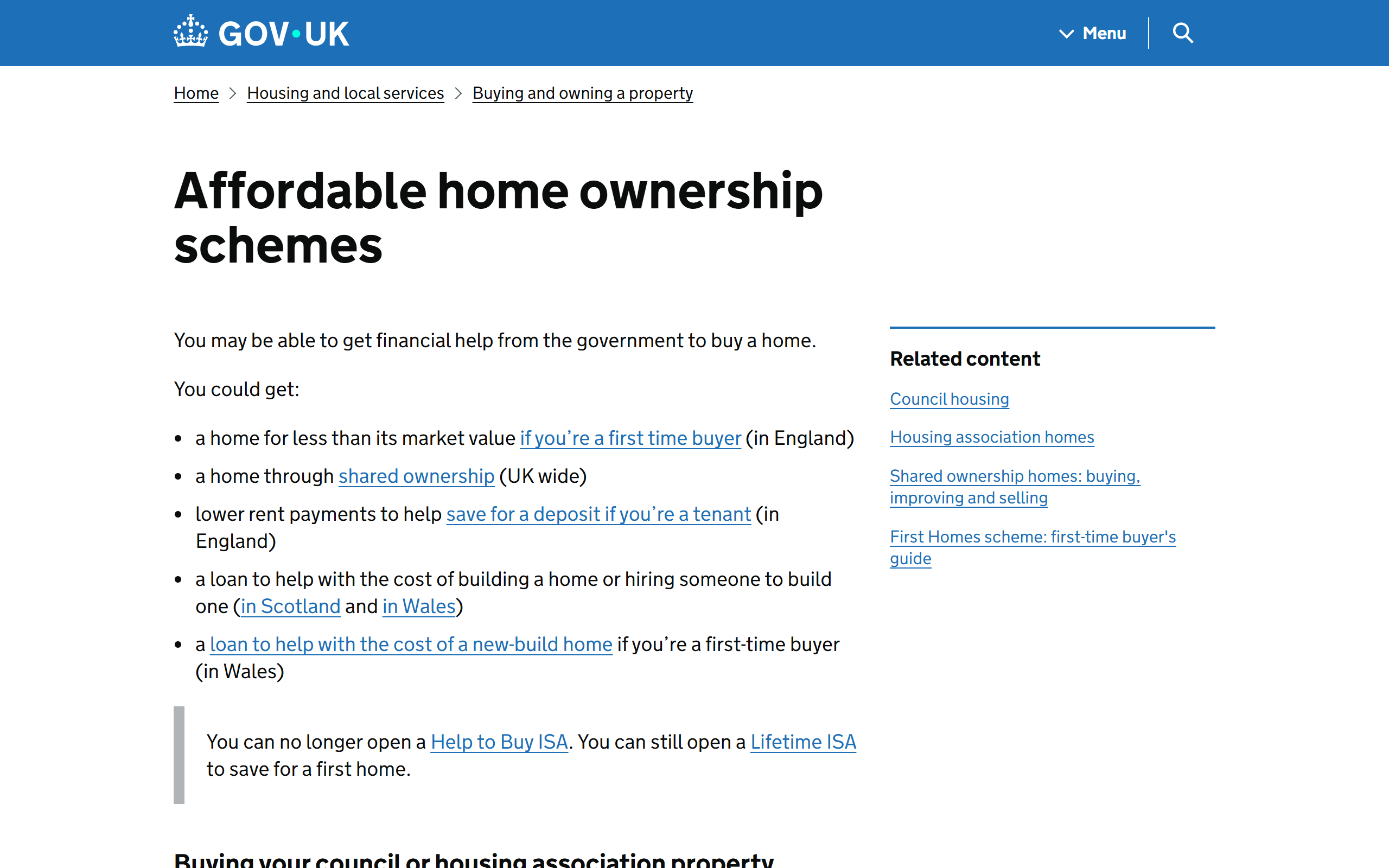

UK first-time buyer schemes in 2026

| Scheme | Min deposit | Best for | Key trade-off |

|---|---|---|---|

| Mortgage Guarantee Scheme | 5% | Small deposit, mainstream lenders | Higher rates than 75% LTV deals |

| First Homes (England) | Varies | Local FTBs in eligible new-builds | 30%+ discount stays with property |

| Shared Ownership | 5% of share | Buyers who cannot afford 100% | Rent and service charges on top |

| Lifetime ISA bonus | n/a (booster) | Under-40s buying under £450,000 | 25% penalty on non-qualifying use |

| Skipton Track Record (100%) | 0% | Long-term renters with payment history | No equity buffer, higher rate |

Help to Buy closed in 2023. These are the 2026 replacements.

