State Pension Forecast UK: How to Check Yours

Missing NI years are quietly costing thousands of UK workers retirement income forever. A two-minute gov.uk check could be the highest-return move you ever make in your fifties.

Cite this article

Freedom Isn't Free (2026) State Pension Forecast UK: How to Check Yours. Available at: https://freedomisntfree.co.uk/articles/state-pension-forecast-uk (Accessed: 29 July 2026).

Italicise the article title in your bibliography. Accessed date set to today.

TLDR

- A full new State Pension in 2026/27 is £241.30 a week, requiring 35 qualifying National Insurance years

- Check your forecast at gov.uk/check-state-pension - takes 2 minutes with a Government Gateway login

- Missing years can be filled by paying voluntary Class 3 NI contributions, currently around £900 per year - usually a high-return move

- Stay-at-home parents earn NI credits automatically if they claim Child Benefit, even when opting out of payment

State Pension Forecast UK: How to Check Yours

A full new State Pension forecast UK workers receive in 2026/27 is £241.30 a week, or roughly £12,548 a year. Get it wrong - miss qualifying years, fail to claim credits, retire abroad without checking the rules - and the gap between what you expect and what you receive can be thousands of pounds a year for the rest of your life.

This guide covers how to check your forecast in two minutes, what the qualifying-years system actually requires, how to fill gaps before they cost you, and the few quirks that catch people out.