UK Mortgage Types 2026: Every Scheme Explained

The UK mortgage market in 2026 has more variety than most buyers realise. The mainstream image is a 25-year repayment mortgage on a 5-year fix, and that is genuinely what most people end up with. But underneath that default sit dozens of other structures, each designed for a specific buyer or situation: first-time buyers without a deposit, parents helping children, self-employed contractors with patchy accounts, retirees releasing equity, landlords building portfolios, people self-building their own home.

This guide walks through every major UK mortgage type and scheme available in 2026. The aim is not to recommend a specific product but to give you a map of the options so you know what to ask your broker about. For the maths of what the mortgage actually costs, our mortgage overpayment calculator covers the repayment side in detail.

Contents

- Quick Comparison Table

- Repayment Structures

- Interest Rate Types

- First-Time Buyer Schemes

- Family-Assisted Mortgages

- Specialist Mortgages

- Mortgages for Older Borrowers

- Right to Buy and Forces Help to Buy

- Green Mortgages

- How to Choose Between All These Options

- Frequently Asked Questions

Quick Comparison Table

If you only have 30 seconds, scan this table to find the products worth reading about in detail below.

Rate types

| Rate type | How it moves | Typical use case | Watch out for |

|---|---|---|---|

| Fixed-rate (2/3/5/10yr) | Locked for the deal period | The default, around 80% of UK mortgages | Early repayment charges if you exit early |

| Tracker | BoE base rate + fixed margin | Useful when rates are expected to fall | Monthly payment moves with the base rate |

| SVR | Lender's choice, loosely tied to base rate | Almost never the right answer | Always more expensive than a fix or tracker |

| Discount variable | Lender's SVR minus a discount | Niche, rarely the cheapest option | Lender controls when the rate moves |

| Capped rate | Variable up to a fixed ceiling | Rare, expensive optionality | Pricing reflects the cap value |

First-time buyer schemes

| Scheme | Min deposit | Best for | Key trade-off |

|---|---|---|---|

| Mortgage Guarantee Scheme | 5% | Buyers who can save a small deposit but not 10%+ | Higher rates than 75% LTV deals |

| First Homes (England) | Varies | Local first-time buyers in eligible new-builds | 30%+ discount stays with the property forever |

| Shared Ownership | 5% of share | Buyers who cannot afford 100% of the property | Rent + service charges layer on top of mortgage |

| Lifetime ISA bonus | n/a (deposit booster) | Under-40s buying under £450,000 | 25% penalty on non-qualifying withdrawals |

| Skipton Track Record (100%) | 0% | Long-term renters with proven payment history | No equity buffer, higher rate |

| Forces Help to Buy | 0% (boosts deposit) | Serving armed forces personnel | Capped at £25,000 or 50% of salary |

Family-assisted

| Type | Family role | Best for | Key trade-off |

|---|---|---|---|

| Joint Borrower Sole Proprietor | Income only | Boosting borrowing power without parents owning | Parents on the hook for missed payments |

| Guarantor mortgage | Pledges to cover defaults | Buyers with weak credit or low income | Family member's home or savings at risk |

| Family Springboard / 100% LTV | Deposit held in linked account | Buyers with no deposit but family savings | Family savings locked for 5+ years |

| Income Boost | Income added to affordability | Groups buying together | Co-ownership is hard to unwind |

Specialist and older-borrower mortgages

| Mortgage | Best for | Key trade-off |

|---|---|---|

| Buy-to-let | Property investors / landlords | Tax changes since 2017 hurt higher-rate landlords |

| Offset | Self-employed, high-cash savers | Slightly higher rate, savings tied to mortgage account |

| Self-build | People building their own home | Released in stages, complex, more expensive |

| Bridging | Auction buys, chain breaks | 8-15% rates, expensive arrangement fees |

| Holiday let | Short-term rental properties | Stricter stress tests, FHL tax rules changing |

| Retirement Interest-Only (RIO) | 55+ wanting to release equity, keep payments low | Capital never reduces, repaid on sale or death |

| Lifetime mortgage | 55+ wanting cash from home with no monthly payments | Compounding interest can balloon over 20+ years |

The repayment structure determines what each monthly payment actually covers. Three options exist.

Capital and Interest (Repayment)

The default and most common structure. Each monthly payment covers the interest on the outstanding balance plus a portion of the original capital. Over the term of the mortgage (typically 25-35 years) the balance reduces to zero and you own the property outright.

Most UK mortgages from 2026 are repayment mortgages on regulated owner-occupier terms. If you are a first-time buyer or moving home, this is what you almost certainly want.

Interest-Only

You pay only the interest each month; the capital balance never reduces. At the end of the term, you repay the entire original loan in one lump sum from a separate source - usually the sale of the property, an investment portfolio, or another asset.

In 2026, interest-only owner-occupier mortgages are rare and tightly regulated. Lenders require a credible repayment vehicle and tend to limit interest-only deals to high-income or high-equity borrowers. Where it shines: buy-to-let landlords, where the rent covers the interest and the property itself is the repayment vehicle.

Part and Part

A hybrid where part of the balance is on repayment and part is on interest-only. Less common but still offered by some lenders for borrowers who want lower monthly payments than full repayment but more capital reduction than full interest-only. Usually a niche product.

Interest Rate Types

The rate type determines how the interest charged on your balance changes over the deal period.

Fixed-Rate

The interest rate is locked for a fixed period - typically 2, 3, 5, or 10 years - regardless of what happens to the Bank of England base rate. At the end of the fix, the mortgage rolls onto the lender's Standard Variable Rate unless you remortgage.

Around 80% of new UK mortgages in 2026 are fixed-rate according to UK Finance lending data, and 5-year fixes are the single most popular product. Fixed deals are predictable, easy to budget around, and have been the default after the rate volatility of 2022-2024.

Standard Variable Rate (SVR)

The lender's "default" rate, charged once a fixed or tracker deal ends. SVRs are typically 2-4 percentage points above the base rate and almost always represent the worst value. The vast majority of customers should remortgage off SVR onto a new deal as soon as their fix expires.

Tracker

The interest rate is fixed at a margin above the Bank of England base rate. If the base rate is 4.5% and your tracker margin is 0.99%, you pay 5.49%. When the base rate moves, your rate moves automatically (sometimes immediately, sometimes with a one-month lag).

Trackers are useful when base rates are expected to fall. They tend to be cheaper than fixed rates in normal conditions because you are bearing the rate risk yourself. Many trackers come with no early repayment charges, making them flexible for borrowers who might want to overpay heavily or move soon.

Discount Variable

A discount off the lender's SVR for a set period. Cheaper than the SVR itself but still moves whenever the lender chooses to change their SVR (which is correlated to the base rate but not directly tied). Less popular than trackers because the link to the base rate is indirect.

Capped Rate

Rare in the UK in 2026. The rate is variable but cannot rise above a fixed cap. Provides upside if rates fall and protection if they spike. Pricing reflects that optionality, so they tend to be more expensive than a comparable tracker.

First-Time Buyer Schemes

The 2026 schemes for first-time buyers are different from those a decade ago. The Help to Buy Equity Loan closed to new applicants on 31 October 2022, with completions running until March 2023, and will not return. Several other options have replaced it.

Mortgage Guarantee Scheme (95% LTV)

The government guarantees a portion of mortgages with deposits as low as 5%, encouraging lenders to offer 95% LTV products. The scheme was extended and runs through at least 2027. Most major UK lenders participate, including Lloyds, Halifax, NatWest, HSBC, Barclays, and Santander.