Contents

- How to check your State Pension forecast

- What the forecast actually shows

- The 35-year rule explained

- How to fill gaps in your NI record

- Voluntary Class 3 contributions

- Special cases: NI credits, deferral, expats

- Frequently asked questions

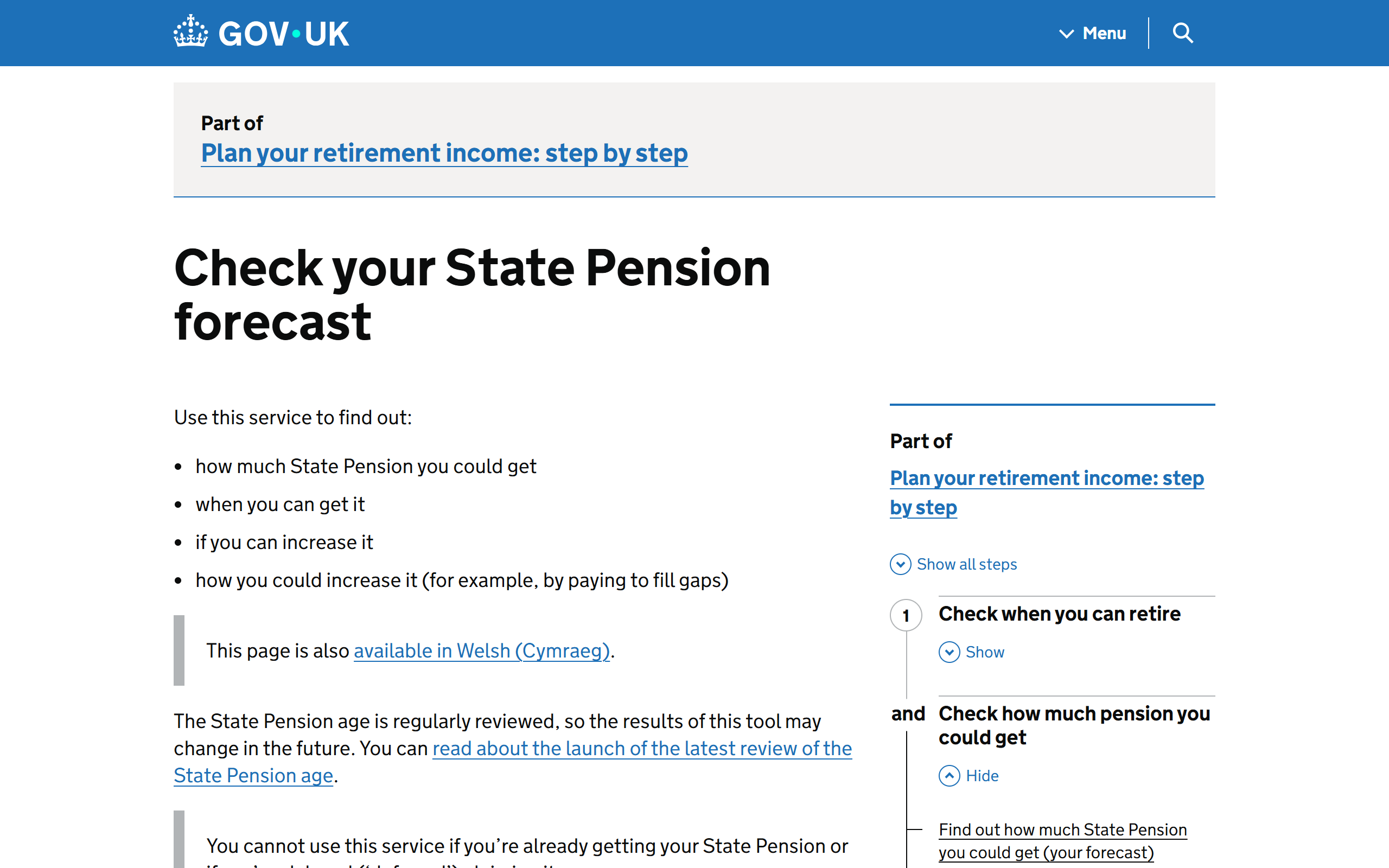

How to Check Your State Pension Forecast

The official tool sits at gov.uk/check-state-pension. To access it you will need:

- A Government Gateway login (create one on the spot if you do not have one - you will need ID such as a passport or driving licence to verify)

- Your National Insurance number

- A working email address

The check itself takes about two minutes. You will see:

- Your current forecast (what you would receive at State Pension age based on contributions to date)

- Your maximum possible forecast (what you would receive if you contribute every year between now and State Pension age)

- Your full National Insurance record (year by year, showing whether each is "full", "incomplete", or "missing")

If you have not checked it before and you have ever worked abroad, taken a career break, or had self-employment phases, do this today. The number of households we have seen with quietly missing years is striking.

What the Forecast Actually Shows

The forecast page reports three figures that often get confused:

- Estimate based on your NI record so far. What you would get if you stopped earning and stopped contributing tomorrow.

- Forecast if you contribute until State Pension age. The figure you will probably actually receive, assuming you keep working until 67 (66 for those born before April 1960).

- The maximum amount you could ever get. Capped at the full new State Pension - £241.30 a week in 2026/27.

The new State Pension applies if you reach State Pension age on or after 6 April 2016. For older retirees the basic State Pension and additional pension rules apply, which is a different (and more complex) calculation.

The forecast does not account for any uprating beyond the current rate. The triple lock has uprated the State Pension by ~5-10% per year recently, so the figure you see today is a floor, not a ceiling.

The 35-Year Rule Explained

To get the full new State Pension you need 35 qualifying years of National Insurance contributions or credits.

A qualifying year is one in which:

- You were employed and earning above the Lower Earnings Limit (£6,396 in 2026/27), with NI deducted from your pay

- You were self-employed and paying Class 2 contributions

- You received NI credits (e.g., from claiming Child Benefit, being on Universal Credit, or carer's credit)

- You paid voluntary Class 3 contributions to fill a gap

Below 10 qualifying years you get nothing. Between 10 and 35 you get a pro-rata amount: each year after the first 10 adds 1/35th of the full pension.

Worked example: 25 qualifying years = (25 / 35) × £241.30 = £172.36 a week, or about £8,963 a year. The 10 missing years cost roughly £3,585 a year for life.

Annual State Pension by qualifying NI years, 2026/27

Source: gov.uk new State Pension rules, full rate £241.30 a week

How to Fill Gaps in Your NI Record

When you check your forecast, the GOV.UK page lists every tax year and flags incomplete or missing ones. For each gap, you have a few options:

- Voluntary Class 3 contributions. Pay HMRC directly to credit a missing year. Costs about £907.40 for the 2026/27 tax year (the rate is set annually). For most people, paying Class 3 is one of the highest-return moves available - £900 to gain £329/year for life is roughly a 36% annual return if you live a typical lifespan post-State-Pension-age.

- Class 2 (self-employed). If you were self-employed in a missing year and your profit was below the threshold, you can voluntarily pay Class 2 (~£183 per year for 2026/27) instead of Class 3. Much cheaper for the same credit.