Practical effect: you can buy a £300,000 home with a £15,000 deposit instead of a £30,000 deposit. The trade-off is that 95% LTV deals carry higher interest rates than 75% or 60% LTV products, so the monthly cost is meaningfully higher per pound borrowed.

First Homes

The First Homes scheme offers eligible first-time buyers a discount of at least 30% (sometimes up to 50%) on the market price of new-build homes in England. The discount stays with the property for future buyers, so resales must also be sold to qualifying first-time buyers at the same percentage discount.

Eligibility includes income caps (£80,000 outside London, £90,000 in London) and price caps after discount (£250,000 outside London, £420,000 in London). The supply is limited - First Homes are built into specific developments, not retrospectively applied to any new build - so availability varies by area.

Shared Ownership

You buy a percentage of a property (typically 25-75%) and pay rent on the rest to a housing association. Over time you can "staircase" by buying additional shares until you own 100%.

In 2026, the model includes the updated Shared Ownership rules introduced in 2021, which require a minimum 10-year repair-and-maintenance support period from the housing association on new-build leases and allow staircasing in 1% increments rather than the old 10% minimum. These changes addressed common complaints about the original scheme.

The honest assessment: Shared Ownership lets you on the ladder with a small deposit but layers on rent, service charges, and lease complications. Staircasing to 100% ownership is theoretically possible but rarely happens in practice because share prices rise with the property's market value. For some buyers it is the only realistic route to home ownership; for others it can be a trap that delays full ownership for decades.

Lifetime ISA Bonus

The Lifetime ISA gives a 25% government bonus on contributions up to £4,000 a year, capped at a £450,000 first-home property price. Two adults each maxing the LISA contribute £8,000 a year and receive £2,000 in bonus payments toward the deposit.

The £450,000 cap is the key constraint - if you are buying in London or the South East, many properties exceed it, and using LISA money on a property above the cap triggers a 25% withdrawal penalty. Our Lifetime ISA UK guide covers the rules in detail.

Skipton Track Record (100% LTV)

Skipton Building Society launched the Track Record mortgage in 2023 and it remains one of the few 100% LTV products available in 2026. Eligibility requires 12 months of consecutive on-time rent payments, ages 21+, and proof you can afford the new mortgage payments at a level not exceeding your current rent.

It is genuinely useful for renters who could afford a mortgage but cannot save a deposit because rent absorbs everything. The trade-off is the rate (higher than equivalent 90% or 95% deals) and the absence of any equity buffer. A 5-10% house price fall puts you in negative equity immediately.

A handful of other lenders (Barclays, Vernon Building Society) have launched competing 100% LTV products since, often with a family-deposit or rent-history requirement.

Family-Assisted Mortgages

A growing category that lets parents help without simply gifting a deposit. The mortgage industry calls this segment "Bank of Mum and Dad" and it is now estimated to fund around 40-50% of UK first-time buyer purchases.

Joint Borrower Sole Proprietor (JBSP)

Two or more people share the mortgage liability but only one owns the property. Most often used when parents add their income to a child's mortgage application to boost borrowing capacity. The child is the legal owner; the parents are jointly responsible for repayments.

The advantage is that the child gets a bigger mortgage and the property does not count as a "second home" for the parents (avoiding the 5% Stamp Duty surcharge on additional properties). The risk is that the parents are fully on the hook for missed payments, even though they do not own the property.

Guarantor Mortgages

The guarantor (usually a parent) does not appear on the mortgage but pledges to cover any missed payments. Variants include savings-as-security mortgages where the guarantor's savings are held in an account linked to the mortgage and earn interest, but cannot be withdrawn until the mortgage is repaid or has reduced to a target LTV.

Family Springboard and Deposit-Free Mortgages

Products like Barclays Family Springboard let a buyer take a 100% LTV mortgage where a family member places 10% of the purchase price into a linked savings account for 5 years. The savings earn interest and are returned at the end of the period if the mortgage payments have been kept up to date.

These provide effectively the same outcome as a 90% LTV mortgage with a parental gift - but the parents get their money back rather than gifting it permanently.

Income Boost Mortgages

Some lenders allow up to four borrowers' incomes to count toward affordability. Useful for groups of friends buying together or multi-generational household arrangements. Be careful about the legal structure - jointly owning a property with friends is much harder to unwind than a couple's joint ownership.

Specialist Mortgages

These cover specific purposes outside the typical home-purchase use case.

Buy-to-Let

Mortgages on properties bought to rent out. Almost always interest-only on a fixed-rate basis, with the rental income covering the interest and the property itself acting as the repayment vehicle (usually via sale at the end of the term).

In 2026, buy-to-let lenders apply rental stress tests at notional rates of around 6-7%, regardless of the actual product rate, to make sure the rent comfortably covers payments. Tax changes since 2017 have made buy-to-let materially less profitable for higher-rate taxpayers, especially after the phased loss of full mortgage interest tax relief. Many landlords now hold properties through limited companies rather than personally.

Offset Mortgages

Your savings sit in an account linked to the mortgage. Interest is charged only on the difference between your mortgage balance and your savings balance. £200,000 mortgage with £50,000 in savings means you pay interest on just £150,000.

Offset mortgages work brilliantly for self-employed borrowers who want to keep cash liquid for tax bills, or for high earners who would otherwise have a lot of cash sitting in low-yielding savings accounts. The trade-off is a slightly higher product rate than equivalent non-offset deals.

Self-Build Mortgages

Released in stages as the build progresses, secured against the value of the land plus completed work. The borrower pays interest on the drawn amount, not the full loan. At completion, the loan converts to a standard residential mortgage. Useful for people building their own home but more complex and more expensive than buying an existing property.

Bridging Loans

Short-term loans (3-24 months) used to bridge a gap, most commonly buying a new home before selling the old one. Interest rates are very high (8-15% APR equivalent) and arrangement fees are typically 1-2% of the loan. Bridging is genuinely useful in specific scenarios - auction purchases, chain breaks - but expensive enough that it should be a last resort, not a default.

Holiday Let Mortgages

For properties let out on platforms like Airbnb or Sykes Cottages on a short-term basis. Lenders apply different stress tests than buy-to-let because rental income is seasonal and less predictable. Tax treatment is also different - the Furnished Holiday Lettings regime was abolished from 6 April 2025, bringing FHL income under standard property income rules, so check current treatment with an accountant.

Self-Employed Mortgages

Not technically a different product, but lenders apply different income criteria. Most require 2-3 years of certified accounts or SA302s for sole traders. Specialist lenders accept 12 months of accounts or contractor day rates. Brokers who specialise in self-employed cases can dramatically improve your acceptance odds and rate.

Mortgages for Older Borrowers

Two products specifically for the over-55 segment.

Retirement Interest-Only (RIO)

You pay only the interest each month, like a buy-to-let. The capital is repaid when the property is sold, usually after the owner moves into care or dies. Income requirements are based on retirement income (pensions, drawdown, rental income) rather than employment income.

Useful for older borrowers who want to release equity but keep monthly costs predictable. The downside is that the principal never reduces, so the property's eventual value goes mostly to repaying the mortgage rather than to heirs.

Lifetime Mortgages (Equity Release)

A long-term loan secured against your home with no monthly payments required. Interest accrues and compounds, repaid when the property is sold (typically on death or move into care). The total debt can grow significantly over a 20+ year horizon.

Lifetime mortgages are tightly regulated by the FCA and member firms of the Equity Release Council offer a no-negative-equity guarantee, meaning the debt cannot exceed the eventual sale value. They suit older homeowners who want to access wealth tied up in their property without selling, but the compounding interest means the cost can be very high if held for decades. Independent advice is mandatory before taking one out.

Right to Buy and Forces Help to Buy

Two niche schemes worth knowing about.

Right to Buy lets council and most housing association tenants in England buy their home at a discount, depending on length of tenancy. The maximum discount cap was reduced sharply on 21 November 2024, bringing the cap down from £102,400 to broadly the pre-2012 regional limits (around £16,000 to £38,000 depending on region). It still exists; it is just much narrower.