- Backdated NI credits. Carer's credit, Universal Credit, and Child Benefit credits can sometimes be backdated if you forgot to claim. Worth ringing HMRC if you have a clear gap and a reason it should have been credited.

The deadline for voluntary contributions is normally 6 years from the end of the tax year in question. There has been a series of extensions to allow people to fill gaps from 2006 onwards, with the most recent extension closing in April 2025. After that the standard 6-year window applies again.

Voluntary Class 3 Contributions

Class 3 is the catch-all "buy a missing year" payment. To decide whether it is worth paying:

- Check your forecast. Does it already show the maximum £241.30/week? If yes, paying for more years is worthless - you cannot exceed the full pension.

- Are you below the maximum? Each missing year you fill adds ~£329/year to your eventual pension.

- Will you reach the maximum naturally before State Pension age? If you are 45 with 25 qualifying years and plan to work until 67, you will hit 47 qualifying years naturally and never need Class 3. The 35-year ceiling matters.

The number of people we have seen pay Class 3 unnecessarily because they were on track to hit 35 years anyway is significant. Always check your forecast first. The Future Pension Centre on 0800 731 0181 will confirm whether paying for a specific year actually moves your eventual pension.

Special Cases: NI Credits, Deferral, Expats

NI Credits for stay-at-home parents

If a parent is at home looking after a child under 12 and they (or their partner) claims Child Benefit, the parent earns Class 3 NI credits automatically - even if they have opted out of receiving payment. This is the most-missed credit on UK State Pension records. If you have ever been a stay-at-home parent and were not claiming Child Benefit, this is worth investigating immediately.

Deferral

You can defer drawing the State Pension when you reach State Pension age. The current uplift for the new State Pension is 1% for every 9 weeks deferred (~5.8% per year). Whether deferral is worth it depends on your other income, life expectancy, and tax position - generally deferral wins for healthy retirees with no immediate need for the income, especially those still earning who would otherwise be taxed at higher rates.

Retiring abroad

Pensions paid into bank accounts in EU/EEA countries, Switzerland, the US, and a small group of other "treaty" countries continue to receive annual triple-lock uprating. Pensions paid into "frozen rate" countries (Australia, Canada, India, South Africa, and many others) stay at the rate they were when you first drew the pension and never increase. This frozen-rate policy has been criticised for decades but remains in place. Check the GOV.UK list before relocating.

For a fuller picture of how the State Pension fits with private savings, run your numbers through the Life Plan Calculator.

Working past State Pension age

You stop paying NI contributions from the date you reach State Pension age, regardless of whether you continue working. You also become eligible for the State Pension itself, even if your salary continues. The State Pension is taxable income, so for higher earners continuing to work, deferral often makes more sense than drawing-while-working.

Frequently Asked Questions

How do I check my UK State Pension forecast?

Go to gov.uk/check-state-pension and log in with your Government Gateway account (you can create one on the spot if you do not have one). The check takes about two minutes and shows your current forecast, your projected forecast, and your full year-by-year NI record.

How many years do I need for a full UK State Pension?

35 qualifying years of National Insurance contributions or credits. Below 10 years you get nothing. Between 10 and 35 you get a pro-rata amount based on the number of qualifying years.

Can I top up my State Pension by paying voluntary contributions?

Yes. Class 3 voluntary contributions cost about £907.40 to fill a missing year for 2026/27. Each filled year adds roughly £329 a year to your eventual pension - usually a strong return for the cost, provided you are not already on track to hit 35 years naturally.

What is the new State Pension rate in 2026/27?

£241.30 a week, or about £12,548 per year. This applies to those reaching State Pension age on or after 6 April 2016. The rate is uprated annually by the triple lock - the highest of CPI inflation, average earnings growth, or 2.5%.

What happens if I retire abroad?

State Pension is paid into UK or overseas bank accounts. In the UK and "treaty" countries (most of Europe, US, Switzerland), it continues to receive annual triple-lock increases. In "frozen rate" countries (Australia, Canada, parts of Asia), it stays at the level you first drew it. Check the GOV.UK frozen-rate list before relocating.

Prefer to watch?

We turn these money breakdowns into short videos

A few a week, plain-English UK money. If you would sooner watch than read, follow along:

Enjoying the content?

If this site has been useful, a coffee goes a long way.

Browse more articles

Browse all