Forces Help to Buy is an interest-free loan of up to 50% of salary (capped at £25,000) for serving members of the armed forces, repaid over 10 years. Useful as a deposit boost. The scheme has been extended through 2026 and beyond.

Green Mortgages

Several major UK lenders now offer "green mortgages" - typically a small rate discount (0.05% to 0.20%) for properties with EPC ratings of A or B, or for energy-efficiency improvements made within a certain period of purchase. The discounts are modest and the eligibility tight, but if you are buying a new-build (almost always EPC B or A) the green product is sometimes available with no extra hassle.

Some lenders also offer "green further advances" - additional borrowing earmarked for energy improvements (insulation, heat pumps, solar) at a discounted rate. Whether the rate discount actually saves money compared to a standard further advance varies, so do the maths.

How to Choose Between All These Options

The mortgage choice problem usually breaks into three questions answered in order.

1. What is your situation? First-time buyer, mover, remortgage, releasing equity, building, buying to let. This rules out about half of the options immediately.

2. What rate type do you want? Fixed-rate is the default for predictable monthly costs. Tracker is cheaper if you expect rates to fall and have flexibility on monthly outgoings. SVR is almost never the right answer.

3. What schemes apply to you? First-time buyers have access to several layered schemes (LISA + Mortgage Guarantee + First Homes might apply to the same buyer). Family help opens more options. Older borrowers, self-employed borrowers, and self-builders have specialist routes.

A good independent broker is the single most useful resource here. They have access to deals that direct-to-bank applications do not, and they know which lenders are friendly to which situations. The cost (typically £300-£600 for a fee-charging broker, free for fee-free brokers paid by the lender) is almost always recovered in better rate or product fit. The government-backed MoneyHelper service also publishes free, impartial guidance on every scheme covered above and is a sensible second source if your broker only knows their own panel of lenders.

For the post-purchase question of whether to overpay or invest spare cash, our guides on should I pay off my mortgage or invest and the invest vs pay off mortgage calculator cover the maths.

Frequently Asked Questions

What is the most common type of UK mortgage in 2026?

A capital-and-interest (repayment) mortgage on a 5-year fixed-rate deal at 75-90% LTV. This combination accounts for roughly half of all new UK mortgage lending. The next most common is the 2-year fixed equivalent.

Can I still get Help to Buy in 2026?

The Help to Buy Equity Loan scheme closed to new applicants in March 2023. Existing Help to Buy loans continue to run as agreed. The replacement schemes are the Mortgage Guarantee Scheme, First Homes, and Shared Ownership.

How much deposit do I need for a UK mortgage in 2026?

The mainstream market starts at 5% (95% LTV) under the Mortgage Guarantee Scheme. A handful of lenders offer 100% LTV products like Skipton's Track Record. Below 5%, the market thins out quickly and rates rise sharply. Above 25% deposit, you typically access the cheapest rates.

What is the maximum I can borrow against my income?

Most lenders apply a 4.5x salary multiplier as a default, but several offer up to 5.5x or 6x for first-time buyers earning above certain thresholds (typically £50,000+) under specific products. Affordability is also stress-tested at higher rates, so the headline multiple is not the only constraint.

Is interest-only still available for owner-occupiers?

Yes, but tightly. Lenders require a credible capital repayment vehicle (investment portfolio, pension, sale of another property) and typically restrict interest-only to higher-income or higher-equity borrowers. It is rare for first-time buyers and standard movers in 2026.

What is the difference between a tracker and a discount variable mortgage?

A tracker is tied to the Bank of England base rate plus a fixed margin. A discount variable is tied to the lender's SVR with a fixed discount. Trackers track the base rate transparently; discount variables move when the lender chooses to move their SVR (correlated to base rate but not directly).

Further Reading:

I Will Teach You To Be Rich - Ramit Sethi - Sethi's chapter on mortgages and the rent-vs-buy decision is one of the clearest treatments of the subject for anyone weighing whether home ownership fits their financial life. (Affiliate link - we may earn a small commission at no extra cost to you.)

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all